COMMENTARY:

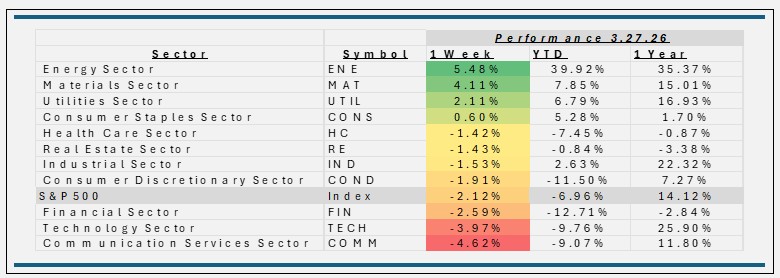

- The S&P 500 declined -2.1% for the week ending March 27, 2026, as markets faced renewed pressure from rising interest rates and persistent inflation concerns. Stronger-than-expected economic data pushed Treasury yields higher, reinforcing expectations that the Federal Reserve may keep policy restrictive for longer. At the same time, a notable rebound in commodity prices—particularly in energy—drove sharp performance divergence across sectors, with cyclical and resource-oriented areas outperforming while growth sectors lagged.

- Energy was the top-performing sector, gaining 5.5% for the week. The advance was driven by a sharp rise in crude oil prices amid tightening global supply and ongoing geopolitical uncertainty. Large integrated companies such as Exxon Mobil and Chevron were key contributors, benefiting from stronger earnings expectations and robust cash flow outlooks. Exploration and production companies also added to gains, as higher oil prices directly supported revenue growth. The sector’s performance reflects its leverage to commodity prices and its role as a hedge during inflationary periods.

- Materials also delivered solid gains, rising 4.1% over the week. Strength was led by metals and mining companies, supported by higher prices for key commodities like copper and gold. Freeport-McMoRan contributed on improving copper demand expectations tied to global infrastructure and electrification trends, while Newmont advanced as gold prices strengthened, attracting investors seeking stability. Broader optimism around fiscal spending and resilient industrial activity further supported the sector’s positive performance.

- Communication Services was the weakest-performing sector, declining -4.6%. Losses were concentrated among large-cap digital advertising and platform companies such as Meta Platforms and Alphabet, which faced pressure from rising interest rates and some softening in advertising outlooks. Higher bond yields weighed on valuations, particularly for growth-oriented companies with longer-duration earnings profiles. Additional weakness in media and streaming names, driven by competitive pressures and profitability concerns, further contributed to the sector’s decline.

- Technology also moved lower, falling -4.0% for the week. The sector was pressured by the same rise in interest rates, which led to multiple compression across many high-growth names. Apple, Microsoft, and NVIDIA were among the largest detractors, despite relatively stable fundamentals. While long-term growth drivers remain intact, the sector continues to face near-term headwinds as investors rotate toward more cyclical areas of the market.

- Overall, the week underscored a continued shift in market leadership, with strength in commodity-linked sectors offset by weakness in growth-oriented areas as investors navigate an evolving macroeconomic backdrop.