The S&P 500 sits just below the 6000 level, up a shade under 31% for the year. Inflation has leveled off and enabled the Fed to focus on boosting the main street economy and investors have moved up the risk curve, dumping bonds for stocks and taking Bitcoin to new all-time highs.

Q3 earnings season is largely in the books with results that were solid but largely uninspiring compared to historical standards. Factset’s “streetaccount” summarized the season as follows:

“…the blended earnings growth rate for Q3 S&P 500 EPS currently stands at 5.8%. This compares to the 4.3% expected at the end of the quarter. The blended revenue growth rate is 5.6%. Of the 95% of S&P 500 companies that have reported for Q3, 75% have beaten consensus EPS expectations, below the 78% one-year average and the five-year average of 77%. In addition, 61% have surpassed consensus sales expectations, below the 62% one-year average and the five-year average of 69%. In aggregate, companies are reporting earnings that are 4.5% above expectations, below than the 5.5% one-year average positive surprise rate and the five-year average of 8.5%. In aggregate, companies are reporting sales that are 1.2% above expectations, better than the 0.8% one-year positive surprise rate but below the five-year average of 2.0%.”

–Factset Earnings Insights Report

Given the 30%+ capital gain in the S&P 500 and earnings that were short of blockbuster levels, investors would be wise to ask if the good news, at least for the time being, is priced in? What are the potential drivers of upside surprise with earnings results now that comparisons are going to get harder to beat?

Our outlook at ETFsector.com is that interest rates need to revere lower to keep the bull trend sustained. Rate relief will be key to the consumer sector which has struggled with the accumulation of rising costs. Near-term price rise reflects optimism that Donald Trump will put policy in place that tackles inflation, but the actual platform he is advocating has several components that are likely to add to inflationary pressure rather than ameliorate it. Tariffs are the obvious one, but his plans to slash regulation are already driving bets on mergers and acquisitions that could result in increased corporate pricing power if effective oligopolies are created from industry roll-ups. This may redound to the benefit of the stock market in the near-term, but it doesn’t offer a clear path to relief for the consumer.

Investors agree, and we’ve seen upwards pressure in the near-term on longer duration bond yields and on the 30yr prime mortgage rate (chart below). This is likely not what the Fed had in mind as an ideal outcome when it announced its initial 50bp cut to the policy rate in September, and if mortgage costs continue to inhibit housing affordability, it could eventually tilt the economy into recession despite the Fed.’s efforts to the contrary.

With enthusiasm for Technology shares waning, investors are placing bets on continued recovery, margin gains and overall fundamental improvement from pro-cyclical sectors like Industrials, Financials, Discretionary and Energy. Economic data from manufacturing has already been registering as contractionary. If the resilient services sector comes under pressure due to deteriorating consumer balance sheets and overall confidence we could be due for a bumpy start to 2025.

Read on as we highlight notable breakouts from the past week and review highlights of Q3, 20224 earnings season.

Patrick Torbert, Editor & Chief Strategist, ETFSector.com

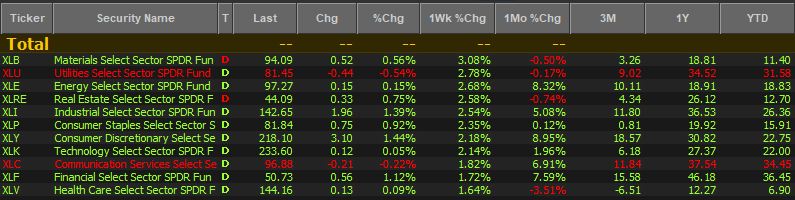

Week in Review: Sectors

The Healthcare sector continues to exhibit weakness while other YTD laggards Real Estate and Materials joined Energy and Utilities in leading the tape for the week. The continued back up in US Treasury Yields has combined with not quite overwhelming results from the Semiconductor space to put a pause on Growth style leadership trends for 2024. Energy, Discretionary and Financial shares have led month-to-date on the back of bullish speculation after Donald Trump won the presidency.

