September 12, 2025

With the S&P 500 printing its latest all-time high yesterday and consensus now firm on Fed policy, it’s an excellent time to survey our factor charts to gage potential opportunities into year end. What has been clear since equities put in their April 7th low is that investor risk appetite has continued to firm. Commodities exposures and low vol. stocks have been out of favor, and the AI trade has reasserted its dominance over other themes in the equity market.

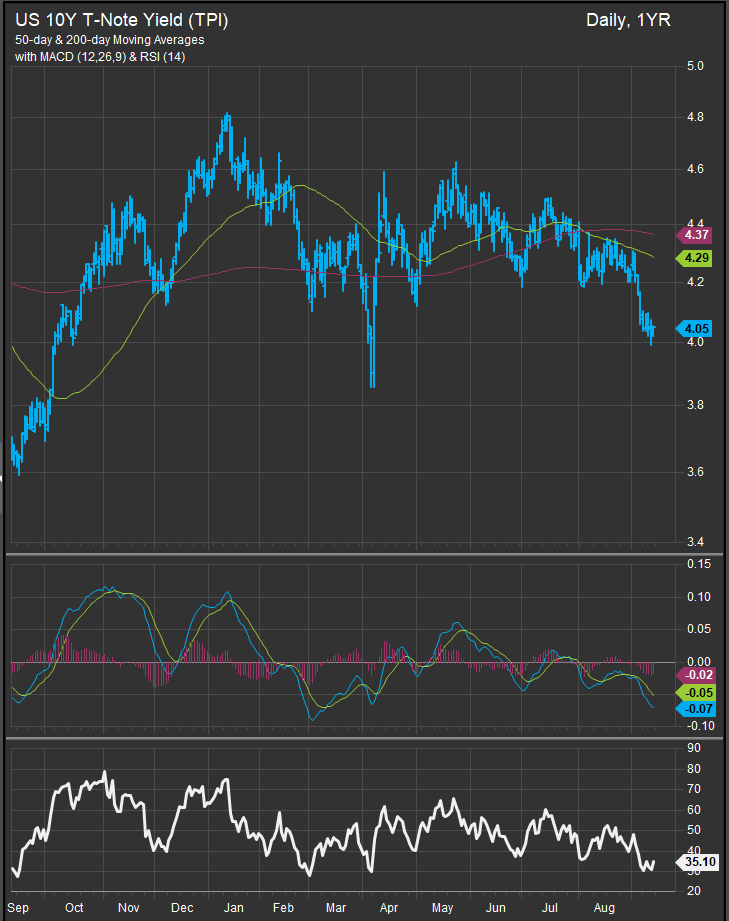

An easing Fed should be supportive of equities, but there is a need to remain vigilant as expectations of lower rates and the optimism that accompanies those expectations may lead to more inflationary outcomes going forward. The chart of the US 10yr (below) is showing deeply oversold conditions (bottom two panels) while equities are overbought. While the cadence of corporate earnings remains strong and the new flow remains positive, it is also true that a lot of good news is priced in. It will be interesting to see how investors respond to the next macro bogey that comes our way. We’d also note that yesterday’s bullishness sent the 10yr Yield higher, not a concern yet, just an illustration of the crosscurrents that are still in play.

