ETFsector.com is dedicated to helping investors navigate the complexities of the markets and their investment exposures. Our focus is on the S&P sectors, specifically the eleven listed ETFs. Each week, our expert team delivers insights on significant market movers and performance drivers, along with key updates in the ETF landscape.

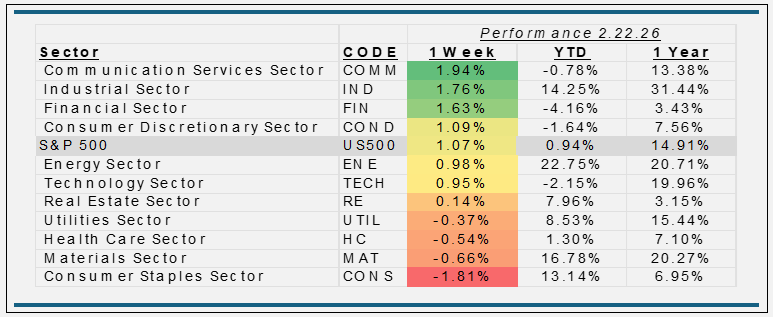

- The S&P 500 climbed about 1% this week as investors absorbed the U.S. Supreme Court ruling overturning broad Trump-era tariffs, easing trade uncertainty and lifting risk assets after a recent downturn. Tech and cyclicals participated despite slowing GDP and mixed economic data, suggesting growth is moderating but still intact. Mega-cap leaders like outpaced peers as AI optimism returned, helping drive breadth north.

- The Communications led sector gains, up about 1.9%, with media and ad-linked stocks benefiting from the broader risk-on sentiment and tariff relief news. Big internet names like Alphabet and Meta rallied in response to policy clarity and renewed ad spending confidence, while streaming stocks also lifted on subscriber growth prospects. Mixed macro data took a back seat as rotation favored high-growth communications.

- Industrials rose roughly 1.8% as economically sensitive areas regained favor, reflecting improved transport and manufacturing sentiment. Expectations the Fed may cut rates later this year supported capital-goods and infrastructure-linked names, while tariff clarity eased input cost fears. Strength in cyclicals showed investors are more comfortable extending rallies beyond growth names.

- Financials bounced back about 1.6% as bank and insurance stocks regained traction on firm yields and stable lending conditions. With labor data still solid and rate-cut expectations creeping in, investors rotated back into value-oriented financials after recent underperformance. Big bank names like JPMorgan and Bank of America helped buoy sector returns.

- Consumer Staples lagged, down about 1.8% as investors favored risk assets and cyclicals over defensive names in a risk-on week. Defensive staples like grocery and household stocks underperformed amid soft consumer demand signals and higher input costs, making them less appealing relative to sectors tied to growth and trade optimism/

- Bottom Line: Relief from trade policy uncertainty and rotation back into cyclical and growth names drove broad market gains this week, with communication, industrial and financial sectors outperforming while defensive staples lagged