August 28, 2025

As investor continue to digest NVDA’s earnings report and position for the next leg of the AI trade, we wanted to call out some emerging near-term weakness in another key Technology theme in our column today. Cyber Security stocks and thematic funds have been retracing their YTD gains over the past 2-months, and we think there are signs of buyer exhaustion emerging in the stock charts.

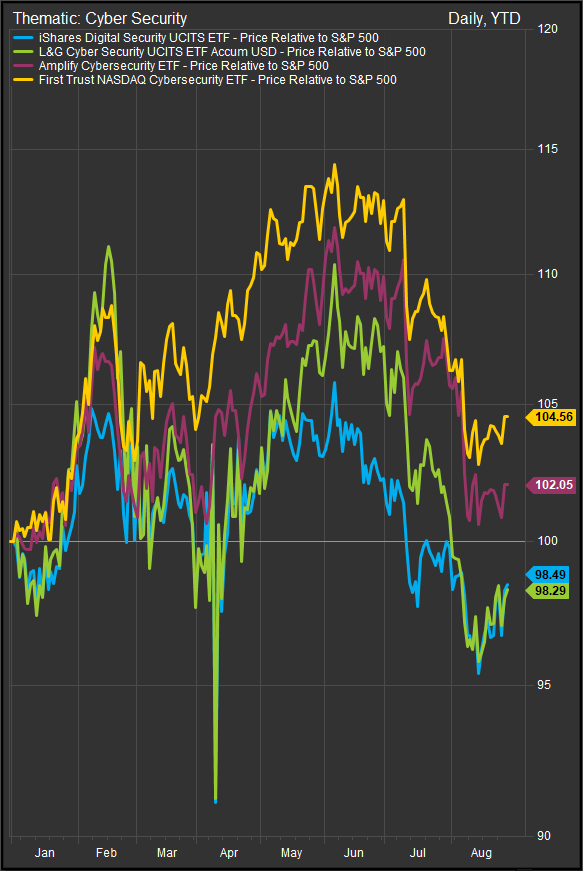

Looking at our basket of thematic cyber security ETFs (below), we can see the uniform retracement of YTD gains across our basket of liquid thematic ETFs in the space. We note the UCITS ETFs (LOCK and USPY) didn’t make convincing new highs after the April low for equities was put in and made new lows vs. the S&P 500 in August. US domiciled Cyber ETFs (we feature CIBR and HACK) have also given back YTD gains but have performed marginally better.

At the stock level some names have continued to show strength, but several key players in the space came through with disappointing earnings results in the most recent quarter. Over the last 2 months we’ve downgraded PANW, FTNT and OKTA and our aggregate fund score for CIBR has moved to a sell rating in the near-term as well.

FTNT

Recent bearish gap lower at the 200-day moving average is a bearish sign (chart below). Over the longer-term, the uptrend had weakened and the current selling triggers some longer-term trend change signals from our weekly momentum studies.

PANW

Price action is less extreme than with FTNT, but PANW also recently broke lower in the near-term after showing a loss of upside momentum in 2025 (chart below).

From a big picture perspective, it’s worth pointing out that bull markets driven by technological innovation typically go through internal transitions over the longer-term. Currently our fancy new technology is AI, but other tech themes like cyber-security, cloud computing and software as a service (SAAS) have been strong contributors to Tech sector outperformance in this cycle. We’ve already seen some big winner of the past roll over in this cycle (CRM, ADBE, WDAY, TEAM, ADSK, NOW) and we may be seeing another software-based theme peel off from the leadership bucket.

This change dynamic is intuitive considering the emergence of AI and how it is starting to take-over tasks that used to be the province of niche software applications. It also has precedent at a conceptual level. Since the 70’s we’ve seen the personal computer take over for the mainframe computer. We’ve seen Software take over as a dominant theme vs. Tech Hardware when PC makers became commodified in the late 90’s. The internet pushed out traditional PC based software after the “Tech Bubble” overhang dissipated in the 2010’s, while software as service put pressure on traditional IT services companies in that period as well.

We’ve argued that AI could and should be its own sector, but we’re also looking to identify AI companies in different sectors, not just because they contribute to a Tech based AI company, but because AI is ingrained their business line that it is adopted into new sectors. For example, companies like WMT and AMZN have huge potential benefit from AI as inventory management, pricing, sourcing and logistics coordination. That process is already starting, but the language with which the media describes those companies will be key going forward.

Conclusion

We think AI enthusiasm may have hit a near-term peak, but when we consider the longer-term nature of technology innovation, we would expect that AI is positioned to remain the most relevant concern within the Tech Sector. We think sector investors would benefit from tracking technology themes at a high level. We’re expecting AI integration to eventually move beyond the Tech Sector as its locus. We also think that if the AI trend can live up to the hype, we must eventually see results that promise material growth and efficiency to a broader array of businesses. That potential remains on the table, and we think that’s why the AI theme will persist despite the usual ebbs and flows of a long-term trend.