COMMENTARY:

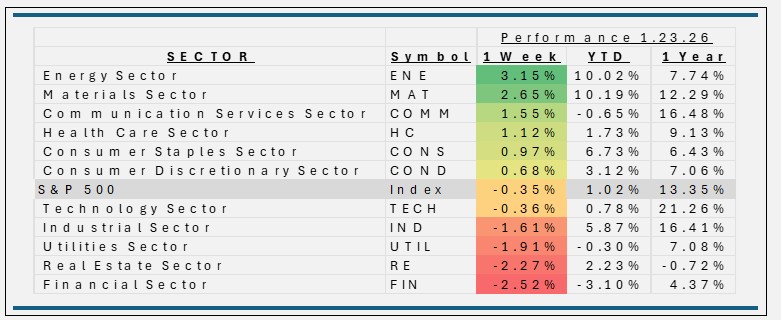

- The S&P 500’s slight decline of 35 basis points reflects a market grappling with conflicting signals: geopolitical uncertainty and a major tech earnings disappointment on one side, and resilient pockets of growth and late‑week stabilization on the other. While risk sentiment softened, the underlying market tone remains constructive, with investors selectively leaning into opportunities as volatility persists.

- Energy’s strong performance this week reflects a constructive backdrop for energy markets, supported by firmer commodity prices, weather‑driven demand, and a rotation toward real assets. While volatility remains elevated across broader markets, the Energy sector continues to benefit from solid cash generation, disciplined capital spending, and supportive supply‑demand dynamics. Exxon Mobil (XOM) – Strong crude pricing and resilient downstream margins helped lift the sector’s largest weight. Chevron (CVX) – Benefited from both oil strength and improved sentiment around global LNG markets. ConocoPhillips (COP) – Outperformed on higher natural gas prices and favorable production mix.

- Materials took second place due to a constructive backdrop for commodity‑linked equities, supported by firmer metals pricing, resilient construction activity, and a rotation toward real assets. While macro uncertainty remains elevated, the Materials sector continues to benefit from global demand stabilization, disciplined supply, and supportive commodity trends. Linde (LIN) – Strength in industrial gases and steady demand across end markets supported gains in the sector’s largest weight. Sherwin‑Williams (SHW) – Benefited from resilient construction activity and improving coatings demand. Freeport‑McMoRan (FCX) – Rose alongside higher copper prices and improving global metals sentiment.

- This week’s weakness in Financials, which fell 2.5% this week reflects a market leaning toward caution. Lower interest rates, mixed earnings, and geopolitical uncertainty all played a role. While the sector remains tied to the direction of the economy and interest rates, many investors are taking a “wait‑and‑see” approach as the broader outlook evolves. JPMorgan (JPM) – Lower yields and cautious loan‑growth commentary weighed on the stock. Bank of America (BAC) – Sensitive to interest‑rate moves, and consumer trends were softer. Wells Fargo (WFC) – Higher credit‑loss provisions and weak mortgage activity pressured shares