Readers of a certain age will remember SNL’s “Deep Thoughts.” A calming satirical interlude where we pause to reflect and think at a slightly different speed. There’s a satire angle here too as thinking deeply about long-term dynamics in the financial markets can be a fool’s errand when an economic print 0.1% above an expected threshold can send billions of dollars sloshing around between asset classes and sector exposures.

That said, we’ve been hitting you over the head on a weekly basis with factor analysis, equity and interest rate trends and sector trading dynamics. We are going to pause that frenetic game and lay out some of our high-level thoughts on what is motivating the bull market and what is problematic from our view. These are bigger ideas that frame how we interpret the day-to-day movements of the market.

Equities: Mega Cap. Growth vs. Everything Else

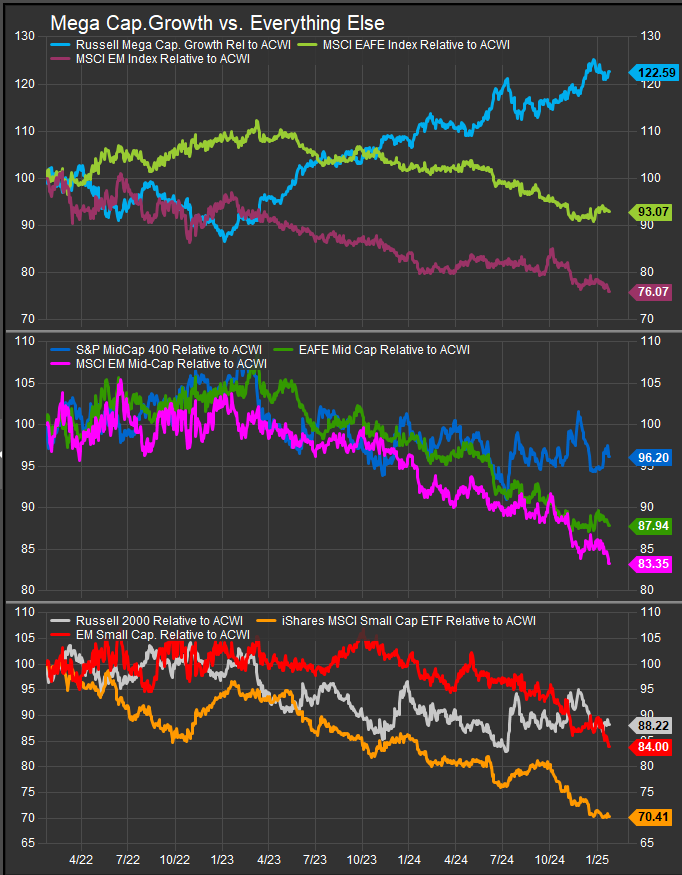

We start at the same place we usually start our regular Factor Friday column with. Russell 1K and Mega Cap. Growth vs. Value continues to have extremely high negative correlation (chart below).

But, let’s take Mega-Cap. Growth out of that chart and put it against US, EM and DM equity indices across small, mid and large cap. stocks over the past 3-years (chart below). Mega Cap. Growth has outperformed the MSCI All-Country World Index by >20% over the past 3-years even accounting for the bear market of 2022. For reference, the S&P 500 has outperformed by 7% over that time frame. Key takeaway is that the Mega Cap. Growth stocks accounted for all of the S&P 500’s excess returns during that time period. The S&P 500 ex-Mega Cap. Growth was just another laggard index in that period, and as the chart shows, so was everything else at the index level.

We think the takeaway here is to be respectful of the way equities will pivot knowing that perceived tailwinds or headwinds to Mega Cap. Growth are what will swing the market rather than some emerging new exuberance for Value stocks or Dividend stocks. Those will only be preferred once there are cracks in the Mega Cap. space. Mag7 is obviously at the core of this. The Roundhill Mag7 ETF (chart below) is a nice way to track the Mag7 performance. We can see by its relative curve vs. the S&P 500 that Mag7 softness since mid-December has corresponded with improving breadth and performance across a broad swath of sectors and stocks. If Mag 7 resumes its outperformance trend, it’s likely to continue sucking funds away from other exposures.

