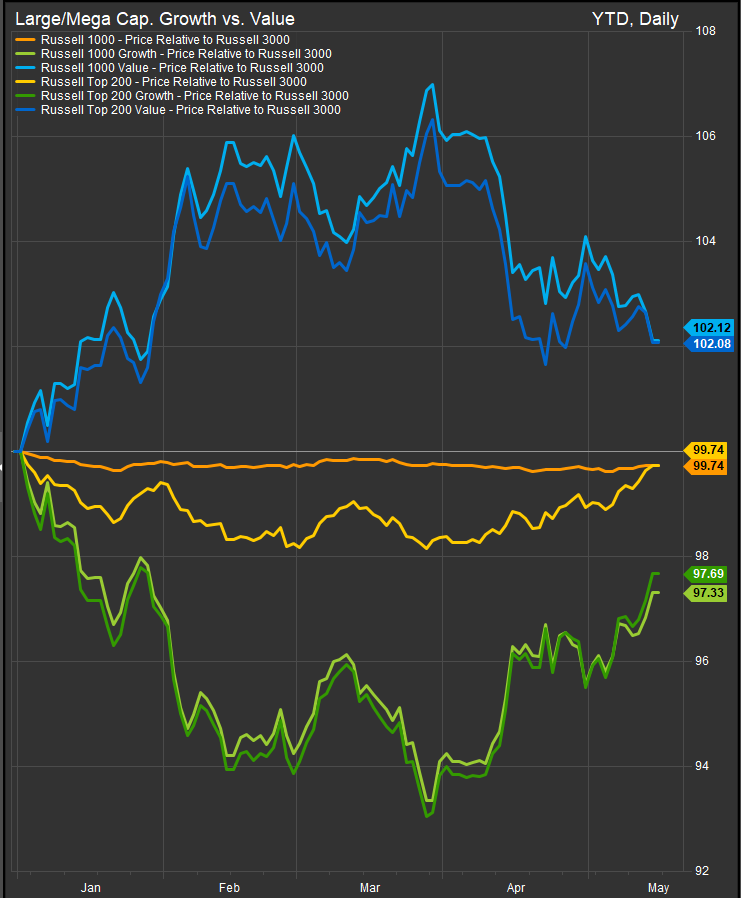

The current style tape still favors Value, but the more interesting story is that the trade has become less one-sided. Russell Large cap. style indices versus the Russell 3000 show a clear trend, so the right interpretation is not “absolute return,” but which style is gaining or losing ground versus the broad market. On that basis, Value is still ahead YTD, while Growth has been trying to repair early-year damage.

| Style Index | Relative level vs. Russell 3000 | YTD relative move |

| Russell 1000 Growth | 97.33 | -2.67% |

| Russell 1000 Value | 102.12 | +2.12% |

| Russell 1000 Growth vs. Value spread | — | Growth trails Value by ~4.7% |

| Russell Top 200 Growth | 97.69 | -2.31% |

| Russell Top 200 Value | 102.08 | +2.08% |

The conclusion: Value owns the YTD leadership, but Growth owns the optionality. Since late March, the Russell 1000 Growth relative has rebounded from a trough near 93.36 to 97.33, while Russell 1000 Value has faded from roughly 107.00 to 102.12. That is not enough to flip the year, but it is enough to say the market is no longer simply “buy Value, sell Growth.” It is now testing whether the AI-growth narrative can overcome a macro backdrop that still looks friendlier to Value.

This distinction matters because Growth and Value are not just labels. FTSE Russell’s style framework uses book-to-price for value and two growth characteristics: medium-term forecast earnings growth and five-year historical sales-per-share growth. Its Russell U.S. indexes also allow investors to track style and market-cap segments under the broader Russell 3000 architecture.

The macro regime still leans Value. The latest headlines frame a classic Value-friendly tape: global yields backing up, war-driven inflation fears, stretched positioning in tech, weak breadth, and risk-off pressure after an underwhelming Trump-Xi summit and continued Middle East uncertainty. That is exactly the mix that usually pressures long-duration Growth multiples and rewards investors for owning cheaper, cash-generative, dividend-paying, more inflation-linked businesses.

The outside data reinforce that tension. BLS reported that April CPI energy prices rose 3.8% on the month, gasoline rose 5.4%, core CPI rose 0.4%, and all-items CPI was up 3.8% over the last 12 months. BLS also reported April PPI final demand up 1.4%, with services up 1.2%, goods up 2.0%, and final demand prices up 6.0% over 12 months. Reuters added that the 10-year Treasury yield hit 4.54%, Brent crude climbed near $109, and Nasdaq futures were hit harder than Dow futures as inflation and rate concerns weighed on the AI rally.

That is the Value case in one sentence: higher oil, higher yields, and higher inflation make valuation discipline matter again. Value is not just “cheap”; in this environment, it is also a proxy for nearer-term earnings, more tangible cash flows, and sectors that can benefit from nominal growth, energy scarcity, reshoring, defense spending, financial intermediation, and dividends.

Growth, however, has a powerful catalyst: AI is becoming a capital-cycle story, not just an earnings-revision story. The headlines cite Applied Materials’ strong semiconductor-equipment demand, Figma’s AI monetization, Cerebras’ debut, Big Tech borrowing to fund AI expansion, and continued AI-agent competition. Reuters separately reported that Alphabet, Amazon, Microsoft, and Meta have signaled AI spending will not slow, with combined spending now expected to exceed $700 billion this year.