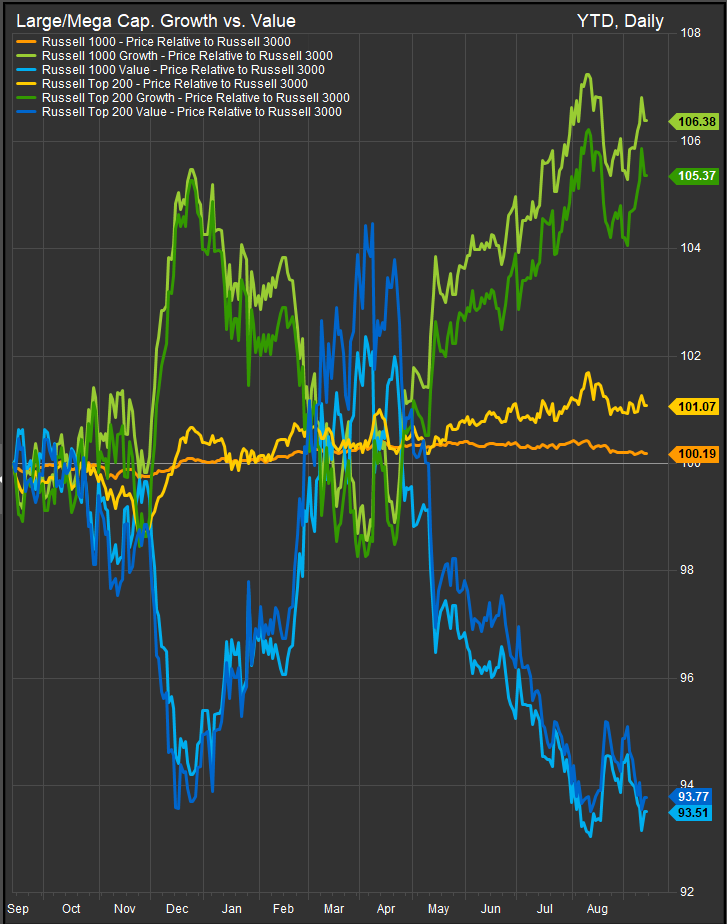

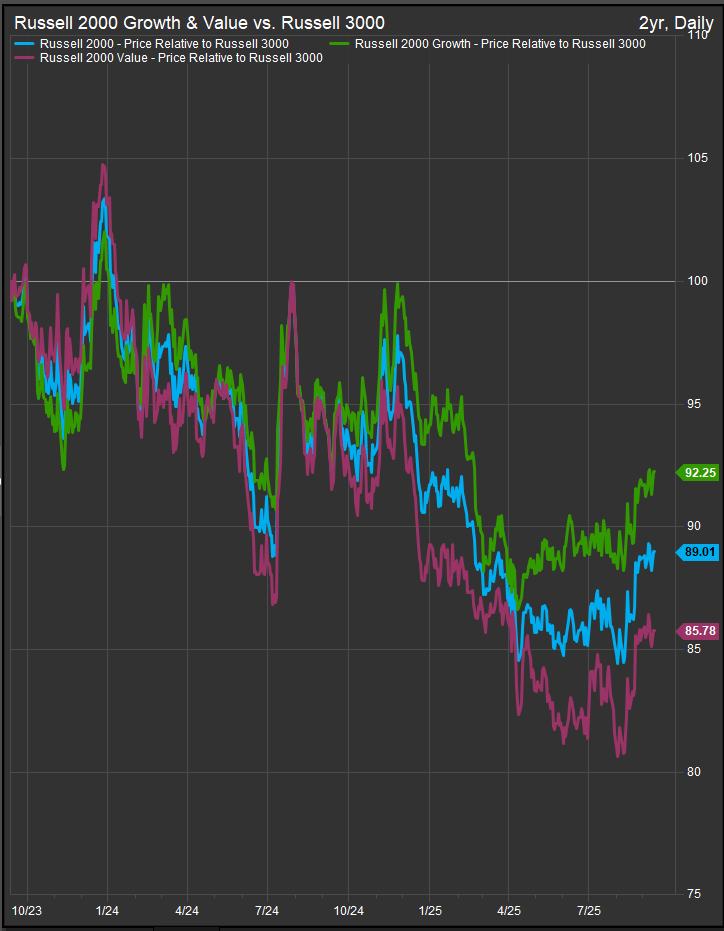

Growth/Value

Large cap. domestic stocks remain as bifurcated by Growth/Value performance dynamics as ever. Rotation risk is top of mind. As we’ve pointed out in the past, central bank easing often begins with a bid for laggards. When considering the relative performance of the Russell style indices vs. the broad market Russell 3000 Index, we can see that Value stocks are the laggard cohort among Large and Midcap tiers (Russell 1000).

