US equities ended off worst levels of the day grinding out a mixed result with the Tech-heavy Nasdaq pacing Large cap stocks up +59 bps with the S&P +2bps and the Dow off -55bps on disappointing news from AMGN and MRK. Crude and Gold prices rose as the Fed continues to signal a probability of more interest rate hikes with Governor Kashkari the latest to adopt a somewhat hawkish tone in his comments.

As of this writing Wednesday’s futures are generally positive with the S&P 500 and Nasdaq up slightly and the Russell 2000 showing a small decline.

Eco Data Releases | Friday May 29th, 2024

| Date Time | Event | Period | Survey | Actual | Prior | Revised |

| 05/29/2024 07:00 | MBA Mortgage Applications | 24-May | — | — | 1.90% | — |

| 05/29/2024 10:00 | Richmond Fed Manufact. Index | May | -6 | — | -7 | — |

| 05/29/2024 10:00 | Richmond Fed Business Conditions | May | — | — | -6 | — |

| 05/29/2024 10:30 | Dallas Fed Services Activity | May | -9.4 | — | -10.6 | — |

| 05/29/2024 14:00 | Federal Reserve Releases Beige Book |

S&P 500 Constituent Earnings Announcements by GICS Sector | Friday May 29th, 2024

CRM is on the docket to report after market on the 29th with the software industry in need of a win during what has been a somewhat disappointing start to 2024. Rising rates, fears of slowing sales growth, and worries about longer-term prospects of B2B subscribers are taking some luster off the industry. It is also being crowded out by the relentless focus on AI and investors rushing to get “picks and shovels” exposure through buying semiconductors stocks and funds.

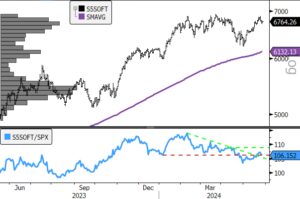

- CRM (200-day m.a.| Relative to S&P 500)

- CRM is showing a negative relative strength divergence breaking to new YTD lows while price consolidates. The longer-term bull market trend gets the benefit of the doubt above the $227 level, but software is a headwind to the XLK at present.

- S&P 500 Software Industry (200-day m.a.| Relative to S&P 500)

- The Industry chart is in better shape than the CRM chart, but has deteriorated from a “Strong Buy” to a “Neutral” chart from a technical perspective.

World-Wide Wednesday:

This week we will take a look at MSCI EAFE country performance. The steadiest trends over the past 12-months belong to Japan, Denmark, The Netherlands and Italy. The core of the EU (France & Germany) are a shade under the EAFE benchmark on performance while the weakest areas of developed market equities are Hong Kong, Portugal, Finland and New Zealand.

Source: Bloomberg