ETF Insights | November 1, 2024 | Industrials Sector

Price Action & Performance

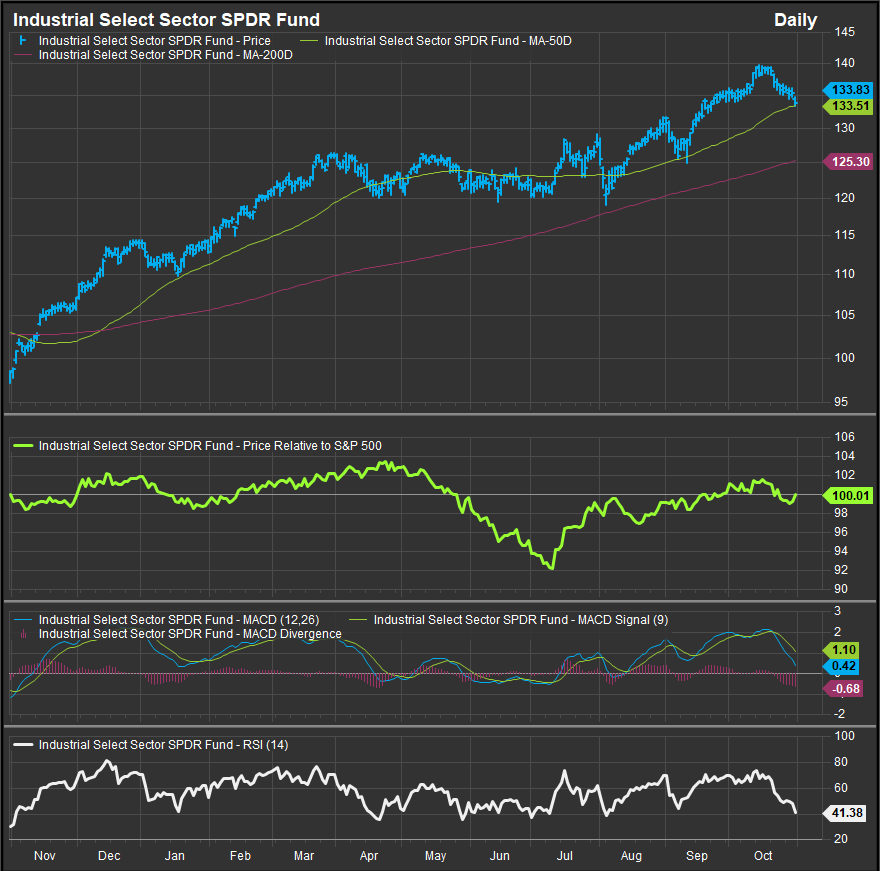

The Industrial Sector, proxied here by the XLI ETF, executed a bullish pivot in early July and has been in a constructive bullish reversal pattern ever since. That said, sustained outperformance has remained elusive for the Sector. Over 6 and 12-month periods Industrials have been just off the pace of the broad market, and even in the near-term we have seen the outperformance trend roll over in the past week after creating some positive separation through Mid-October. While not outright oversold, the Sector ETF has pulled back to its 50-day moving average, which is where buyers stepped in at the beginning of September.

