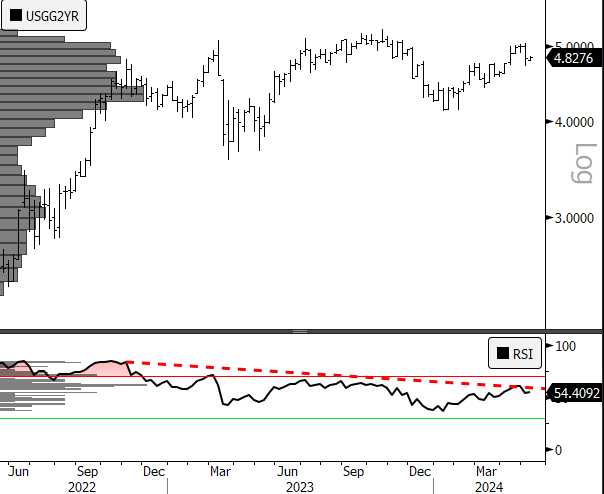

Thursday saw equities continue to build value as rates edge lower. The Dow paced the major benchmarks at +85bps while S&P 500 added +51 bps and the Nasdaq Composite lagged at +27 bps. Legacy defensive sectors led the tape as bottom-fishing the Real Estate Sector (e.g. XLRE) has been a theme in May. EQIX popped >+10% and was a halo to the sector. Initial and continuing unemployment claims ticked up yesterday and investors responded by moving to higher yielding areas of the equity market. Charts of the US 2yr and 10yr yield are starting to look “toppy” as upside momentum has continued to trace out a negative divergence for the yields over a multi-year period.

Eco Data Releases | Friday May10th, 2024

| Date Time | Event | Survey | Prior |

| 05/10/2024 10:00 | U. of Mich. Sentiment | 76.2 | 77.2 |

| 05/10/2024 10:00 | U. of Mich. Current Conditions | 79 | 79 |

| 05/10/2024 10:00 | U. of Mich. Expectations | 75 | 76 |

| 05/10/2024 10:00 | U. of Mich. 1 Yr Inflation | 3.20% | 3.20% |

| 05/10/2024 10:00 | U. of Mich. 5-10 Yr Inflation | 3.00% | 3.00% |

| 05/10/2024 14:00 | Monthly Budget Statement | $250b | $176.2b |

S&P 500 Constituent Earnings Announcements by GICS Sector | Friday May10th, 2024

No Earnings Releases Today

- US 2yr Generic Treasury Yield has seen a negative momentum divergence (panel 2) over the past 2 years. Typically this is part of a distributional or topping pattern and sets up a contrast to the tone from the Fed

- EQIX (50-day, 200-day) popped on a smaller than expected miss on the quarter. Stock had sold off almost 40% from highs in early march, follow through is key as price is currently at resistance

Factor Friday

Each Friday we will be taking a look at some of the most popular factor investing strategies and their performance over varying time periods with a focus on how they relate to sector investing.

Size & Style Factors

We’ll be starting out with a look at the Market Cap. Tiers as defined by the Russell Co’s. The sector investor can generally take advantage of a correction in Growth by going underweight their Large Cap. Tech Sector, Discretionary Sector and Comm Services Sector exposures (e.g. XLK, XLY, XLC) as those sector have high concentrations of Growth stocks. Value has generally been represented by Energy Sector, Financial Sector, Materials and Industrials Sectors (e.g. XLE, XLF, XLB, XLI). Sector ETF’s in general offer a dynamic and cost effective way to tailor exposure to these factors given the different compositions and companies within.

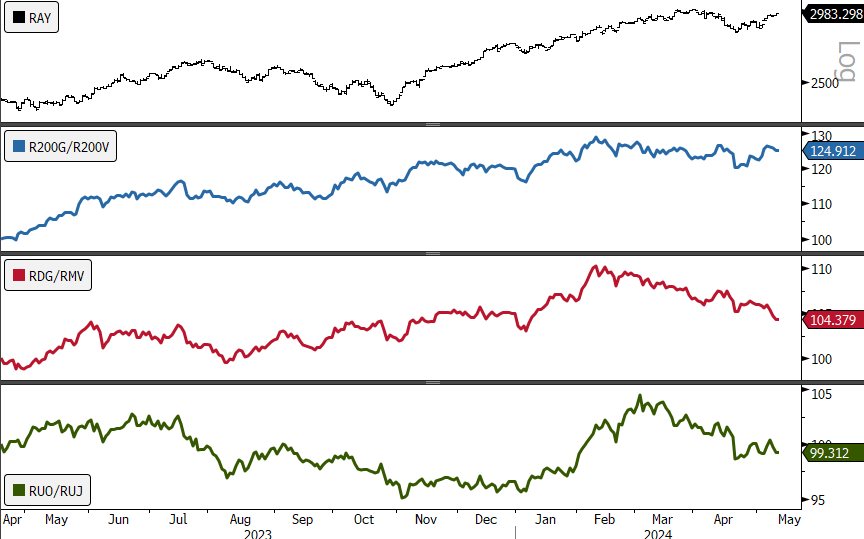

- RAY Index (Russell 3000) is showing near-term bullish reversal after it’s March/April correction

- Russell Mega Cap. Growth (R200G) has outperformed Mega Cap. Value (R200V) during the rally

- Mid Cap. Growth (RDG) has continued to lag despite near-term buying

- Small Cap. Value remains in the driver’s seat as well since Growth peaked in March

Volatility and Momentum Factors

Looking at the ratio of the Invesco S&P 500 High Beta ETF to Invesco S&P 500 Low Volatility ETF we see investor preference for high beta weakening despite broad market prices rising in the near-term. As one would expect given the preference for min vol., momentum stocks are also underperforming. Based on the charts today, the takeaway is investors are skeptical of peak-growth pricing and absent a new catalyst (looking squarely at NVDA earnings, 5/22 here) there could be some prolonged rotation away from Growth leadership.

- S&P 500 with the Relative Performance of Invesco High Beta/Low Vol (panel 2) and Relative Performance of ishares MSCI Momentum ETF vs. S&P 500