AI Needs to be a benefit to More than just AI Companies….

Dovetailing with Mega-Cap. Growth and Mag7 dominance is the AI theme. NVDA is obviously at the heart of the revolution, but every big Tech stack out there is a potential AI resource for collecting data and training a model. We are no experts on AI, but we flatter ourselves in thinking we have some common sense. The commonsense question that guides us more and more on AI is cui bono? Who benefits? Many are losing reasonably good jobs to the technology, but which companies not in the business of developing AI are actually outperforming because of AI. Given what we’ve shown with “Mega Cap. Growth vs. Everything Else” it’s fewer than we’d like to see given the panacea it’s believed to be.

In our informal accounting on the matter, we see COST and WMT in very strong sustained uptrends. WMT in particular has referenced AI as a driver of its efficiency. But otherwise, when we look across consumer and industrial business lines it’s unclear that there are big swaths of business that are becoming more attractive to invest in because they use AI to optimize their core business and investors perceive organic earnings growth resulting.

We need some optimism transference from AI makers to AI users to keep this bull market sustained. We need to start seeing it in the stocks!

Rising Rates: What if they Reflect Optimism?

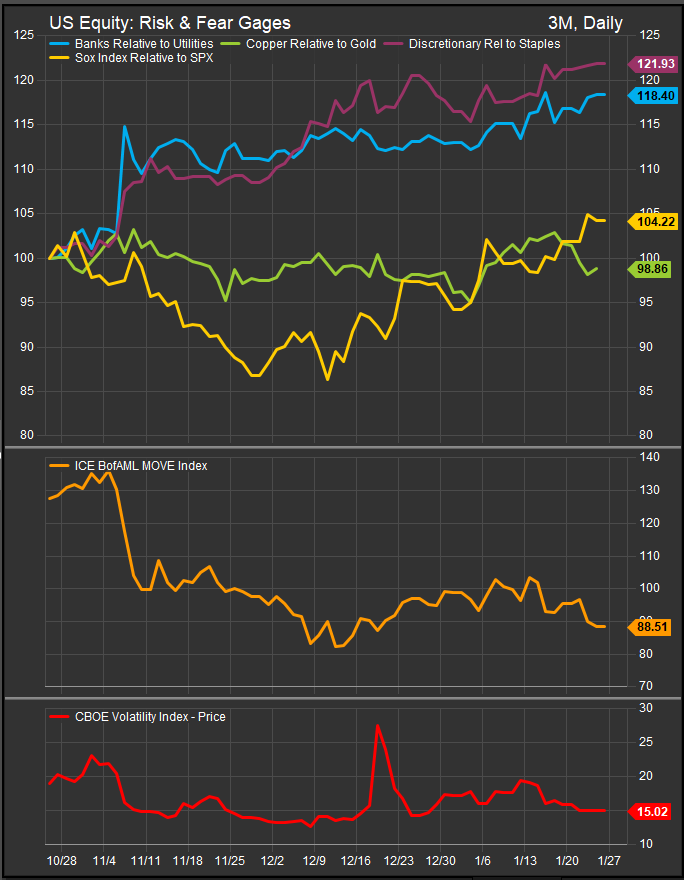

At the risk of sounding like we’re making excuses for ourselves, we recently got tactically cautious as rates moved above the 4.68% level 2 weeks ago. This was because our perception at the time was that rising rates are bad for equities and a threat to the bull market. We expected some sector rotation and, at the top line, some selling in aggregate. However, with Trump pulling a Grover Cleveland and getting back into the Whitehouse after a 4-year absence, there is an undeniable exuberance to some of the commentary around his deregulatory policies. Business and market types from CEO’s to Strategists are happy he’s back. They have a sense he will support their endeavors and ease regulatory burdens. These are more like “vibes” as younger generations than my Gen-X one are fond of referencing. There are good vibes in the US equity market. This sets the table for animal spirits. This also may explain why our risk appetite gages were firming when market internals were washing out at the end of the year. See the chart below.

