The macro picture changed last week as persistently strong economic data has driven interest rates above 2024 highs to start the new year. Crude and Commodities prices have firmed in the near-term as investors position for a more inflationary environment and Growth areas of the equity market come under renewed pressure.

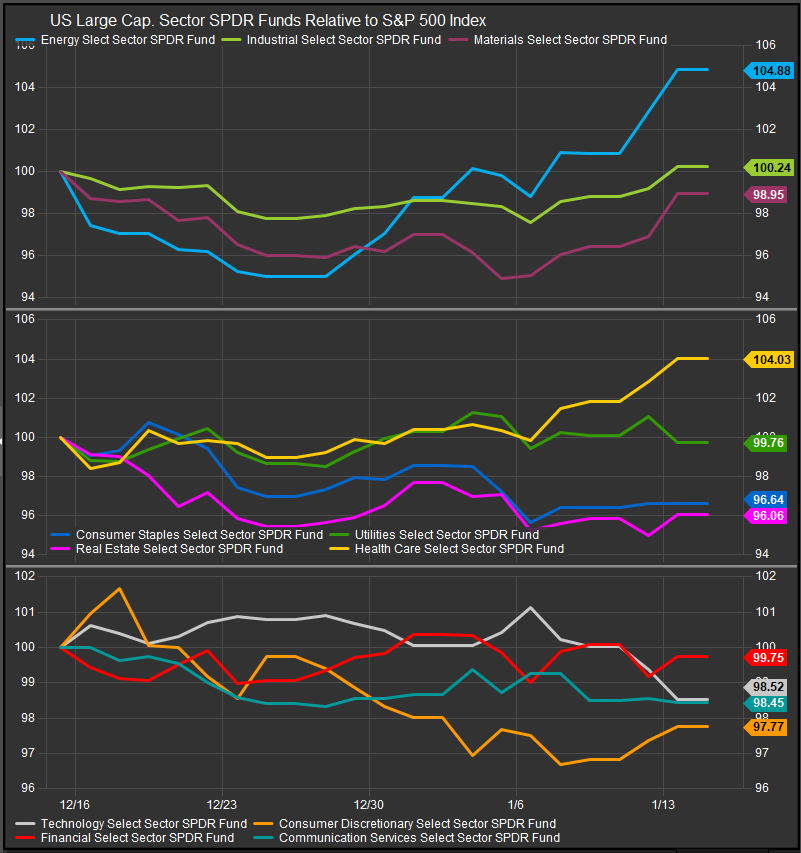

At the sector level, rotation into Energy and Healthcare sectors has been most pronounced near-term, though commodity-linked sectors have seen the broadest buying over the very short-term (chart below). Selling has hit the Real Estate, Technology and Consumer Sectors hardest. We think a mixture of commodity-linked and defensive sectors are likely to be leadership while market level turbulence persists.

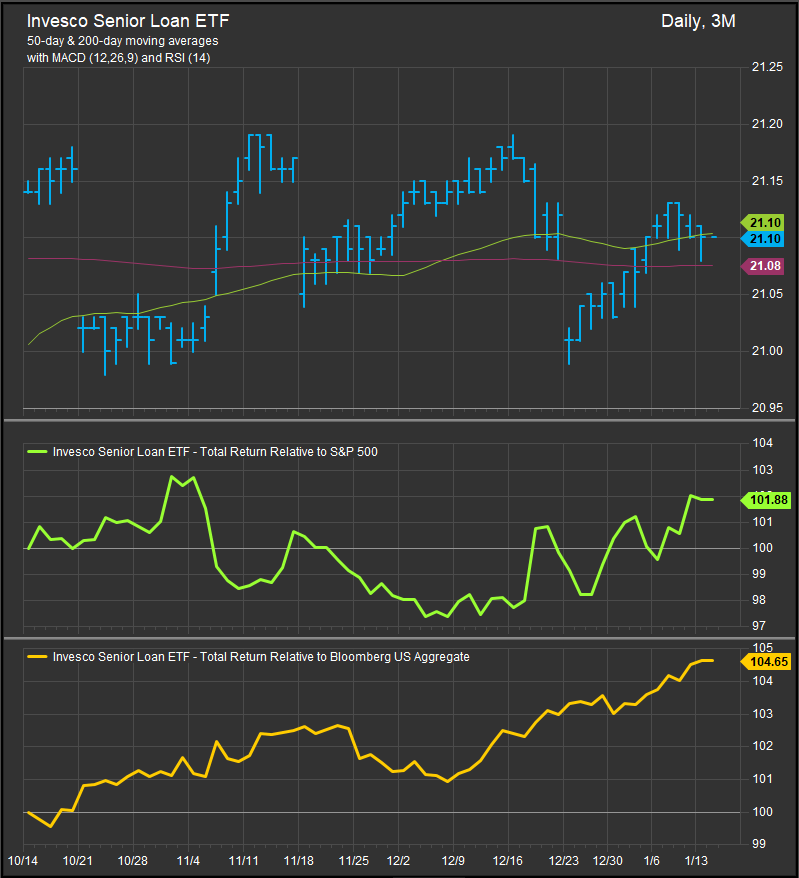

Within the fixed income markets, short duration bonds and floating rate securities like corporate bank loans have outperformed in the near-term as the long end of the curve backs up. A good example of the latter is the Invesco Senior Loan ETF (chart below). Bank loans have outperformed the S&P 500 and the Bloomberg Agg Bond Index over the past 3-months, and uncertainty about the direction of rates at the long-end of the curve is likely to persist, making the floating rate feature attractive.

With the US 10yr yield projecting more long-term upside to near the 5.8%-5.9% level (chart below), we expect the short end of the curve to be seen as safety while market turbulence persists. We also think defensive sectors of the equity market like Healthcare will continue to outperform in the near-term. The yield curve continues to steepen at the long end (chart below) which supports these trades.

Conclusion

Economic strength has triggered the re-emergence of inflationary pressures. Investors are starting to position for more inflationary outcomes, and we expect the Energy and Healthcare sectors to continue outperforming in the near-term. The macro dynamics are a tailwind to the performance of short duration and floating rate fixed income as well and we expect bank loan funds to continue outperforming while equities correct.

Data sourced from FactSet Research Systems Inc.