We have been focused on the direction of interest rates over the past month as the election of Donald Trump to a 2nd presidential term has injected some exuberance into the equity market and, for a time, had rates rising concurrently. In the two weeks since we tapped out our last missive on the keyboard, interest rates as proxied by the US 10yr Yield have rolled over and equity investors have responded by rotating into Growth exposures. This is the reference scenario for a falling rate bull market. The question is how long the bull trend can persist without sparking inflation pressures, but while these conditions last, we should be participating.

Perusing the news over the past week, we observed a familiar mix of optimism and anxiety as bullish positioning has invited renewed concerns about inflation. My junior analyst, A.I. Botman, wrote up the weekly economic summary thusly…

“The labor market presented mixed signals this week. Initial jobless claims rose to 224K for the week ending 30-November, above the consensus estimate of 214K and marking the highest level since mid-October. However, continuing claims declined to 1.871M, better than the expected 1.907M, and marked the second consecutive weekly drop. These data points come ahead of the November nonfarm payrolls report, which is anticipated to show a rebound after October’s strike and weather impacts. Meanwhile, the November ISM Services Index fell to 52.1, missing the 55.5 consensus and marking its lowest reading since August. Business activity and new orders declined, though supplier delivery performance improved. The manufacturing sector offered a glimmer of optimism, with the November ISM Manufacturing Index rising to 48.4, above the 47.5 consensus, driven by an improvement in new orders after seven months of contraction.”

–A. I. Botman paraphrasing FactSet StreetAccounts

Whether evaluating interest rates vs. equities, or trends in economic data, the tension between good and bad that keeps us on our toes is a well understood behavioral set up that market technicians refer to as the “Wall of Worry”. The phenomenon exists within the tension between a strong uptrend in the equity markets which is currently in place and the continuing evaluation of all the potential catalysts for bearish trend change. When there are several known bearish catalysts in the financial market zeitgeist like there are today (inflation, high mortgage rates, Middle East fighting, war in Ukraine, trade war with China), the tension between the bullish reality on the ground and the fodder for bearish speculation creates the “Wall of Worry”. This keeps investors bullish but somewhat restrained as bad news acts as a damper on expectations. The result is a more sustainable pace of advance that is beneficial to the bull trend.

We think those conditions are present as we head into year end, and we have the coincident near-term tailwind of December seasonality to give us a little push. Historically, the S&P 500 has delivered an average return of +2.04% in December since 1928, with performance weighted toward the latter part of the month, the “Santa Claus rally.”

Patrick Torbert, Editor & Chief Strategist, ETFSector.com

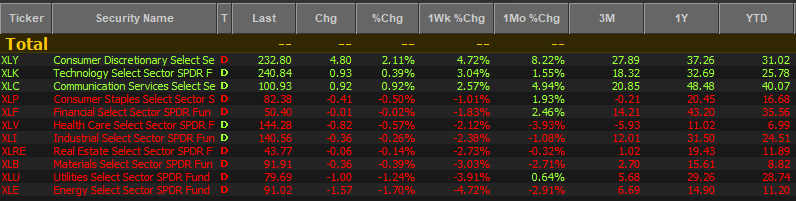

Week in Review: Sectors

The past week has seen sector performance dovetail cleanly with the macro picture as Discretionary, Technology and Comm. Services shares outperformed while defensive sectors and commodities-exposed sectors move lower. We entered December under-exposed to both commodities and defensives as we find the stock-level characteristics to be bearish, particularly for the Healthcare, Materials and Energy sectors, which continue to grade poorly in our work.

