South Korea’s single-stock leveraged ETF experiment was meant to modernize the local ETF market. Within weeks of launch, it has become a test case for how quickly product innovation can collide with market concentration, retail leverage and regulatory risk.

The policy rationale was straightforward. Korean authorities wanted to close the gap between domestic ETF rules and overseas markets where Korean investors were already able to buy single-stock leveraged products through brokerage apps. Previous domestic rules effectively prevented single-stock ETFs by requiring diversified baskets and limiting exposure to any one holding. The new framework allowed ETFs and ETNs tied to blue-chip stocks, capped leverage at 2x, and added investor-protection rules around education, base deposits, risk labeling and securities-registration review.

Those safeguards looked meaningful on paper. Investors in the new products were required to complete additional training, receive warnings about negative compounding and premium/discount risk, and meet a 10 million won base deposit requirement. Product descriptions also had to highlight terms such as “single-stock,” “leverage” or “inverse” so investors would not mistake them for diversified equity ETFs. The issue is that disclosure-based safeguards are not always strong enough to cool a market already captivated by a narrow AI-driven rally.

Demand was immediate. The first leveraged ETFs tied to Samsung Electronics and SK hynix launched in late May, giving domestic investors a simple way to magnify exposure to the two companies most closely associated with Korea’s AI-memory boom. According to local reporting, retail investors bought nearly 2 trillion won of four Samsung- and SK hynix-linked leveraged ETFs on the first trading day. The attraction was obvious: these were not obscure speculative vehicles, but leveraged wrappers around Korea’s dominant companies and the country’s most powerful equity-market narrative.

The regulatory tone has since shifted sharply. Financial Supervisory Service Governor Lee Chan-jin acknowledged that approvals had been prepared too hastily and said the watchdog was reviewing possible stabilization measures. That is an unusually direct mea culpa. It reflects concern that the products are not merely giving investors another trading tool, but potentially amplifying the movement of the underlying stocks themselves.

The concern is credible because the market has become extremely concentrated. Samsung Electronics and SK hynix together now represent more than half of KOSPI market value, meaning their swings have index-level consequences. When the stocks fell more than 12% each on June 23, the KOSPI dropped nearly 10% and triggered a 20-minute market-wide trading halt.

SK Hynix

Chart: SK Hynix remains in a strong bull trend despite the recent pullback.

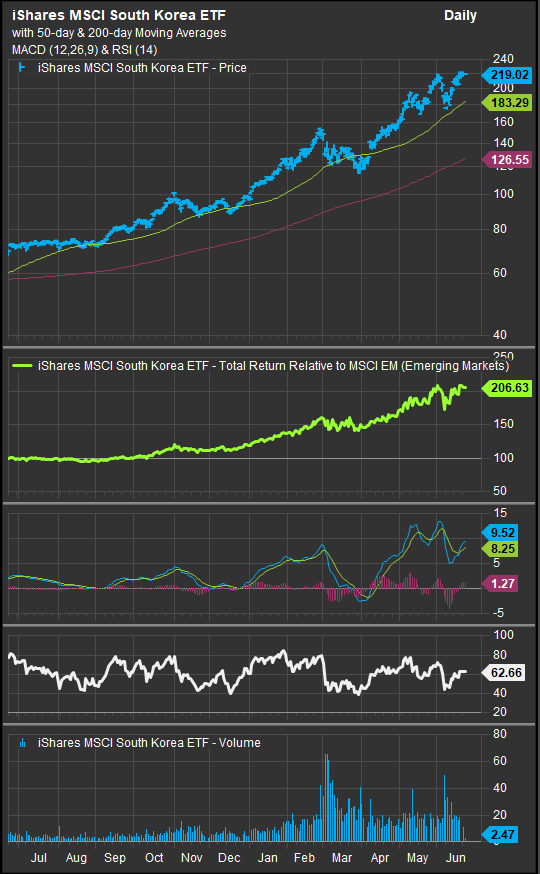

The same concentration has spilled into U.S.-listed Korea ETFs. The iShares MSCI South Korea ETF (EWY), the dominant Korea country ETF, had more than $26 billion in assets as of June 22 and was up roughly 122% year-to-date on a NAV total-return basis as of June 18. Franklin FTSE South Korea ETF (FLKR), a lower-cost broad-market alternative, reported a 91.6% YTD NAV return as of June 5, while Matthews Korea Active ETF (MKOR) was up 99.0% YTD as of June 18. The leveraged Direxion Daily MSCI South Korea Bull 3X ETF (KORU) had gained about 502% YTD on a NAV basis as of June 22. These returns underscore the strength of the Korea trade, but they also show how quickly broad Korea exposure has become a highly concentrated expression of the AI-memory cycle.

EWY

Chart: Volume into Korean equities has surged in the past 6-months.

KORU

Chart: KORU has delivered superior returns coincident with the bull trend.

That is the core tension for regulators. Korea wanted to keep domestic capital at home, deepen the local ETF market and give investors access to products they were already using overseas. Those are legitimate policy objectives. But importing single-stock leverage into a market dominated by a small number of chip leaders creates a different risk profile than launching the same structure on a broader, deeper U.S. equity market. The product may be capped at 2x, but the underlying exposure is attached to the most crowded trade in the country.

For investors, the lesson is not that Korea’s equity story is broken. The long-term case for Korean semiconductors, high-bandwidth memory, AI infrastructure and corporate-governance reform remains important. The lesson is that the vehicle matters. A diversified Korea ETF, an active Korea ETF, a 3x country ETF and a domestic 2x single-stock ETF may all appear to express the same macro view, but they carry very different compounding, liquidity, concentration and behavioral risks. Investors need to keep these fund specific risks in mind and manage them at the portfolio level.

The likely regulatory response will not necessarily be a full retreat. More likely, authorities will tighten product review, investor eligibility, app-based risk disclosures, marketing rules and market-stability mechanisms. Regulators may also revisit whether single-stock leveraged ETFs should be allowed on companies that already dominate index performance and retail trading behavior.

Recent selling related to Korean leveraged ETF regulation will be a test for the AI trade as well. Korea has been a central node in the global AI infrastructure trade. Product and regulatory risk is a consistent factor over time when innovation cycles become popular retail and mainstream investments. This market structure challenge for Korean equities is a likely bellwether for AI demand in the near-term. Anyone with significant assets devoted to AI exposure should be watching the Korean market closely in the near-term. The near-term reaction to overnight selling will be important from a crowd sentiment perspective.

Sources

- Financial Services Commission — January proposal on allowing single-stock ETFs/ETNs and limiting leveraged exposure to 200%.

- Financial Services Commission — April framework approving single-stock leveraged, inverse and covered-call products, with investor-protection requirements.

- Reuters — FSS Governor Lee Chan-jin’s comments that approvals were prepared hastily and stabilizing measures are under review.

- Reuters — June 23 KOSPI selloff, Samsung Electronics and SK hynix declines, and market-wide trading halt.

- BlackRock/iShares — EWY assets and YTD NAV total return data.

- Franklin Templeton — FLKR assets and YTD NAV return data.

- Matthews Asia — MKOR assets and YTD NAV return data.

- Direxion — KORU YTD NAV return data and fund objective.

Disclaimer: This material is for informational and research purposes only and does not constitute investment advice or a recommendation to buy or sell any security, ETF, ETN or derivative product. Past performance does not guarantee future results