January 13, 2026

The U.S. equity market is entering 2026 in a familiar but challenging position: growth remains intact, inflation pressures have eased, and recession fears have receded, yet leadership has become less forgiving and more rotational. The macro environment now looks best described as a late-cycle expansion with rising dispersion, where interest-rate uncertainty, earnings breadth, and fiscal expectations are shaping sector outcomes more than headline economic growth.

In this phase of the cycle, sector selection tends to matter far more than market direction. Broad beta still works, but incremental returns are increasingly earned by owning the right parts of the market at the right time, rather than by chasing what worked last year.

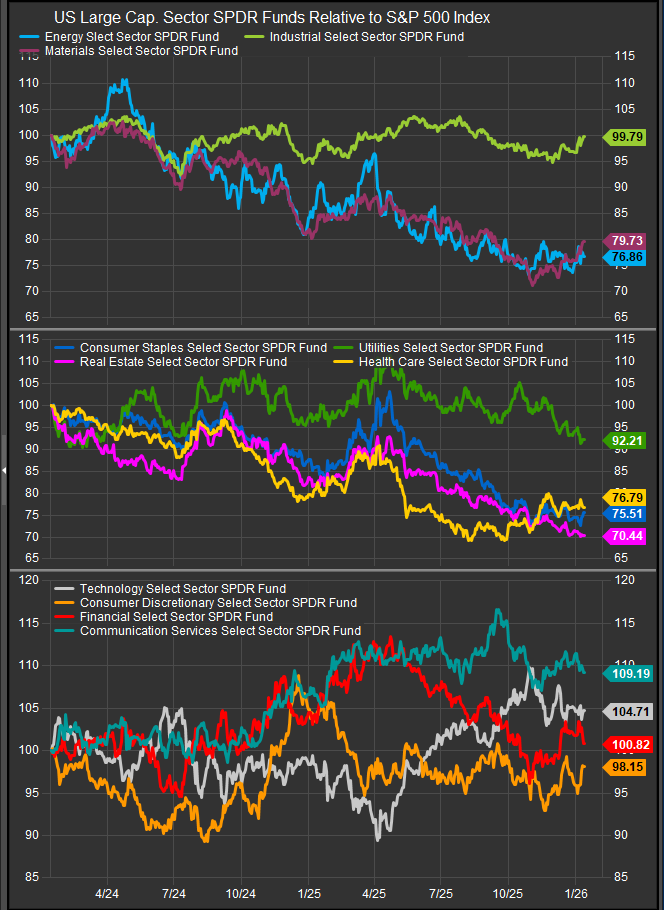

When considering the past 2 years of large cap. sector performance vs. the S&P 500 (chart below) and the current macro backdrop, we take stock of tactical considerations to give a view on where opportunities lie in the first half of 2026.

Sectors with the Best Forward Prospects

Industrials stand out as one of the clearest tactical beneficiaries of the current macro setup. The combination of improving productivity, easing unit labor costs, and rising expectations for fiscal and infrastructure-related spending creates a favorable backdrop for operating leverage. Importantly, Industrials are no longer just a “cyclical growth” trade—they are increasingly tied to secular themes such as automation, electrification, reshoring, and AI-related infrastructure. As earnings growth broadens beyond a narrow mega-cap cohort, Industrials offer exposure to expansion without the valuation sensitivity embedded in long-duration Growth sectors.

Financials, particularly large U.S. banks, also screen well tactically. Credit conditions remain stable, loan losses have stayed contained, and capital markets activity is showing signs of normalization. While rate cuts may eventually pressure net interest margins, the current environment of range-bound but elevated yields supports profitability, buybacks, and dividends. Financials also benefit from late-cycle dynamics, where investors favor near-term earnings visibility and balance-sheet strength over distant growth. As long as the economy avoids a sharp downturn, Financials remain well positioned.

