March 6, 2026

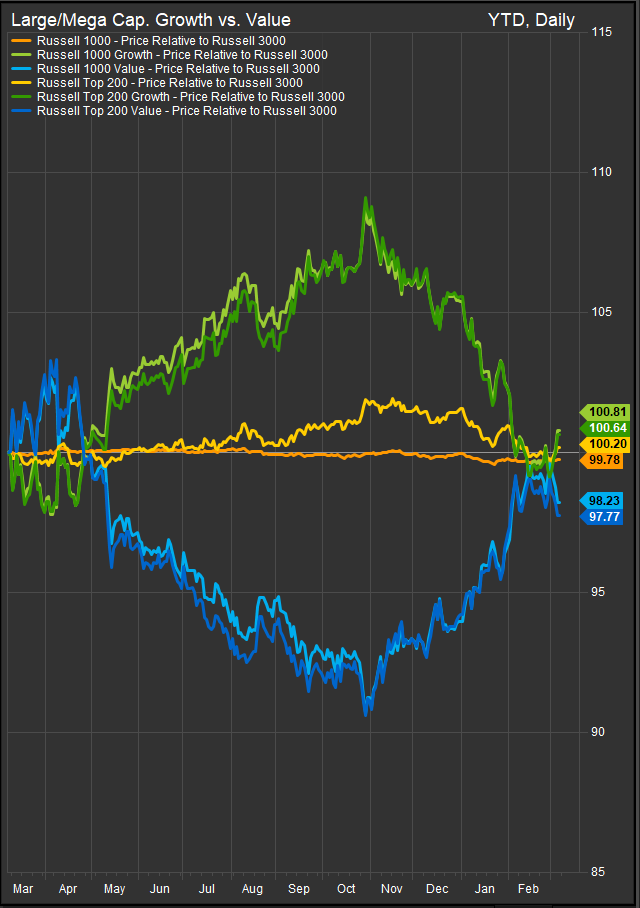

The factor leadership in U.S. equities has shifted abruptly in the very near term, with Large Cap Growth reasserting leadership after several months of Value and cyclical outperformance. The move appears less like a structural rotation and more like a tactical repositioning driven by macro stabilization, positioning dynamics, and renewed confidence around the durability of the AI investment cycle.

The April 2025 lows were the last major pivot for Growth vs. Value favoring the latter. The roundtrip in performance sets up another potential pivot. However, we think upwards pressure on rates likely supports Value if it continues.

Over the past several weeks, a combination of geopolitical risk, commodity strength, and rising real yields pushed investors toward Value-oriented exposures—including Energy, Financials, and Materials. Those sectors benefited from inflation hedging and higher interest rates, while Growth sectors such as Technology and Communication Services faced valuation compression and concerns around capital intensity related to AI infrastructure spending.

However, several developments have catalyzed a short-term rebound in Growth. First, bond yields have stabilized, easing pressure on long-duration equity valuations. Growth stocks tend to be particularly sensitive to real yields because their cash flows are weighted toward the future. Even modest declines in real yields can therefore support multiple expansion. The stabilization of the U.S. 10-year yield in the low-4% range has removed one of the most immediate headwinds facing Growth exposures.

Second, AI demand expectations remain strong despite recent skepticism. Hyperscalers such as Alphabet, Amazon, Meta, and Microsoft continue to signal massive capital expenditures tied to artificial intelligence infrastructure. Estimates suggest combined capex among these firms could approach $650 billion annually in the next cycle, reinforcing the view that the AI buildout remains one of the dominant investment themes in global markets. Semiconductor and infrastructure suppliers have consequently rebounded as investors reassess whether the earlier selloff overstated the risk to earnings growth.

Third, positioning and sentiment had become excessively defensive. Over recent months, flows into commodities, natural resources, and dividend-oriented sectors rose sharply, while exposure to high-growth technology stocks was reduced. When macro volatility stabilized and earnings expectations remained intact, investors began rebuilding Growth exposure. Short covering and systematic strategies likely amplified the move.

