March 16, 2025

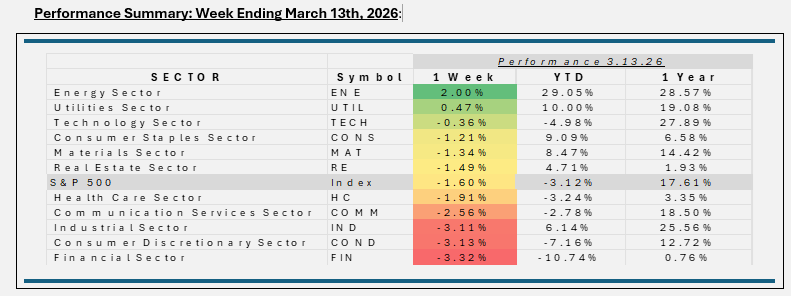

- The S&P 500 fell 1.6% for the week ending March 13, 2026, as investors contended with higher for longer interest rate expectations, renewed inflation concerns driven by surging oil prices, and persistent geopolitical tensions centered on the conflict in Iran. Wall Street’s third straight week of losses, the S&P 500’s slide to fresh year to date lows reinforced a risk off tone that weighed on cyclical and growth sectors throughout the week.

- Energy was the standout sector, gaining 2.0% as oil’s rebound above 100 dollars per barrel improved earnings sentiment for producers and integrated majors leveraged to higher crude realizations. The sector benefited from expectations that ongoing disruptions around the Strait of Hormuz and uncertainty over Iranian supply would keep global inventories tight, supporting commodity prices and cash flow visibility.

- Utilities, the only other sector to end in positive territory, inched higher by about 0.5% as investors sought relative safety in regulated, income-oriented businesses amid elevated volatility. This week’s modest gain came from a handful of large regulated electric and multi utilities whose scale, yield characteristics, and defensive profiles made them favored destinations during the risk off rotation.

- Financials were the weakest space, with the sector declining 3.2% as markets reassessed the path of policy easing and the implications of higher energy driven inflation for funding costs, net interest margins, and credit risk. A slower than anticipated pivot by the Federal Reserve raised concerns that banks will face extended deposit competition and elevated short-term rates, while macro uncertainty weighed on capital markets linked revenues across brokers, asset managers, and investment banks. The bulk of the downside came from its largest money center and universal banks and major payment networks, whose earnings sensitivity to both the rate environment and overall risk.

- Consumer Discretionary also fell 3.2%, pressured by worries that higher energy prices and lingering inflation could erode real household incomes and limit spending on non-essential goods and services. Sector level weakness was dominated by a small group of mega cap discretionary and platform stocks whose outsized weights meant broad based de rating in this cohort overshadowed more mixed results among traditional retailers, autos, and leisure companies.

- U.S. equities delivered a distinctly risk off week reflecting the market’s struggle to balance still solid economic activity against resurgent energy driven inflation and a less dovish Fed backdrop. Leadership narrowed to Energy and a sliver of defensive Utilities, while Financials and Consumer Discretionary bore the brunt of higher yields, geopolitical uncertainty, and concerns about the consumer and credit cycle.

ETF Tidbits:

For the week ending March 13, 2026, the U.S. ETF landscape was shaped by:

- Steady regulatory pressure (especially for complex and crypto products) but no new rulemaking.

- Flows favoring defensive assets (GOLD) and tactical small‑cap and international allocations.

- Crypto ETFs showing net‑positive flows as Bitcoin stabilized.

- A healthy pipeline of new ETF launches, especially in thematic, income, and digital‑asset categories.