COMMENTARY:

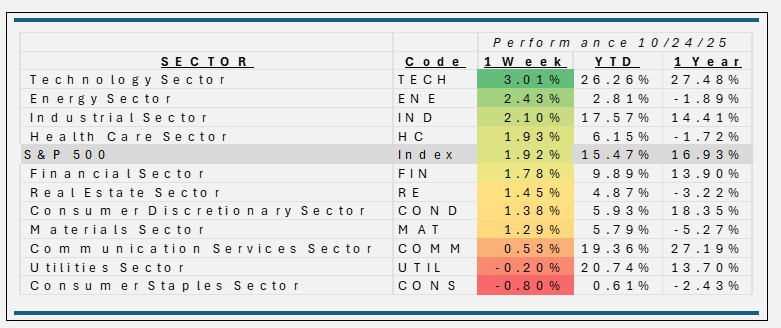

- This week’s S&P 500 rally (+1.9%) was driven by a robust start to the Q3 Earnings Season: so far 29% of S&P 500 companies had reported earnings, with a higher-than-average percentage beating analysts’ expectation. Both the magnitude of earnings surprises and the rate of positive surprises exceeded 10-year averages. The index marked its ninth consecutive quarter of year-over-year earnings growth, reinforcing investor confidence in corporate profitability.

- Technology rose 3% for the week driven by strong earnings from mega-cap tech stocks like Microsoft (+2.0%), Apple (+4.2%), and NVIDIA (+1.7%), alongside easing rate hike fears and upbeat consumer data. Headlines this week included: Q3 Earnings Strength: Tech earnings continued to beat expectations, with strong revenue growth and optimistic forward guidance across cloud, AI, and consumer tech. Consumer Resilience: Retail sales and consumer sentiment data came in stronger than expected, supporting demand for tech products and services.

- Energy gained 2.4%, helped by strong earnings from oil majors, rising crude prices, and geopolitical tensions that supported energy demand and pricing. ExxonMobil (+2.8%), Chevron (+1.6%), ConocoPhillips (+1.8%), were included in strong Q3 earnings and upbeat guidance, supported by higher refining margins, tightening global supply and strong demand forecasts. Geopolitical unrest in oil-producing regions raised concerns about supply disruptions, boosting energy prices and investor interest in the sector.

- Consumer Staples was off by 80 basis points and was the worst performing sector this week. Weak earnings along with cautious consumer spending data weighed on the sector. September retail sales data showed signs of slowing discretionary spending, raising concerns about staples demand. Procter & Gamble (+0.7%): Shares slipped after reporting flat volume growth and margin pressure due to higher input costs. PepsiCo (-1.4%): Fell after missing revenue expectations, citing soft demand in North America. Walmart (1-.5%): Pulled back slightly despite solid earnings, as investors rotated out of defensive names.

- Year-to-date all eleven sectors have positive returns with Technology in first place returning 27.5% and Consumer Staples at the bottom, with about 60 basis pointS of return so far this year. The overall S&P500 Index sits at 15.5% and ride on continued earnings strength and AI momentum could propel further gains, but macro risks and policy shifts may introduce volatility.