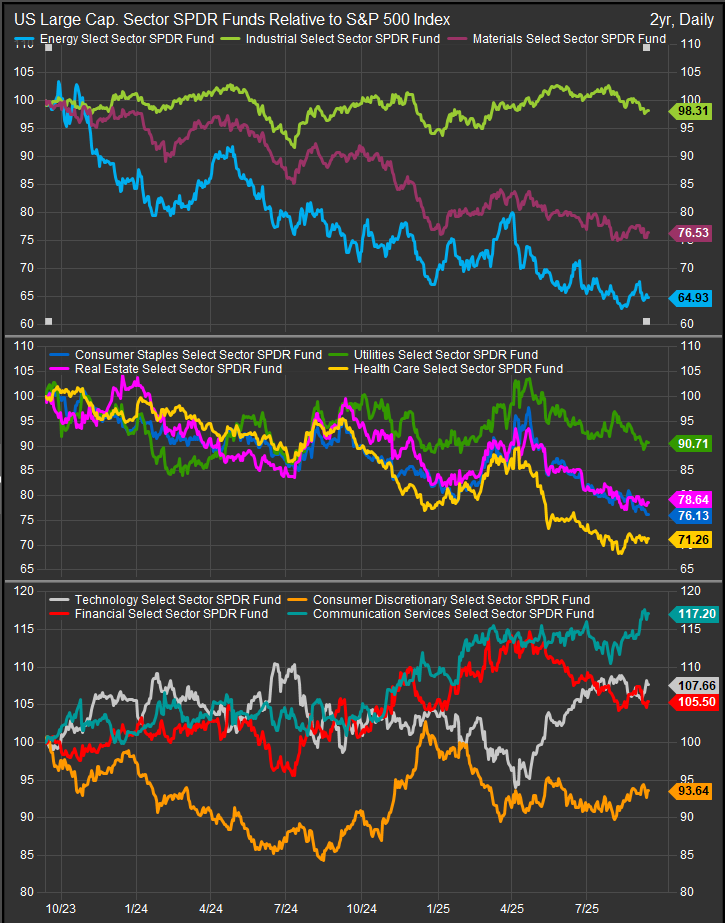

From a sector perspective that may put Large Cap. Technology and Comm. Services stocks on notice for some near-term profit taking (chart below, bottom panel) as both sectors have been leadership for much of the present bull trend while also enjoying strong performance in the near-term. Energy, Materials and low vol. stocks have been structural laggards in this cycle along with Discretionary stocks. We think this is a dynamic to pay close attention to.

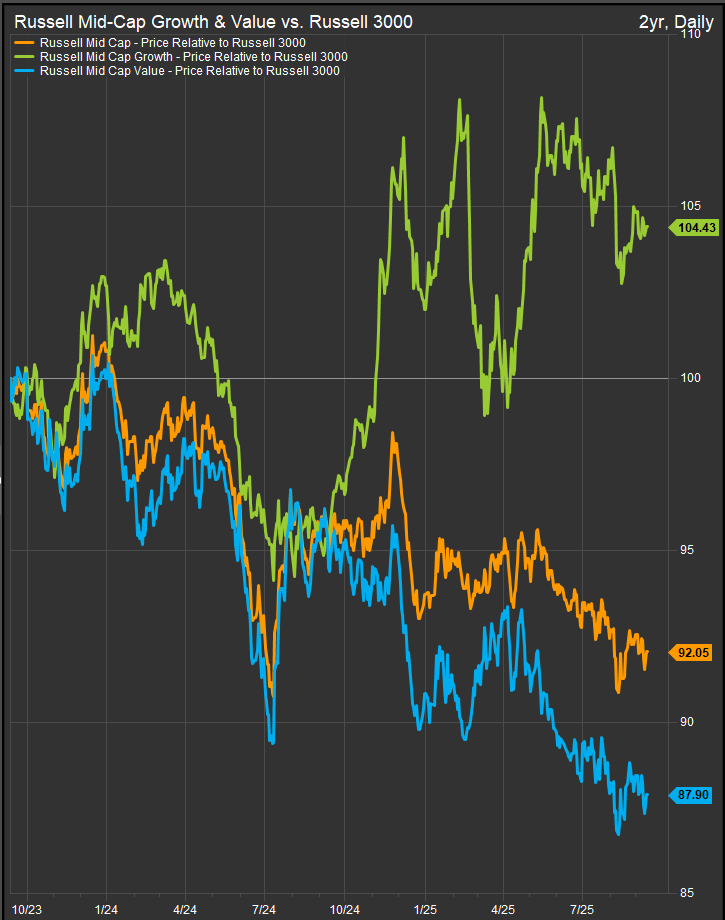

Small/Mid a Different Dynamic

While Mega Cap. Growth stocks have been strong enough to pull the Russell 1000 Growth benchmark higher, beneath the surface, MidCap stocks have been weak in the near-term while Small Cap. stocks have strengthened. MidCap. Growth has been part of the leadership cohort over the longer-term, but hasn’t sustained momentum in the near-term (chart below).

Small Cap. stocks are showing coincident strength regardless of Growth or Value style (chart below).

