COMMENTARY:

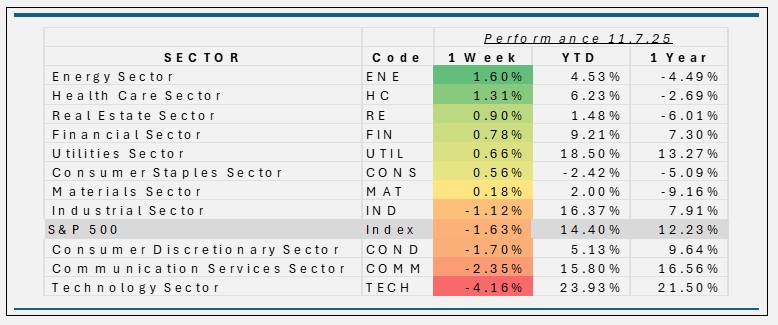

- The S&P 500 index fell 1.6% for the week ending November 7, 2025, with the decline primarily driven by a sharp sell-off in technology and AI-related stocks, concerns over high valuations, and macroeconomic uncertainty amplified by the ongoing U.S. government shutdown, the longest in history limited the availability of official economic data, heightening investor caution and making the macro backdrop more uncertain.

- Energy won the week with a 1.6% gain, driven by rising crude oil prices following an unexpected draw in U.S. inventories and escalating geopolitical tensions in the Middle East. Investors favored energy stocks as safe havens amid increased market volatility, policy uncertainty from the U.S. government shutdown, and expectations for stronger Q1 2026 earnings as oil supply concerns mount.

- Tech and AI Valuation Reset: The sector fell 4.2%. Major technology and artificial intelligence infrastructure stocks such as Nvidia, Broadcom, Microsoft, AMD, and Palantir experienced significant declines, with investors worried about “sky-high valuations” and the risk of a bubble in AI names despite strong earnings.

- Communications services fell 2.4%, mainly due to heavy selling in leading social media, streaming, and digital advertising stocks as investor risk appetite waned and market volatility increased. Coupled with advertising revenue softness, negative guidance from key industry players, investors rotated out of higher-beta stocks amid market uncertainty. Meta (-4.1%) and Alphabet (-0.8%) make up also a third of the benchmark and had the largest negative impact.

- Year to date, all but one sector is sitting on gains. Although this was an off week, Technology has a robust 23.9%, which is 5% more than the second-place sector Utilities. Consumer Staples has lost about 2.4% YTD, as companies continue to navigate the unknown impact of the tariffs.