Communication Services occupies a middle ground between cyclical and secular leadership. Unlike pure Technology, this sector offers exposure to AI-driven monetization, digital advertising, and platform scale, while maintaining stronger free-cash-flow profiles. As investors grow more selective around valuation, Communication Services can continue to attract capital as a “quality Growth” allocation—particularly if earnings momentum remains intact and ad demand stabilizes.

Health Care also deserves attention from a tactical perspective. While not a high-beta play on economic acceleration, it offers defensive growth characteristics that become increasingly valuable in a late-cycle environment. Earnings visibility, innovation pipelines, and lower macro sensitivity position Health Care as a stabilizer if volatility rises, while still allowing for upside through stock-specific catalysts. In an environment where investors are balancing pro-cyclical exposure with risk management, Health Care remains a natural portfolio anchor.

Sectors That Look Oversold or Mispriced

Some of the most interesting tactical opportunities lie not in leadership sectors, but in areas where sentiment and positioning have overshot fundamentals.

Energy is one such example. While longer-term revenue growth remains challenged, current equity pricing reflects a very pessimistic view of oil demand and pricing. Elevated global supply, geopolitical noise, and decarbonization narratives have kept investors sidelined. However, Energy equities remain highly sensitive to even modest improvements in pricing or capital discipline narratives. From a tactical standpoint, the sector is oversold relative to cash-flow generation and could rebound meaningfully if macro conditions remain supportive or geopolitical risks flare.

Materials also appear oversold relative to their historical sensitivity to global growth and fiscal spending. Concerns around China’s slowdown, currency strength, and uneven manufacturing data have weighed heavily on the group. Yet Materials tend to perform well when growth stabilizes and infrastructure and industrial activity pick up—conditions that are increasingly plausible given fiscal expectations and improving productivity trends. While volatile, the risk-reward has improved meaningfully at current levels.

Consumer Discretionary is more nuanced. The sector has lagged as investors grow cautious about household spending and income durability, particularly among lower- and middle-income consumers. That caution is not misplaced, but it has created selective opportunities. High-quality discretionary names with pricing power, strong balance sheets, and exposure to higher-income cohorts are increasingly mispriced alongside weaker peers. The sector may not lead broadly, but dispersion within it creates tactical entry points.

Sectors to Approach with Caution

Not all defensive or lagging sectors are attractive. Utilities and Consumer Staples, while traditionally viewed as safe havens, currently offer limited earnings growth and remain sensitive to rate volatility. In a scenario where rates remain elevated or volatile, these “bond proxy” sectors can underperform despite their defensive reputation. Without a clearer economic downturn signal, they appear better suited as hedges rather than sources of alpha.

Information Technology, despite its long-term strength, also warrants a more tactical lens. The sector continues to deliver superior earnings growth, particularly tied to AI infrastructure and software. However, valuation sensitivity remains high, and the bar for upside surprises has risen meaningfully. Technology is unlikely to collapse, but returns are likely to be more episodic and rotational, favoring selective exposure over blanket overweighting.

Putting It All Together

The defining feature of the current macro setup is not weakness, but selectivity. The economy appears to be expanding at a slower, more sustainable pace, with productivity gains offsetting labor-market cooling and fiscal expectations supporting demand. Interest rates are no longer a one-way tailwind, which raises the premium on earnings quality, cash-flow timing, and balance-sheet strength.

In this environment, Industrials and Financials offer the cleanest forward prospects, benefiting from broadening earnings growth and late-cycle dynamics. Communication Services and Health Care provide complementary exposure to secular growth and defensive stability. Meanwhile, oversold sectors such as Energy and Materials present tactical upside if macro fears fail to materialize.

For U.S. sector investors, the message is clear: this is not a market for passive sector bets or rigid style dogma. It is a market that rewards flexibility, valuation awareness, and an appreciation for where we sit in the cycle. As 2026 unfolds, the winners are likely to be those who lean into opportunity without losing sight of risk—embracing rotation rather than fighting it.