COMMENTARY:

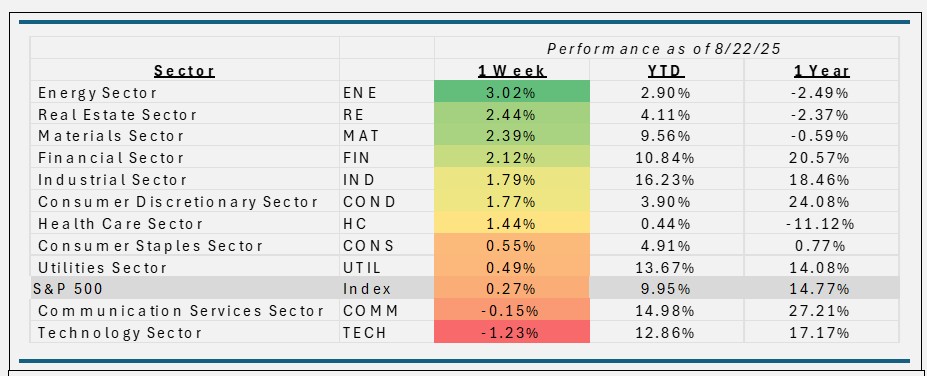

- The S&P 500 surged 1.5% on Friday alone, nearly offsetting midweek losses and finishing up 0.27%. Due to Friday’s Jackson Hole speech by Fed chairman Powell, the markets raised the probability of a rate cut to nearly 90–91% for the Fed’s September. That, combined with solid economic activity and broad-based sector gains, translated into the modest but meaningful gain. Beneath the surface, rate-sensitive sectors and AI stocks led the charge, while inflation pressures linger but were ignored as investors priced in September easing.

- The Energy sector rallied quite significantly this week up 3.0%. Oil prices rose notably during the week in combination of geopolitical uncertainty and stronger-than-expected demand signals. Sector heavyweights—especially integrated energy giants like Exxon (+4.5%), Chevron (+1.0%), and ConocoPhillips (+1.5%) drove most of the gain. Smaller support came from refiners and midstream firms, while equipment names played modest roles.

- Real Estate jumped 2.4%. Powell’s dovish tone and growing rate-cut expectations revived investor interest in rate-sensitive, yield-generating sectors. Also contributing was a tech pullback triggered flow into more defensive and income-oriented parts of the market, with real estate prominently in favor. Stock-level dynamics included gains from ProLogis (+5.3%), Welltower (+1.0%), and American Tower (+2.8%).

- The top seven largest names in the Tech sector were the only constituents in the red, and they represented about 57% of the sector, driving the entire group down 1.2% this week. Those big underperforming names included Nvidia, (-1.4%), Microsoft (-2.5%), Apple (-1.7%), and Broadcom (-4.0%). A combination of sector rotation, valuation concerns, and technical signals that unsettled investors, and caused a shift toward more defensive and income-generating areas of the market.

- This week’s outsized sector returns finally brought all 11 into positive YTD performance. Communication Services is winning, up almost 15%, and Health Care finally in the green sits at a gain of 0.4%.

ETF Tidbits:

- Large-cap and broad-market equity ETFs garnered key gains: The Dow Jones and S&P 500 both hit record highs by Friday, driven by Fed Chair Powell’s dovish tone at Jackson Hole, which reignited hopes of rate cuts starting in September. The Nasdaq pared earlier losses, and the small-cap Russell 2000 also rallied to a 2025 high.

- ETF launches remain prolific: The first half of 2025 saw an all-time high in new ETF launches across the U.S. and Canada—spanning asset classes from crypto to private assets. Emerging “Infrastructure” ETF investing is becoming timely way to potentially generate income, diversify, and hedge inflation.

- Bond-focused ETFs surged as rate-cut hopes intensified, while equity ETFs—especially those tracking small-caps and broader indices—benefited from market rallies. At the same time, tech-heavy ETFs were pressured by rotation and caution, though long-term bullish themes remain.