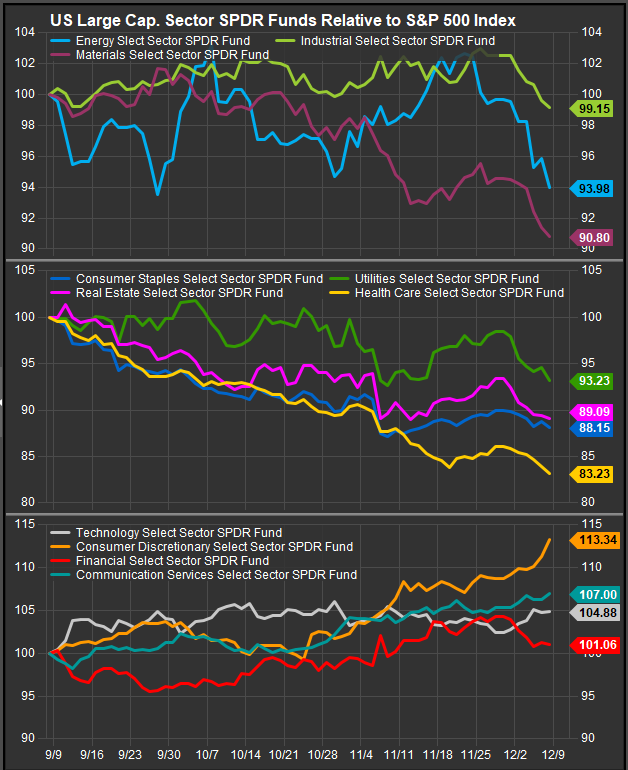

On the bullish side we were uncertain of the direction of interest rates ourselves, but we were certain that lower rates would benefit Discretionary stocks and that has most certainly been the case as the chart below illustrates.

Investors Showing Signs of Exuberance:

In our recent “Tactical Tuesday” serial we highlighted the setup for the ARKK Innovation fund. After a multi-year timeout, investors are embracing concept stocks again. A gap higher on November 14th has kickstarted a bullish breakout. Though currently overbought, we think investors would be wise to accumulate any near-term pullbacks in this nascent uptrend.

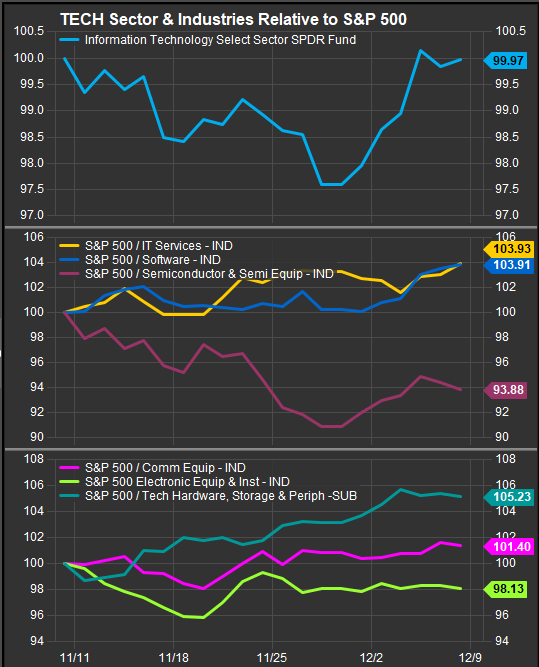

Tech Strength is NOT being led by Semiconductors

The most recent boost for equities has come from the Technology Sector, but intra sector leadership has made a notable change recently. Improvements have been led by Software, Services and Hardware Industries rather than Semiconductors.

A break-out to new YTD highs for the Software Industry is notable, though the bullish reversal is still callow. That said, Growth factor performance we highlighted on Friday, and the break-out in ARKK shares buttresses the case for positive trend change.

Given the macro backdrop of a supportive Fed, ameliorating inflation, some crosscurrents on the horizon for the consumer and for capital spending, we think this is the right environment for Growth to lead.

Meanwhile the SOX Index price action remains lackluster as the index consolidates its gains from the cycle. The price action in the chart below would confirm a top on a move below 4500, but the Index is also still within spitting distance of a potential bullish reversal if buyers push price above the 5315 level.

We think rotation away from Semiconductor leadership is a constructive development for the bull market as it implies progression beyond the bullish catalyst of AI optimism through to a bullish perception of AI boosted operating results. We have been keying on the fact that AI success should benefit a broad array of business lines through efficiency and increased opportunity. As we see investors rotating into a broader range of historical upside exposures, the technical picture is lining up in support of that potential bullish reality.

Data sourced from Factset Research Systems Inc.