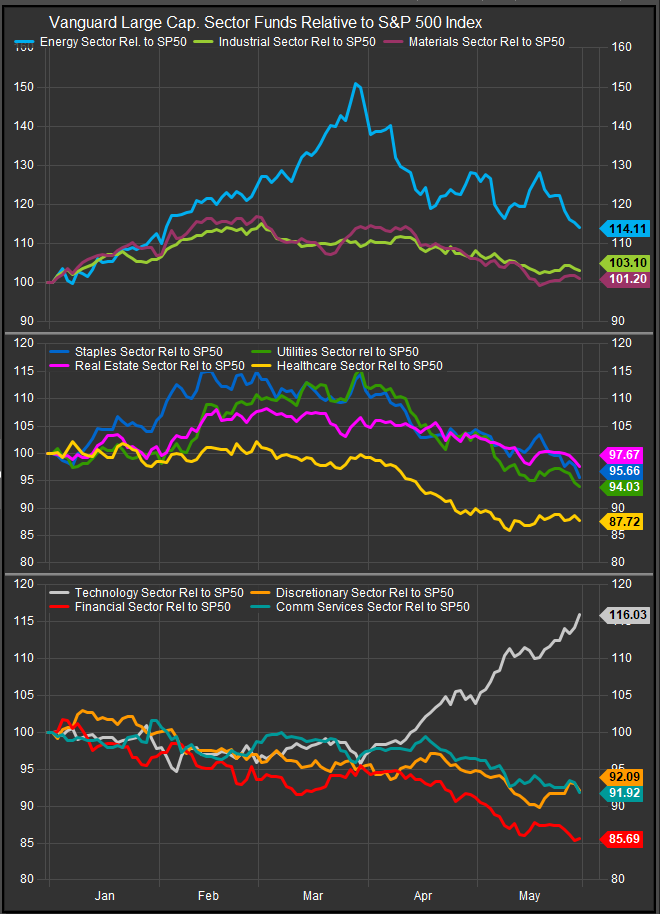

The sector story in 2026 has become increasingly simple: Information Technology is producing most of the excess return, while the rest of the market is being asked to prove that AI is an earnings opportunity rather than a disruption risk. May made that point unmistakably. StreetAccount’s May recap showed the S&P 500 up 5.15% and Nasdaq up 8.36%, but Technology was the only true sector outlier, rising 15.91% for the month, while Energy, Utilities, Staples, Financials, Real Estate, Industrials, Communication Services and Materials all lagged or declined.

This is not just a momentum tape. It is the market’s recognition phase for the AI paradigm. Investors have largely accepted that AI capability will be built out over a long horizon across semiconductors, memory, networking, servers, data centers, cloud infrastructure, power and cooling. The latest sector data reflected that conviction: AI-linked technology exposures dominated monthly returns, led by semiconductors, software, cloud, quantum and broader AI ETFs. StreetAccount also noted that AI tailwinds remained strong because of intense compute demand and expansive capex plans, even as investors continued to debate monetization, ROI and the timeline for productivity benefits.

The narrowness of leadership is therefore telling. The market is confident that the tools of AI must be built. It is much less confident about who will successfully use those tools. Goldman Sachs Research made a similar point in its recent work on enterprise AI: for returns to broaden beyond the semiconductor companies that have captured most of the benefit so far, enterprises need to unlock greater value from the technology. That is the key unresolved question for sector investors. AI adoption may improve margins for some incumbents, but it may also erode distribution advantages, commoditize software workflows, pressure labor-heavy service models and expose legacy operating systems that were never designed for real-time automation.

That is why the largest public companies outside the AI ecosystem should not automatically be viewed as safe adopters. Many have scale, data and customer relationships, but they also have the most profit pools at risk. In a paradigm shift, incumbency can be an asset — or a liability. Investors are paying a premium for companies closest to the build-out because the revenue path is visible. They are assigning lower conviction to downstream sectors because the winners are harder to identify.

The problem is that this setup also creates fragility. StreetAccount flagged that Information Technology exposures had reached the top percentile of their five-year range, that just ten stocks had accounted for 69% of the S&P 500 rally since late March, and that an estimated 87% of leveraged ETF assets were tied to “AI Tech Leadership.” Goldman Sachs has also reported that hedge fund clients have been taking profits in semiconductor and equipment makers after the rally, while also increasing short exposure to index and ETF macro products as a hedge. That is the right tell: sophisticated investors are not necessarily abandoning AI, but they are recognizing that the exit door can get crowded quickly when everyone owns the same expression of the same theme.