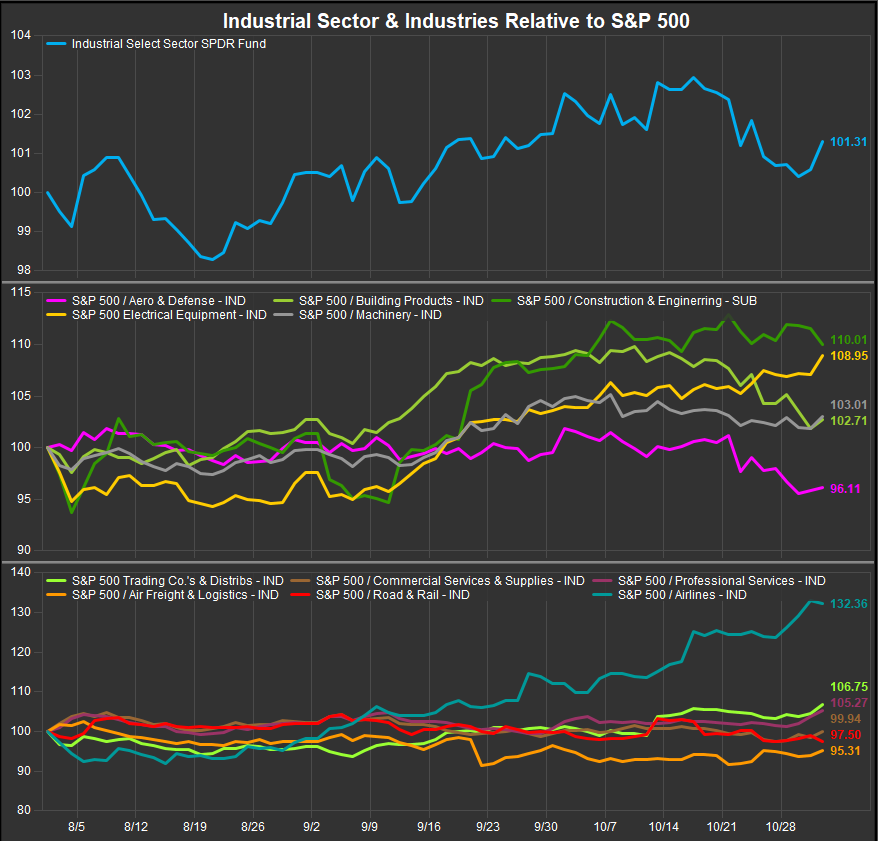

Industry level performance within the sector has improved broadly over the past 3 months with 8 out of 11 GICS sectors outperforming the S&P 500 since August 1, though we’ve seen a profit taking dynamic emerge in the middle of October. Airlines have emerged as a big winner with carriers tightening capacity and hopes that Fed easing will put more money in the Consumer’s pocket. Electrical Equipment, Construction & Engineering, Professional Services (Staffing Agencies) and Trading Co.’s have been outperformers. The key take-away in aggregate is the very broad array of business lines housed within the Industrial Sector. The 11 different industries have varying sensitivities to interest rates, equities and Commodities price trends and typically while one of two industries will be beneficiaries of a given trend, others will be harmed by the same trend. The mix conspires to keep the Sector pretty close to market performance in aggregate.

At the stock level, larger names have been slightly better than smaller ones from a technical perspective, but we are starting to see improvement in the average stock. Our favorite stocks within the Sector are AXON, LMT, HWM, TDG, BLDR, CARR, TT, PWR, ETN, HUBB, MMM, PH, PNR, WAB, CTAS and LDOS.

Economic and Policy Drivers

XLI has faced some macro headwinds from weak commodities prices and falling rates. Historically the sector does better when both are rising. If Commodities prices mean-revert higher, we think that would likely be a tailwind for the sector.

Themes like “onshoring” have benefited the sector as global supply chains have been contracting due to sanctions on Russia and China relating to the war in Ukraine and unfair trade practices respectively. There is also the continued convergence of the Chinese/Russian political block as it seeks to act as a counterweight to US interests globally and press its own agenda on Ukraine, Taiwan, the South China Sea and North Korea. This new geopolitical status quo has boosted the Aero/Defense Industry as well as Building Products stocks, Construction & Engineering stocks and Trading co.’s.

On the fundamental side, supply chain issues continue to crimp margins for many industrial businesses. Manufacturing wages have risen dramatically during the pandemic/post-pandemic cycle despite plateauing Industrial Production. Trade policies and Tariffs are adding to uncertainty with the Geo-Political environment continuing to be fraught with tensions around the “Hot Wars” in the Middle East and Ukraine and the ongoing “Cold War” between the US and China. Finally, theoretically salutary policies like the CHIPS and Science Act and the Inflation Reduction Act which have aimed to reduce reliance on the global supply chain have had some lagged effects which have dampened optimism in the near-term. It appears investors are betting on lower rates to spark increased commercial and industrial lending, as well as ameliorating elevated labor and financing costs. This should set up a ramp for marginal fundamental improvements for the sector moving forward. The complicating factor is that with the “Soft Landing” now consensus, upside bets on “No Landing” are backing up interest rates and undoing the Fed’s policy work.

In Conclusion

A lot of dust needs to settle between earnings and the Presidential Election over the next several days. We remain constructive for now with a modest positive bet on the Industrials Sector.

We remain long XLI on expectations that implementation of Dovish Policy and onshoring tailwinds, however we are trimming the bet given a observable loss of near-term momentum. We start November OVERWEIGHT XLI with a +0.74% allocation above the benchmark S&P 500.

Chart | XLI Technicals

- XLI 12-month, daily price (200-day m.a.| Relative to S&P 500)

- Recent pull back is a test for the bullish reversal that began in July

XLI Relative Performance | XLI Industry Level Relative Performance | T3M

Data sourced from FactSet Research Systems Inc.