ETF Insights | January 1, 2025 | Information Technology Sector

Large Cap. Technology Sector Price Action & Performance

The Technology Sector enters 2025 consolidating gains above its July 2024 price high. Oscillator studies (chart below, panels 3 & 4) are at levels associated with uptrend oversold conditions, though a negative divergence on the RSI study in December is a negative development. Overall, the technical picture remains constructive.

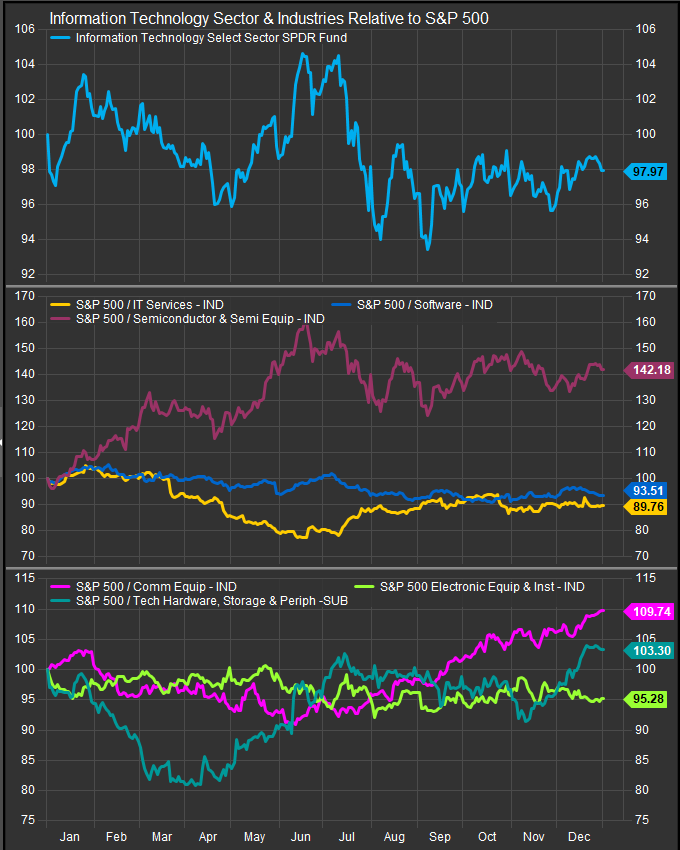

S&P 500 Technology Sector: Industry Performance Trends

Semiconductors spent the last 6 months of 2024 in consolidation though there remain some bullish standouts at the stock level. Comm. Services and Hardware delivered 2nd half outperformance on the backs of AAPL and ANET. Software and IT Services stocks continued in long-term corrections at the industry level.

S&P 500 Technology Sector Breadth

The Technology Sector breadth has shown some negative divergence, but the price structure at the top level has been resilient as different mega cap. stocks have picked up the sector. Capitulation level selling that doesn’t break a bullish price structure is a strong potential accumulation opportunity.

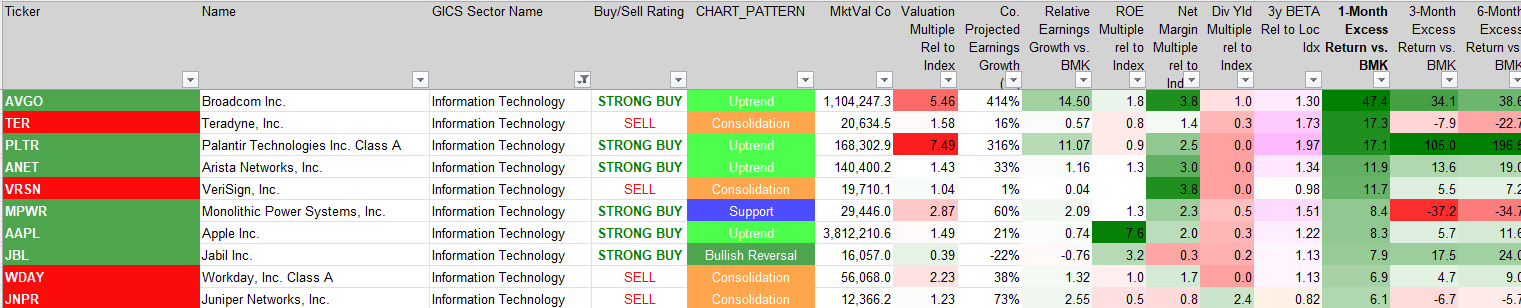

S&P 500 Technology Sector Top 10 Stock Performers

Despite a month of consolidating price action, there were some significant standouts led by AVGO, ANET and PLTR which had been among the strongest stocks heading into the month. Some previously down and out stocks bounced too, notably MPWR, TER, WDAY and JNPR.

S&P 500 Technology Sector Bottom 10 Stock Performers

The bottom 10 list generally features weak stocks getting weaker. However, FICO saw some significant profit-taking in the context of a strong long-term uptrend and scans as a potential opportunity in our work.