Finally, earnings momentum continues to favor Growth sectors. Technology and communication services still represent the largest contributors to overall S&P 500 earnings expansion. Even as macro growth moderates, many of these companies maintain structurally higher margins and balance sheets capable of funding large investment cycles.

Growth vs. Value: Which Factor Wins Next?

Looking forward, the balance between Growth and Value leadership will likely hinge on three macro variables: real interest rates, earnings momentum, and the durability of the AI investment cycle.

If real yields remain stable or decline modestly, the environment is likely supportive for Growth. In that scenario, investors may once again prioritize earnings durability and structural innovation, particularly within the semiconductor, software, and cloud infrastructure ecosystems. The large technology platforms remain central to productivity gains across the global economy, and their ability to finance massive capital investment internally reinforces their competitive positioning.

However, if inflation pressures persist and real yields move meaningfully higher, Value-oriented sectors could reassert leadership. Energy, financials, and industrial cyclicals typically outperform when rates rise because their earnings are more closely tied to current economic activity rather than distant future cash flows. Higher interest rates also compress valuation multiples for long-duration assets, disproportionately affecting Growth stocks.

With real yields near lows, we’d expect the next move to be higher given rising commodities prices in the near-term.

Commodity dynamics will also matter. Continued strength in energy and metals markets—driven by geopolitical risks, supply constraints, or infrastructure demand—would reinforce Value leadership through Energy and Materials exposures. Conversely, a moderation in commodity prices would remove one of the key pillars supporting Value over the past several months.

The Bloomberg Commodities Index is up >30% over the past 12-months. 115 is the current bull/bear pivot point on the chart. Continued upwards pressure on Commodities prices would be a headwind to Growth.

The final and perhaps most important factor is the return profile of AI investment. If corporate spending on artificial intelligence begins translating into measurable productivity gains and revenue expansion, Growth sectors will likely regain sustained leadership. But if investors begin to question whether the extraordinary capital spending required to build AI infrastructure will generate sufficient returns, Value sectors with stronger near-term cash flows could remain attractive.

Investment Perspective

At present, the evidence suggests that the recent rebound in Growth is primarily tactical rather than structural. The macro backdrop—moderate growth, still-elevated interest rates, and geopolitical uncertainty—argues for a balanced factor exposure rather than a decisive bet on either Growth or Value.

A pragmatic allocation approach may therefore emphasize barbell positioning: maintaining exposure to structural Growth themes such as AI and digital infrastructure while also holding Value-oriented sectors that benefit from higher real yields and commodity strength.

In short, Growth’s near-term rebound reflects easing macro pressure and renewed optimism around technology earnings. Whether that leadership becomes durable will depend largely on the path of interest rates—and on whether the enormous wave of AI investment ultimately delivers the productivity gains investors expect.

Out Elev8 model favored Energy and Low vol. inputs this month, but it also favored the Information Technology sector as the strongest long-term outperformance trend over the course of the cycle. The model retains 20% exposure. The point being, whether this is the beginning of the end for the speculative AI trade or not, it’s been the most powerful theme animating global equity markets for the last 3 years. There will continue to be plenty of debate about its prospects for good or ill as 2026 progresses.

FactSet Research Systems – Earnings Insight and sector earnings contribution data

Federal Reserve Economic Data (FRED) – 10-Year Treasury Yield and TIPS real yield series

CME FedWatch Tool – Market expectations for Federal Reserve policy and interest rates

Bloomberg – Coverage of AI infrastructure spending and hyperscaler capital expenditure trends

Reuters – Reporting on semiconductor sector outlook and global technology earnings trends

S&P Global Visible Alpha – Consensus estimates and capital expenditure forecasts for large technology companies

Goldman Sachs Global Investment Research – Factor rotation and positioning commentary on Growth vs. Value

Morgan Stanley Research – Analysis of equity factor performance and interest-rate sensitivity

Additional charts and data sourced from FactSet Research Systems Inc.