The S&P 500 finished Wednesday flat while the Dow was up 44bps and the Nasdaq was off -10bps. Thursday features monthly initial jobless claims and continuing claims releases before the bell. With the 10yr yield at a near-term oversold level below 4.5%, it will be interesting to see the reaction from the bond market to the claims data.

Earnings season wrapping up with roughly 90% of S&P 500 constituents reporting with average earnings surprises across sectors coming in at > +8%. The cross current is expected to come from rates/inflation triggered by strong economic growth and tightening supply for goods and services. So, there’s potential for strong prints to be faded by the market.

Eco Data Releases | Thursday May 9th, 2024

| Date Time | Event | Survey | Actual | Prior |

| 05/09/2024 8:30AM | Initial Jobless Claims | 212K | — | 208K |

| 05/08/2024 8:30AM | Continuing Claims | 1782K | — | 1774K |

S&P 500 Constituent Earnings Announcements by GICS Sector | Thursday May 9th, 2024

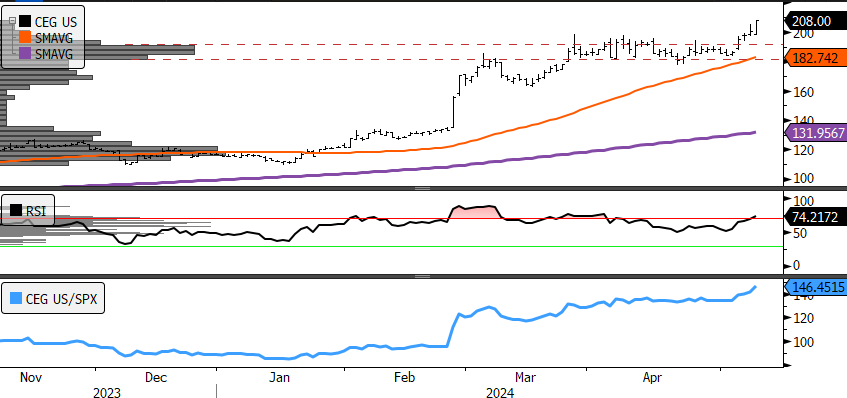

A generally laggard group on the docket for Thursday with CEG (Utilities Sector) the lone YTD stand out up +77%. Bloomberg reports earnings are set to surge for the Utilities concern. Will be interesting to see how much of the good news has been priced in by the recent surge. Utilities have firmed at the sector level and have been a top 3 sector performer in 2024.

- CEG (50-day, 200-day) has been in a strong uptrend since the advent of 2024, outperforming the S&P 500 by +46% over the past 6 months

- Near-term support is $182-190 and a potential accumulation opportunity on a pull-back

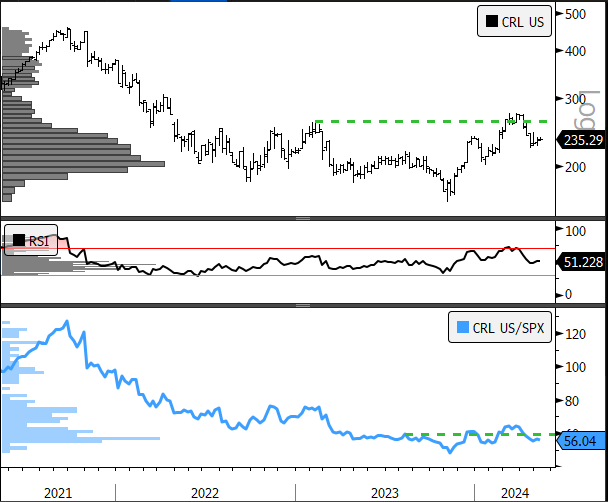

Among the other releases, CRL (Healthcare Sector) is the most interesting on the list from a technical perspective with the chart showing nascent bullish reversal (if you squint really hard!). Looking for follow-through above the March highs to get excited.

- CRL (Relative to S&P 500 ) The earnings release comes at a time when the stock is near-term oversold after breaching longer-term resistance in March. A sustained move above $260 projects upside to $340

Thematic (ETF) Thursday

Surveying Bloomberg’s 153 “Thematic” ETF’s we see that Cannabis remains a YTD leader. Some notable wins in the legislative arena no doubt fuel the speculation, but the chart is not showing the kind of momentum signature that typically front runs strong price appreciation. Using MSOS (Advisorshares Pure US Cannabis ETF) as an example:

- MSOS (50-day, 200-day) price has made new highs in 2024, but more work needs to be done

- Momentum (RSI, middle panel) has been showing negative divergence despite positive relative performance over the past 6 months