Investors Showing Signs of Exuberance:

With equities near new highs, Bitcoin has broken out from a longer-term base pattern. The current objective has a maximum projected upside of $123,600 while currently trading jut below the $100K level. While we subscribe to the long-term technical projection, we note that price has moved above it’s short term target of $94,000 and is likely to consolidate in the near-term. Those with big notional profits are encouraged to fade new highs.

With Trump’s election win, TSLA is also checking the box for exuberance. With Elon Musk currently entrenched within the Trump Administrations inner-circle, there is clear reason to bet on his interests, but we would advice some caution as automobiles as surely as houses need to be financed and the current interest rate back-drop is a headwind.

Earnings Season Highlights

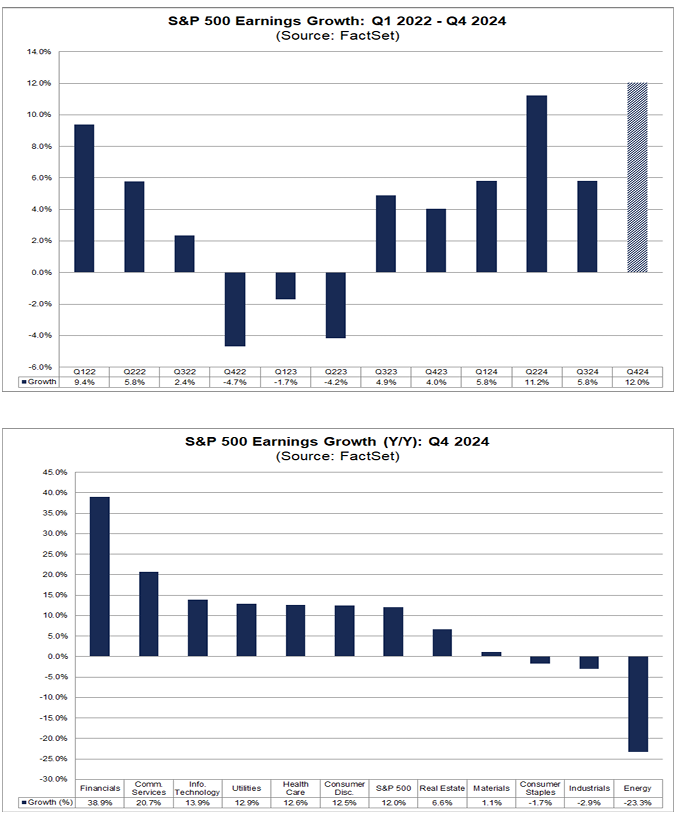

2024 has been buoyed by robust earnings. Q4, 2024 saw 12% growth yoy. At the sector level Financials saw yoy growth of 38.9% while Energy sector earnings contracted 23.3% at the sector level.

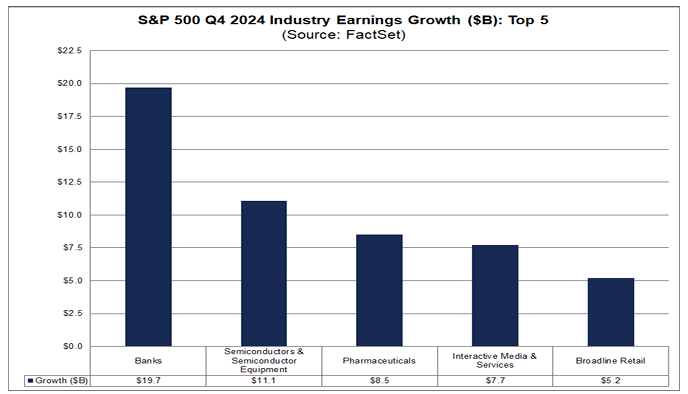

The top 5 industries by earnings growth were as follows:

