ETF Insights | January 1, 2025 | S&P 500

Price Action & Performance

The S&P 500 couldn’t sustain positive momentum in December as the index has delivered a return of -1.97% as of this writing. Per the price chart below, we see important support for the index between 5669 and 5763. Above that range we remain confident in the bull. Oscillator work on the chart has flipped from overbought to oversold on the RSI study as December progressed while the MACD study is showing a near term sell signal.

For the time being, we interpret year-end weakness as tax loss selling and we expect the institutional crowd will be looking to accumulate recent weakness when they return from their vacations on January 2.

S&P 500 Breadth at “Wash out” Level

Internal strength as measured by the percentage of stocks above their 50-day moving average has collapsed to levels where we’ve seen bullish pivots during this longer-term bull cycle. Currently the reading shows only 18% of stocks above their respective 50-day moving averages. The only times that figure has been lower in the recent past were April 2023 and October/November 2023. Both ended up being accumulation signals for equities.

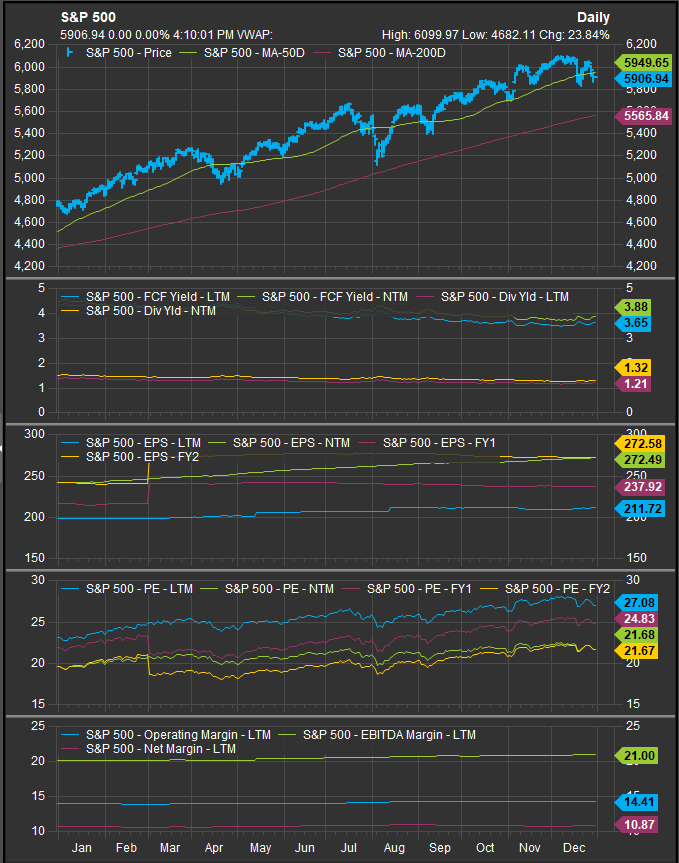

S&P 500 Fundamentals

The chart below shows S&P 500 FCF yield and Dividend Yield as well as projected earnings over the next 3 years, valuation and trailing margins. FCF Yield has not kept up with price but is expected to grow around 10% over the next 12 months. NTM earnings projections have steadily climbed throughout 2024, while FY1 and FY2 projections have been tapered. Investors are projecting earnings to grow roughly 10% a year over the next 3 years. This could set the table for some disappointment if rates move higher and eat up discretionary spending capabilities and raise financing costs. The level of interest rates is our primary concern entering 2025.