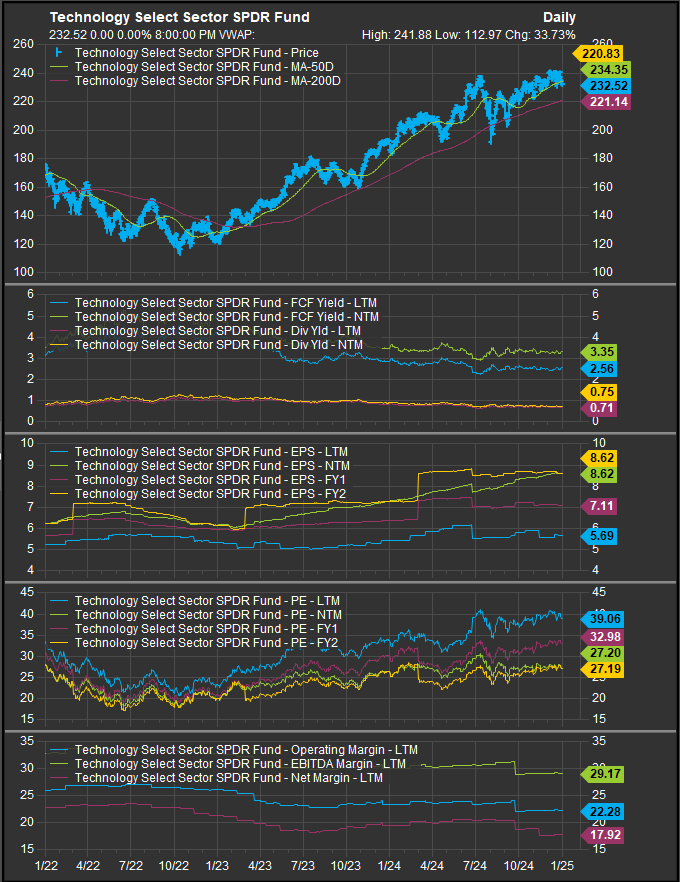

S&P 500 Technology Sector Fundamentals

The chart below shows S&P 500 Technology Sector FCF yield, and Dividend Yield as well as projected earnings over the next 3 years, valuation and trailing margins. Consensus earnings projections show robust continued EPS growth and a resulting downward move in the forward valuation multiple. Continued margin contraction (chart below, bottom panel) may become a concern.

Economic and Policy Developments

The global supply chain for software and semiconductors was shaped by several economic and policy developments during December 2024. Rising geopolitical tensions, particularly between the US and China, continued to impact semiconductor manufacturing and trade. Reports of potential new tariffs under a “Trump 2.0” administration created uncertainty for tech exporters and heightened risks of supply chain disruptions.

Domestically, elevated inflationary pressures and the Federal Reserve’s easing cycle influenced demand for capital-intensive projects in the tech industry. Persistently high interest rates, despite Fed cuts, increased borrowing costs for chipmakers and cloud providers, potentially delaying capacity expansions and R&D investments. Additionally, cybersecurity concerns came to the forefront after the US Treasury reported a major hack by Chinese actors. This underscored the vulnerabilities in global IT networks, which could drive increased spending on cybersecurity solutions in 2025.

On the demand side, reports indicated softening enterprise IT budgets amid tighter economic conditions. However, optimism about AI-related investments continued to provide a tailwind for semiconductor and cloud companies, particularly as businesses ramped up adoption of generative AI and edge computing technologies.

2025 Outlook

Analysts anticipate continued strength in AI-driven demand, particularly for GPUs and cloud services, with NVIDIA and AMD poised to benefit from increased enterprise and governmental AI adoption. The transition to robotics and automation highlighted by NVIDIA could also emerge as a significant growth area.

However, challenges persist. Semiconductor supply chains remain vulnerable to geopolitical risks and potential new tariffs, which could increase costs for manufacturers and delay the rollout of advanced chips. Additionally, enterprise IT spending could face further pressures if economic conditions tighten, affecting software, networking, and cloud providers.

On a positive note, government policies, such as the CHIPS Act, continue to support domestic semiconductor manufacturing, potentially reducing reliance on foreign supply chains over time. Increased cybersecurity spending, driven by recent incidents, may provide a growth catalyst for firms specializing in network security and data protection.

Overall, the US Information Technology sector is well-positioned to weather short-term challenges and capitalize on long-term opportunities, particularly in AI, automation, and cybersecurity. Investors should remain attentive to macroeconomic developments and policy shifts, which will likely play a significant role in shaping the sector’s trajectory.

In Conclusion

The Technology Sector presents to us as a bullish accumulation opportunity in 2025 provided interest rates stay contained. We start 2025 with the Technology Sector as an overweight position of +4.42% vs. the S&P 500 in our Elev8 Sector Rotation Model Portfolio.

Note: We have modified our sector fund selection criteria to use the largest US-based sector funds by AUM in our portfolio construction process. For Technology and Real Estate we use Vanguard Funds which include a slightly broader MSCI benchmark to replicate the sectors as compared to Sector SPDR funds which are bench marked to Standard & Poors Indices. However, our analytic process for the sector uses data from provided by S&P and we site the different headers as “S&P 500” and “Large Cap.” to reflect the difference.

Data sourced from Factset Research Systems Inc.