COMMENTARY:

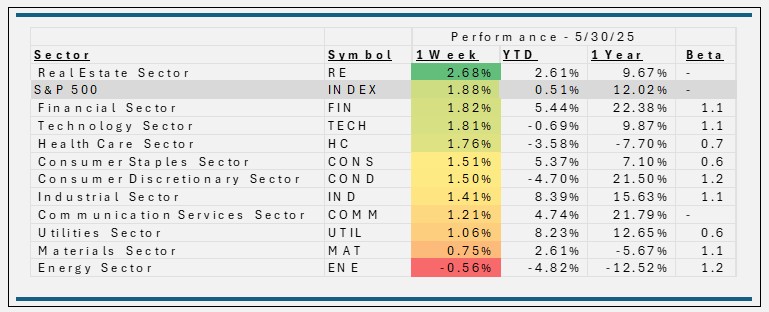

- The S&P 500 delivered a strong performance this week, climbing 1.9% as investor sentiment remained upbeat amid robust earnings from several tech giants and continued optimism about the economic outlook. Notably, the largest S&P 500 constituents—Alphabet, Microsoft, and Nvidia—were key drivers, with Nvidia maintaining momentum from sustained AI demand and Alphabet benefiting from strong digital advertising trends. The index’s advance was supported by expectations of steady GDP growth and cooling inflation, which bolstered confidence in corporate profit growth through the remainder of 2025.

- Real estate equities outperformed, rising 2.7%. This gain was underpinned buoyed by resilient consumer spending and low vacancy rates, increased debt availability, and slowing construction pipelines, which are expected to tilt supply-demand dynamics in landlords’ favor. Thirty of the thirty-one constituents were in the green this week. Host Hotels & Resorts and Essex Property were both up 5.4% and the top two performing names.

- Financials advanced 1.8%. The sector benefited from higher noninterest income and improved asset quality, as well as a modest uptick in loan growth and strong capital positions across major banks. Aon (+4.4%), Mastercard (+3.9%) and Chubb (+3.9%) were the top performers for the week.

- Conversely, the Energy declined by 0.56%, reflecting softer oil prices and sector-specific headwinds. constrained by weak oil prices, oversupply concerns, and cautious investor sentiment. Texas Pacific Land Co. fell 12.5% for the week. Other under-performers for the week included Devon Energy (-2.9%) and Schlumberger (-1.8%).

ETF Tidbits:

- US spot Bitcoin ETFs experienced major outflows totaling $616.1 million on May 30, 2025. This ended a 31-day inflow streak and reflected a shift in market sentiment, with analysts attributing the move to long-term holders rather than retail panic.

- Prior to the week ending May 30, ETFs saw robust net issuance. For the week ending May 21, estimated net ETF issuance was $20.61 billion, highlighting continued demand for these products as tools for both broad market and targeted sector exposure.

- The ETF industry continued to expand its product lineup, with 23 new digital asset ETPs launched globally in April alone. This trend highlights the market’s appetite for specialized and innovative investment products, including those focused on alternative assets and niche strategies.

- Investors continued to favor active ETFs and low-cost index-tracking products, with both categories capturing the majority of first-quarter inflows. This shift reflects a broader move away from mutual funds and into more flexible, tax-efficient ETF structures.