That is Growth’s path back to leadership: AI must broaden from a multiple story into a revenue, productivity, and operating-leverage story. If hyperscaler spending pulls through semiconductors, power equipment, networking, software, cloud, cybersecurity, industrial automation, and enterprise productivity, Growth can outperform even in a higher-rate world. The New York Fed’s Williams also pointed to investor optimism about future productivity growth, “partly AI,” while saying he saw no need right now to raise or lower rates.

But Growth’s Achilles’ heel is also becoming clearer. The same AI capex boom that excites investors is now funded with more debt and heavier cash-flow demands. Reuters reported that the large tech companies’ AI outlays are squeezing cash flows and testing investor patience. That makes Growth vulnerable to any sign that AI revenue is lagging AI spend, that China chip restrictions are binding, or that rising yields force the market to discount future earnings more harshly.

The valuation gap is another reason Value still has the edge. BlackRock’s iShares Russell 1000 Growth ETF (IWF) is at a P/E of 39.18 and P/B of 13.91, while iShares Russell 1000 Value ETF (IWD) is at a P/E of 22.94 and P/B of 3.12, both as of May 13, 2026. BlackRock’s current YTD NAV return snapshots also show IWD ahead of IWF, with IWD at 12.01% YTD and IWF at 5.17% YTD as of May 13.

Catalysts for Value outperformance

Value likely continues to outperform if the market remains in a stagflation-lite regime: oil stays high, inflation surprises remain hotter than expected, the Fed stays patient or turns more hawkish, and bond yields keep backing up. In that world, investors may continue rotating away from expensive long-duration earnings and toward financials, energy, industrials, defense, materials, healthcare value, and cash-return stories.

A second catalyst is breadth repair by rotation rather than by melt-up. The morning headlines note concerns about narrow leadership and fewer active managers beating the S&P 500 as the rally is led by a concentrated group of tech megacaps. If allocators decide concentration risk has become a portfolio problem, Value can win flows simply by being the cheaper, under-owned alternative.

A third catalyst is geopolitical persistence. If the Strait of Hormuz remains impaired, inventories keep drawing, energy security becomes a policy priority, or rare-earth and chip frictions with China remain unresolved, the market may favor real assets, domestic supply chains, defense, energy infrastructure, and old-economy pricing power over high-multiple platform companies. The headline file flags depleted oil inventories, slow rare-earth progress, no semiconductor breakthrough, and ongoing Iran-related energy stress.

Catalysts for Growth outperformance

Growth can regain leadership if rates stabilize. It does not necessarily need aggressive Fed cuts; it needs the bond market to stop repricing higher inflation risk. A durable decline in oil prices, softer CPI/PPI prints, or evidence that the Middle East shock is transitory would lower the discount-rate pressure on Growth.

The bigger catalyst is AI proof of monetization. Growth will outperform if investors see that AI capex is not just defensive spending but is translating into cloud revenue, semiconductor order durability, software pricing power, productivity gains, and margin expansion. The headlines around Applied Materials, Figma, Cerebras, and AI funding all point to that possibility, but the market will need proof beyond “AI demand is strong.”

A third catalyst is geopolitical relief for semis and China-exposed tech. The Trump-Xi summit produced few deliverables, and the headlines specifically note no breakthrough on rare earths or Nvidia H200 sales into China. Any improvement there would directly help Growth sentiment, especially semiconductors, mega-cap platforms, and AI infrastructure suppliers.

Bottom line

For now, current macro dynamics favor Value, because the tape is defined by higher yields, energy inflation, geopolitical risk, and valuation sensitivity. But the market action since late March says investors are not abandoning Growth; they are demanding proof of AI-related monetization. Where that’s happening on the capital expenditure side, investors are accumulating the trade. Where it remains speculative, increasing profitability to legacy business lines, is where investors have been unwilling to follow. We see that most clearly in the Consumer and Financial sectors.

The best read is: Value is the incumbent leader, Growth is the challenger with a powerful catalyst but a narrower margin for error. Value wins if inflation and rates stay sticky. Growth wins if AI monetization broadens and yields stop rising.

Sources:

- Index and performance data sourced from Factset Research Systems Inc.

- LSEG / FTSE Russell — Russell U.S. Style Index methodology and Growth/Value factor definitions.

- BLS — April 2026 Consumer Price Index release.

- BLS — April 2026 Producer Price Index release.

- iShares / BlackRock — Russell 1000 Growth ETF valuation and YTD return data.

- iShares / BlackRock — Russell 1000 Value ETF valuation and YTD return data.

- Reuters — market/rates reaction to inflation, oil, and risk-off dynamics.

- Reuters — Big Tech borrowing to fund AI/cloud expansion.

- Reuters — investor scrutiny of Big Tech AI capex/payoff.

- Reuters — NY Fed President Williams on policy, inflation uncertainty, and AI/productivity optimism

Disclaimer

This material is for informational and educational purposes only and should not be construed as investment advice, a recommendation, or an offer to buy or sell any security, strategy, or investment product. Views are based on market conditions, index data, and headline developments available at the time of writing, including the uploaded headline pack.

Factor performance can change quickly, and Growth and Value styles may behave differently across sectors, market-cap segments, interest-rate regimes, and economic cycles. Past performance is not indicative of future results. Indexes are unmanaged, do not reflect fees or expenses, and cannot be invested in directly. Investors should consult their own financial, tax, and legal advisers before making investment decisions