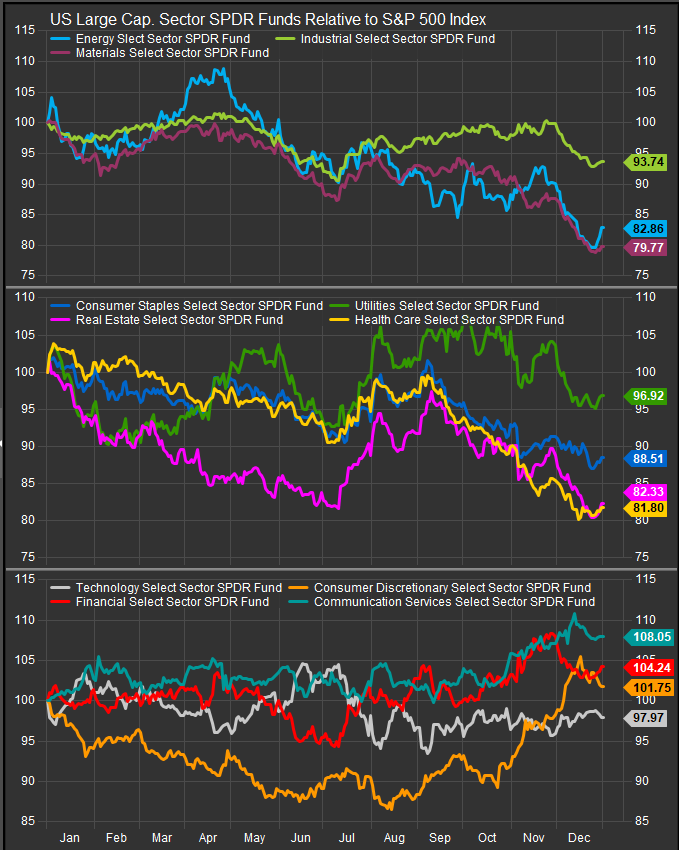

Sector Leadership

Despite December being a down month on the top line, sector leadership favored historically bullish, higher beta exposures. Discretionary was the top performing sector followed by Technology and Comm. Services. Low vol. sectors underperformed while facing a clear headwind from rising interest rates. Commodities linked sectors were the weakest performers with soft commodities prices indicating weak demand. This has combined with weak manufacturing PMI readings, expanding alternative energy capacity and structural headwinds like vehicle electrification to create a strong headwind to outperformance. That said, performance dispersion over 1, 3 and 6-month periods has widened out and there is elevated potential for mean-reversion entering 2025. The chart below shows sector relative performance over the past 6 months vs. the S&P 500.

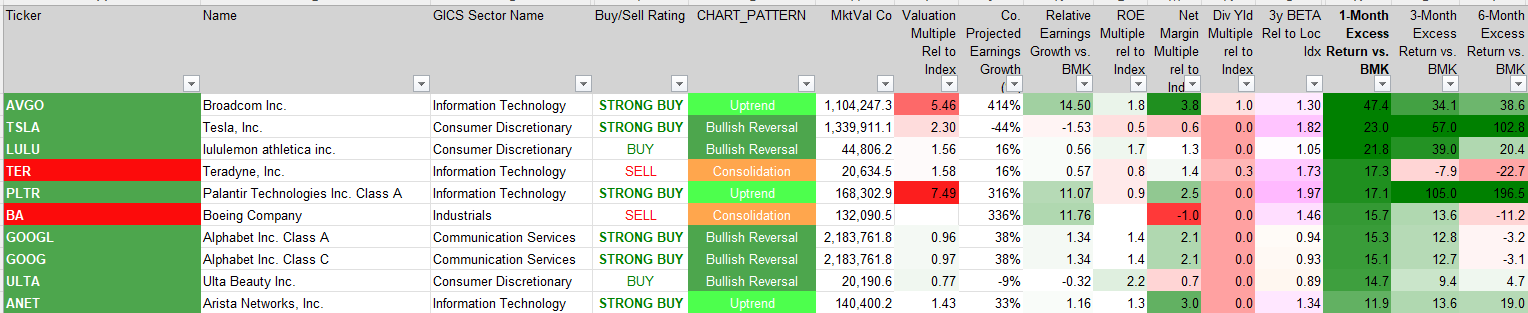

Top 10 Stock Performers

Mag7 and upside exposures in Discretionary and Tech dominated the outperformance list. Semiconductors in aggregate have consolidated, but AI winners like AVGO, ANET and PLTR are going strong. Looking at the profiles of the top performers, high relative earnings growth is still favored, and investors continue to be willing to pay up for it despite rich valuations.

