February 25, 2026

Nvidia’s earnings report arrives at a critical inflection point for the AI investment cycle. The company remains the primary beneficiary of hyperscaler infrastructure spending, and the market’s response will hinge not merely on quarterly results, but on what management signals about durability, capital intensity, and long-term return on capital.

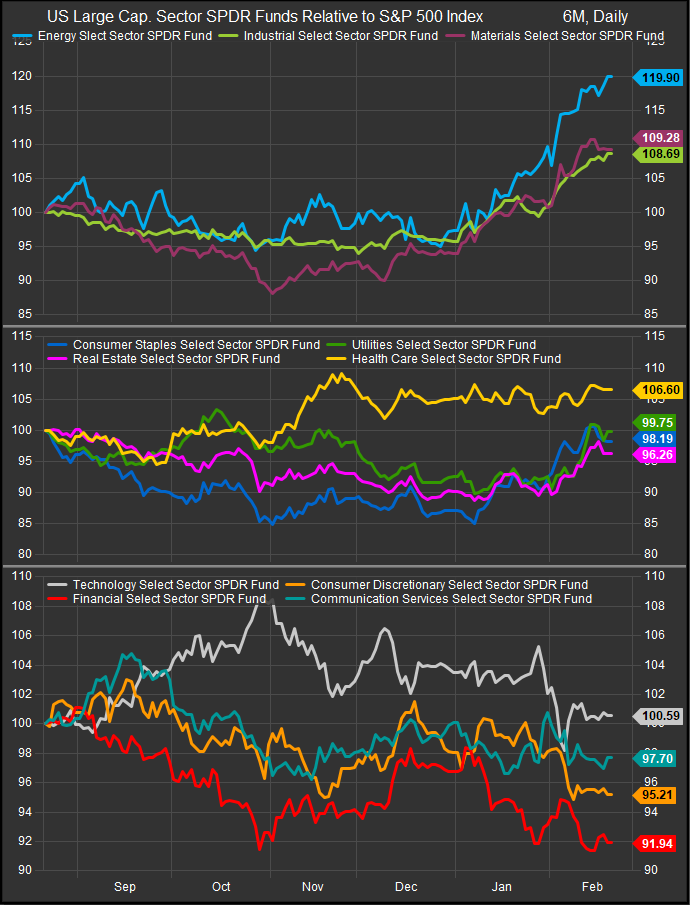

Over the past 6-months, investors have been in clear rotation towards “real” assets. Technology and Comm. Services sectors have moved generally sideways relative to the index over that time frame, but more pessimistic AI scenarios have been discounted since late October.

The Bull Case: Demand Remains Structural, Not Cyclical

Our analysis and reporting from Reuters, Axios, Barron’s, and S&P Capital IQ indicate that AI capital spending remains historically elevated and is still accelerating. Reuters, citing Bridgewater research, reports that Alphabet, Amazon, Meta, and Microsoft are expected to invest roughly $650 billion in AI infrastructure in 2026, up from approximately $410 billion in 2025 — a scale that suggests expansion rather than digestion.

Per Axios, Nvidia stands directly at the receiving end of that spending wave. In its earnings preview, Axios writes:

“For Nvidia, much of that cash is coming in the form of purchases of Blackwell, the most advanced chips it currently sells. Investors will be scrutinizing details about Blackwell orders, both past and future, and guidance on its next-gen platform, Vera Rubin.”

Consensus projections remain formidable. Per S&P Capital IQ (as cited by Axios), analysts expect quarterly revenue of $66.2 billion and net income of $35.8 billion, both potential company records.

Per Axios, RSM Chief Economist Joe Brusuelas framed the macro implications this way:

“Capex intentions by the large technology firms exceeded expectations for 2025 by an unusual order of magnitude… Should reality match planned outlays, this strongly implies upside risk to the consensus 2.2% estimate of GDP for the upcoming year.”

He added:

“Should productivity-enhancing investment arrive close to planned capex outlays, that would imply another year of robust increases in productivity.”

In this framing, Nvidia is positioned not merely as a cyclical semiconductor supplier, but as the central hardware engine of a productivity-driven capital cycle.

The Bear Case: Capital Intensity, Cash Flow Compression, and Cycle Risk

The counterargument is not that AI spending is insufficient — it is that it may be too aggressive and increasingly funded in ways that pressure equity valuations.

Per Reuters, Bridgewater describes the AI boom as entering a “more dangerous phase” as infrastructure buildouts accelerate and reliance on external financing grows. Elevated capex can compress free cash flow and reduce buybacks — historically a major support for large-cap technology multiples.

Per Barron’s, projected AI spending in the $600–$650 billion range is expected to significantly pressure free cash flow at several hyperscalers. Barron’s notes that free cash flow “is expected to take a massive hit this year” as capital intensity rises.

Per Axios, recent viral debate around potential AI-driven economic disruption underscores heightened investor sensitivity to downside scenarios. While Axios cautioned that “there are plenty of questionable assumptions” embedded in extreme forecasts, the episode reflects growing concern about labor displacement, credit risk, and second-order demand effects.

In this framework, Nvidia could beat expectations and still see muted upside if investors interpret the results as reinforcing unsustainably aggressive capital deployment across the ecosystem.

Positioning Implications for Sector Investors

For sector allocators, Nvidia’s report should be viewed as a signal about the durability of the AI capital cycle rather than a single-quarter event. If Nvidia confirms accelerating Blackwell demand and reinforces multi-year visibility, semiconductor-focused vehicles such as SMH or SOXX remain direct beneficiaries of sustained infrastructure buildout.We think investor reaction will be a “tell” on overall risk appetite. With interest rates moving lower in the near-term, a strong print and guide should rally the stock. If it doesn’t move the needle positively it may be a sign of buying exhaustion.

If guidance emphasizes capital intensity risks, slower outer-year growth, or margin pressures, investors may consider increasing exposure to:

-

Large-cap technology with stronger free cash flow conversion

-

Dividend growth and quality strategies (continued rotation towards lover vol. sectors like Utilities, Staples and Real Estate

-

Industrial and infrastructure beneficiaries of data center buildout with less valuation sensitivity

In a market where capital spending is surging while rates remain elevated, the most effective positioning may be a barbell: maintain core exposure to AI infrastructure leaders while balancing portfolios with durable cash-flow sectors.

Nvidia’s earnings will not resolve the AI debate. But they will clarify whether this remains a structurally compounding productivity cycle with strong investor demand — or a capital allocation test for the largest companies in the world.

Sources

Reuters

Axios

Barron’s

S&P Capital IQ