Wealth > Wages

Moving to the micro from the macro. Anyone reading this letter feel like their salary is keeping up with their costs? If your salary is tied to asset values, it potentially has. If you’re a technologist in a “real job” not a “soft job”, it potentially has. If not, you’re likely with me saying “no”. However, prices still keep going up. The stock market is at all-time highs. Bitcoin is consolidating its latest moonshot and the bro who bought PLTR 12 months ago is bragging. More quietly, the Boomer generation has enjoyed most of two secular equity expansions in their lifetimes (1980-2000, 2013-present) and there are likely a bevy of very fat retirement accounts out there filling in for what adult children aren’t quite able to cover and funding home buying. The larger point being, there seems to be more money out there than what we can infer from payrolls, employment and the balance sheet of the average household. Wealth concentrates, and we see anecdotal signs of that everywhere now. From “Roaring Kitty” and “R/Stocktwits” pushing nothing-burger stocks exponentially higher for months to absurd salaries for the best athletes and celebrities, there seems to be a latent demand out there that doesn’t line up with mundainities lilke rising credit card defaults and too-high mortgage rates.

Interesting Things Happen in the Fixed Income Market When Long Rates Rise

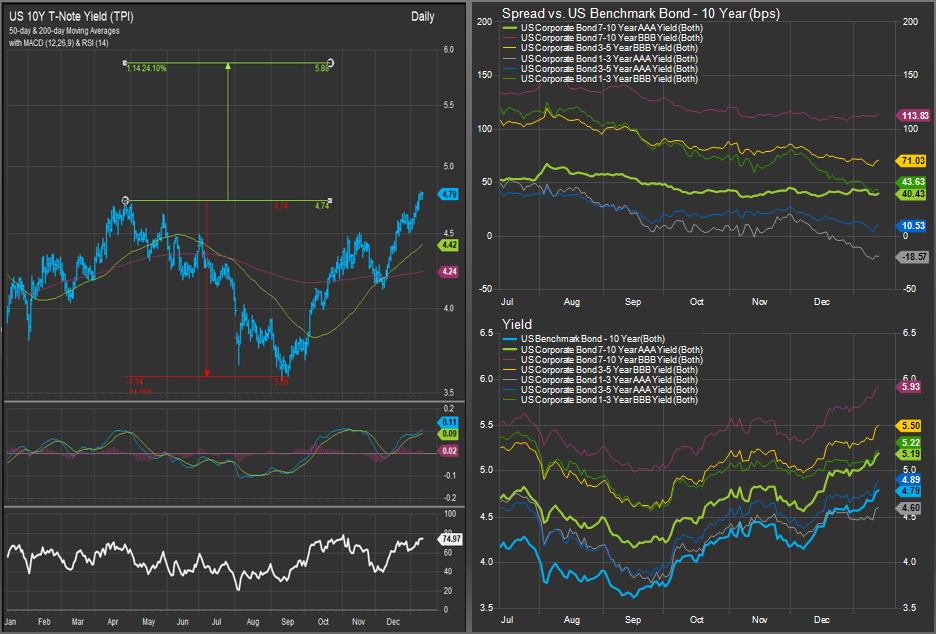

Our final though derives from contemplating why our indicator set is producing more “head-fakes” than we are accustomed to in the near-term. Interest rates are one of our indicators for sector positioning. The chart below shows corporate bond spreads vs. the Bloomberg AGG Bond Index next to a chart of the 10yr Yield. This chart is reprinted from January 15. The takeaway is rising yields pushed the 1-3 year BBB Yield spread into negative territory vs. AGG. This is a sign of herding.

There’s A LOT of money (scientific term!) typically budgeted for longer-duration fixed income exposure. When long yields move higher, that money is under-pressure to move. When a big repository for money starts getting redeemed the outflow of money can overwhelm smaller areas of the market and distort them. Bank Loans, BDC’s, equity derived fixed income and short duration fixed income generally are benefitting in the near-term. We think this is a crucial dynamic to monitor.

Data sourced from FactSet Research Systems Inc.