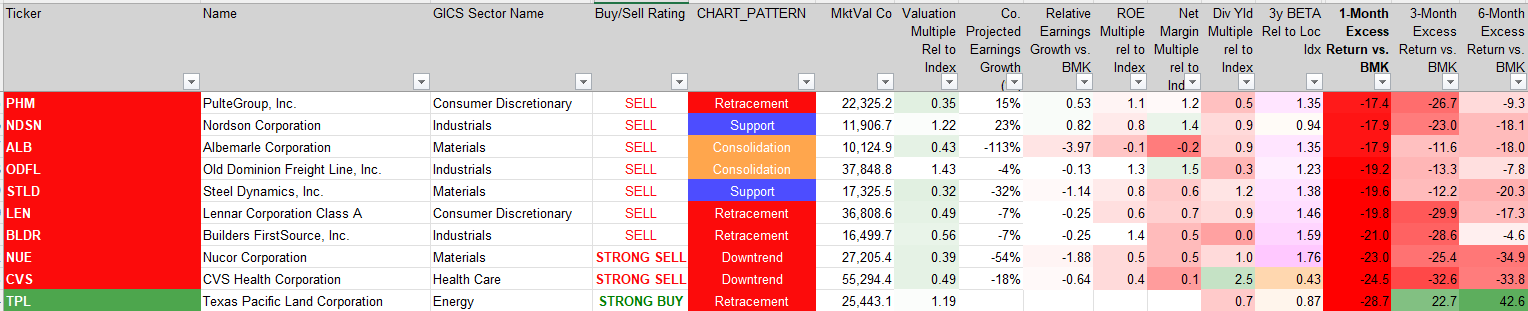

Top 10 Stock Performers

The bottom performers for December are industrials, materials and homebuilding stocks primarily. TPL is an interesting one as it has been a very strong long-term uptrend, and the near-term correction is a potential accumulation opportunity. Homebuilders have moved from buys to sells in our work generally. We would expect them to turn around if interest rates roll over.

Economic & Macro Developments

December economic data painted a mixed picture of the US economy. Inflation indicators suggested easing pressures, with core PCE rising only 0.1% month-over-month in November, below expectations of 0.2%, signaling progress in the Fed’s inflation fight. Consumer spending and income growth fell short of forecasts, coming in at +0.4% and +0.2%, respectively, reflecting cautious consumer behavior amidst high borrowing costs. Housing data was mixed: pending home sales rose 2.2% month-over-month, while housing starts and permits declined due to affordability issues driven by elevated mortgage rates. Manufacturing activity remained weak, with the Chicago PMI at 36.9, well below the 43.0 consensus. Labor market data remained robust, with weekly initial jobless claims consistently below expectations, maintaining the narrative of a tight labor market.

Macro factors influenced sentiment throughout December. The failure of the widely anticipated “Santa Claus rally” was partly due to year-end rebalancing pressures, with Goldman Sachs estimating $20B+ in US pension-fund equity selling. The Federal Reserve’s hawkish commentary dampened optimism, as the Fed flagged inflation, fiscal deficits, and a less aggressive easing cycle as ongoing concerns. Additionally, renewed tariff uncertainty under a potential Trump administration in 2025 contributed to unease. On the corporate front, Nvidia announced a focus on robotics as a new growth driver, while Tesla grappled with pricing pressures and delivery targets. Geopolitical risks were underscored by China’s 4.6% decline in industrial profits for November, adding to concerns about muted global growth prospects.

2025 Outlook

Looking ahead, US equities face a complex outlook for 2025. Although the S&P 500 is on track for back-to-back annual gains of more than 20%, risks include higher bond yields, sticky inflation, and fiscal headwinds. Investors are closely monitoring tariff policies, corporate earnings growth, and consumer spending trends. Legislative and fiscal dynamics, including deficit management and deregulation initiatives, could play a pivotal role in shaping market performance next year. Meanwhile, global factors such as China’s fiscal stimulus and geopolitical tensions remain critical for the broader economic and equity market narrative.

At the Sector level, Discretionary, Comm. Services and Technology Sectors outperformed in December, though positive returns have been trimmed heading into the new year. Commodities-linked exposures continued to be among the weakest sectors, while low vol. sectors also came under pressure as rates moved higher.

Using the US 10yr Yield as a proxy, rates are near-term overbought after moving above the 4.6% level recently. Rates are a key potential pivot entering 2025. If Yields continue higher from here, it puts more pressure on the consumer and the housing market. We note that commodities prices have remained near lowest levels for the year which leaves us skeptical of continued upside for rates.

In Conclusion

Equities have sold off in the last days of December and market internals are showing near-term breadth at wash out levels. Typically this has been a good setup for accumulation in the context of the longer-term bull trend for equities. We are siding with the bull at present, but we view rising interest rates with concern. Our Elev8 Sector rotation model rings in 2025 with overweight positions in Financials, Comm. Services, Technology, Discretionary, Energy, Staples and Industrials sectors. We are short, Materials, Healthcare, Utilities and Real Estate Sectors.

Data sourced from Factset Research Systems Inc.