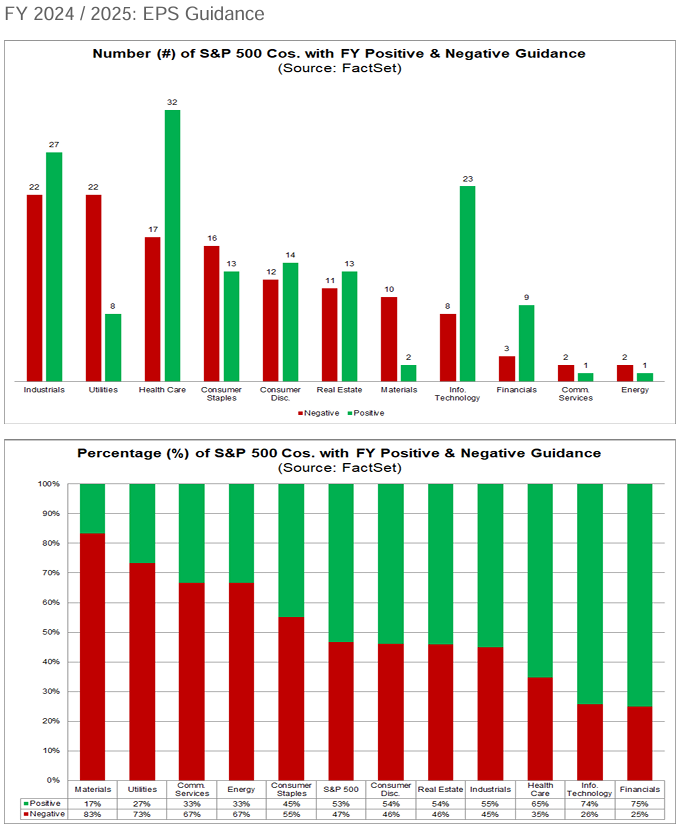

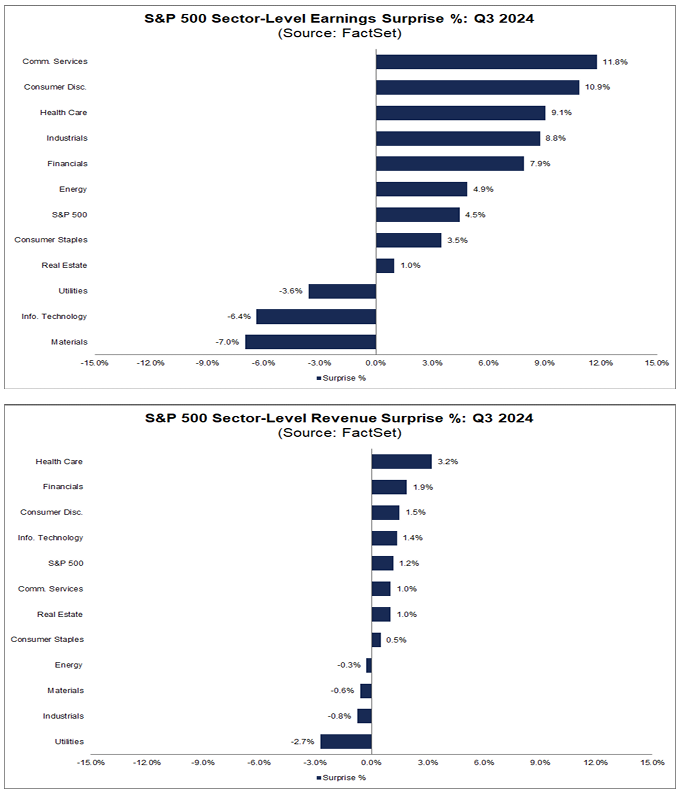

Despite deteriorating performance, the Tech Sector continues to post earnings and revenue results above street estimates.

Financials, Tech and Healthcare also lead in ratio of constituents offering positive vs. negative guidance.

But, Tech has been a victim of its own success showing up on the negative side of the ledger when it comes to quarterly earnings surprise in aggregate vs. expectations. Healthcare ranks high on the list considering its negative YTD performance.

Conclusion

Equities have already had banner results YTD and there is enough momentum present behind bullish themes to carry the cheer into year-end. However, rising rates are becoming a concern, particularly as they relate to the housing market and the strength of consumer balance sheets. AI themes have lost momentum in the near-term, but so far, a hand-off to cyclical sectors has sustained the bull market for equities. We think over the longer-term interest rates will be key to sustaining the bull. We think rates will have to move lower to keep the consumer and the housing market healthy.

Data sourced from Factset Research Systems Inc.