The answer is not to avoid the rally. The AI build-out remains the dominant earnings story. Goldman Sachs recently said AI-infrastructure beneficiaries are expected to account for roughly half of S&P 500 earnings growth this year, and BlackRock’s latest outlook continues to favor infrastructure and equipment tied to the AI build-out, including semiconductors, power and data centers. The answer is to own the rally with a risk budget rather than treating AI beta as a one-way trade.

A practical playbook starts with separating capex takers from capex spenders. The clearest beneficiaries remain the companies selling scarce inputs into the AI build-out: chips, memory, networking, optical components, server architecture, cooling systems, grid equipment and data-center infrastructure. This is where the market has the most visibility. But investors should avoid expressing the entire theme through the most crowded semiconductor basket alone. A more durable AI sleeve can include semiconductors, software infrastructure, power equipment, data-center suppliers and select industrial enablers.

Second, investors can broaden the AI trade without diluting it. Reuters recently highlighted growing interest in small-cap technology names tied to AI infrastructure, including data-center suppliers, networking companies and smaller chip-related businesses, while also warning that parts of the rally may be more speculative than fundamental. That is a useful distinction. Smaller AI beneficiaries may offer better upside than mega-cap leaders, but they require stricter balance-sheet and earnings discipline. In this phase, “AI exposure” is not enough; investors should ask whether the company has pricing power, backlog visibility, margin leverage and a credible path to profitability.

Third, investors should use sector offsets that are hard for AI to disrupt. Infrastructure equities are one example. BlackRock has argued that infrastructure can both benefit from AI adoption and be more difficult for AI to disrupt, especially as data-center growth drives demand for energy and physical assets. This does not mean buying every utility or energy stock indiscriminately. Regulated utilities can be rate-sensitive and politically constrained, while Energy remains hostage to oil prices. But power equipment, cooling, grid modernization, select infrastructure and data-center-adjacent real assets can provide a second layer of AI exposure with a different risk profile.

Fourth, investors should be willing to rebalance mechanically. The AI trade has become large enough that winners can quickly become unintended portfolio concentrations. Goldman’s observation that hedge funds were trimming semiconductor exposure appears less like a bearish call and more like disciplined risk control. Investors can apply the same logic by setting maximum weights for AI infrastructure, trimming after sharp relative moves, and rotating some gains into equal-weight technology, quality growth, infrastructure or cash-like reserves. The objective is to remain exposed while reducing the odds that a one-week reversal drives the entire portfolio.

Fifth, hedging should be considered before volatility returns. Protective puts provide direct downside insurance, but they can be expensive and need to be maintained over time. Collars can be more cost-efficient: they involve buying a put and selling a call against a long stock or ETF position, creating a downside floor while capping upside. Cboe notes that collars can sometimes be structured with minimal or no initial cost, though the tradeoff is limited upside participation. For investors with large gains in AI-heavy ETFs or single names, collars, put spreads, or partial index hedges may be more rational than trying to time the top.

The most important strategic point is that the AI rally should be played as a barbell, not as an all-in sector bet. One side of the barbell owns the build-out: semiconductors, memory, networking, cloud infrastructure, data-center equipment, power and cooling. The other side protects the portfolio from the possibility that the market suddenly questions AI ROI, capex discipline or valuation. That protection can come from cash, option collars, put spreads, equal-weight exposure, infrastructure, quality defensives, or simply lower position sizes in the most crowded winners.

The risk is not that AI stops mattering. The risk is that the market has already moved from disbelief to full recognition, and in recognition phases investors often discount the long-term destination before the earnings bridge is fully visible. Sector leadership is narrow because the infrastructure winners are obvious. It will broaden only when the market can identify the downstream adopters that turn AI into durable revenue growth, margin expansion and competitive advantage.

Until then, the playbook is clear: stay invested in the AI build-out, but do not confuse thematic conviction with portfolio resilience. The rally can continue, but the rush to the exit will be fastest in the expressions that have become easiest to own.

Sources

- StreetAccount Summary — US Monthly Recap, May 2026.

- StreetAccount Summary — US Weekly Recap / Weekend Headlines, week ended May 29, 2026.

- Latest FactSet sector return and flow data supplied for the editorial.

- Goldman Sachs Research — “Will the Corporate Investment in AI Pay Off?”

- Goldman Sachs — “How Hedge Funds Are Trading Semiconductor Stocks.”

- BlackRock — “Adding AI resilience to equity portfolios.”

- Reuters — “Investors hunt for AI winners in small-cap US tech stocks.”

- Options Industry Council — “Collar / Protective Collar.”

- Financial Planning Association — “Hedging with Options.”