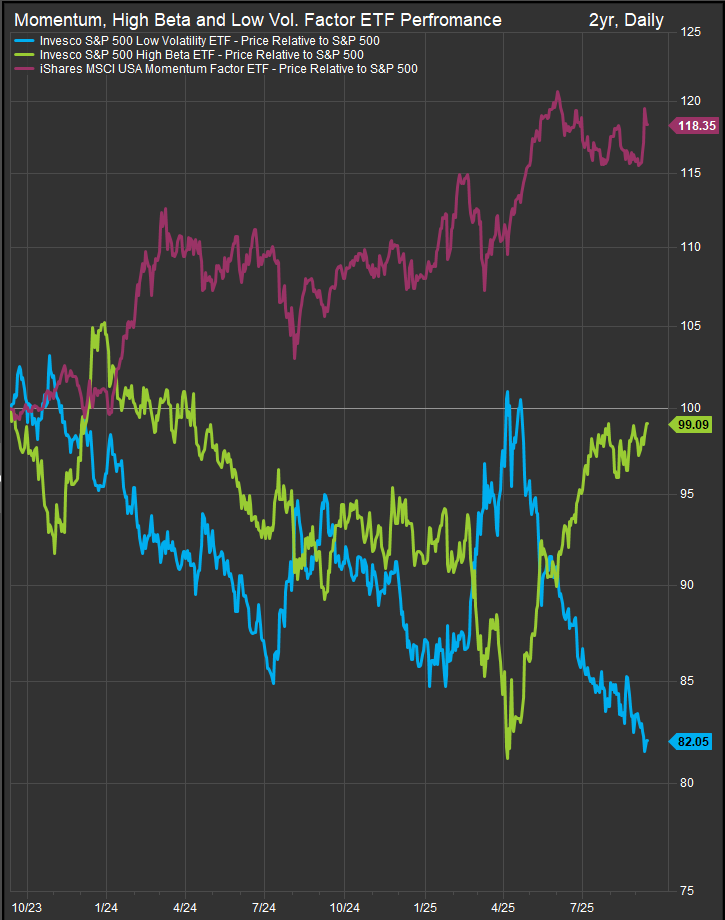

High Beta/Low Vol./Momentum

High Beta stocks have been the unambiguous preference since the April lows (chart below). Recently momentum stocks have caught a bid as well which can mainly be attributed to ORCL’s blow out quarter.

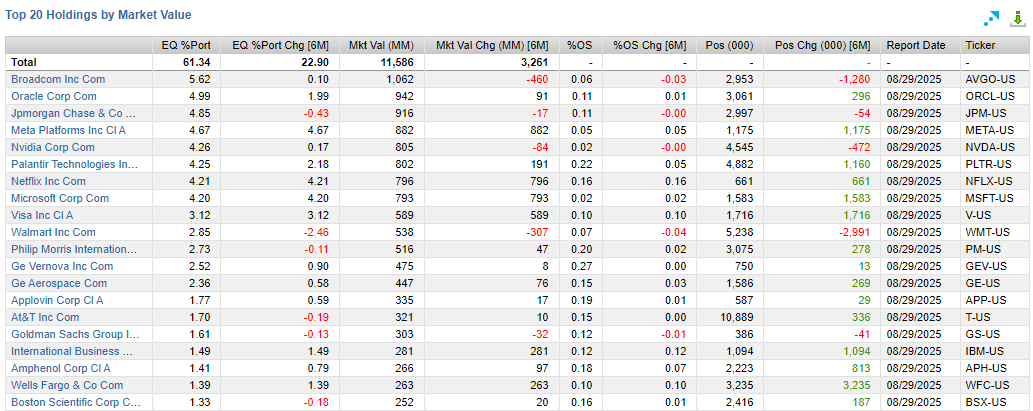

Top Mo. Holdings remain concentrated in Tech and Growth names (below).

MTUM-iShares MSCI Momentum Factor ETF | Top 20 Holdings

The nature of momentum investing is to keep riding the trend. Investors just need to keep that back-up plan in mind when style and factor spreads are as wide as they are now.

Risk on/Risk off

Our risk appetite gages generally remain firm (chart below). Copper/Gold is the notable exception, however that series has been in the global trade cross hairs, so it hasn’t been a great organic signal in the near-term. Volatility gages, VIX and MOVE, remain near lows, so do be prepared for your favorite economist to start talking about complacency.

Conclusion

An old technical analysis saw is that “the trend is your friend”. The present trend for equities is clearly bullish. We think there is some risk of rotation away from the Mega Cap. Growth trade, but not enough to go structurally short. We do think equity investors should diversify sector exposures to include more Value given the wide spread and firming conviction around ongoing Fed support for the economy. That said risk appetite is firm, enthusiasm for AI remains the driving force behind the bull market and inflation and interest rates have been getting more supportive at the margins in 2025 as well. We don’t want to let our fear of the unknown get too much credit vs. the very bullish picture that is right in front of our eyes.

Data sourced from FactSet Research Systems Inc.