October 2, 2025

In 2025, commodity prices have remained subdued despite persistent inflation concerns (chart below), a divergence rooted in slowing global demand, resilient supply, and shifting inflation dynamics. The World Bank projects that aggregate commodity prices will decline by roughly 12% in 2025, followed by another 5% drop in 2026. This weakness is especially striking against a backdrop of stubborn U.S. consumer price inflation, which is services-led rather than commodities-driven.

BCOM

Global demand weakness is central to the story. The IMF downgraded China’s growth outlook to 4.0% for 2025, reflecting weak domestic consumption, modest fixed-asset investment (+2.8% YoY in H1), and falling producer prices (-2.8% in H1). Industrial production remained firmer at +6.4% YoY, but property sector weakness and sluggish internal demand limited metals and energy uptake. In Europe, growth is stuck at +0.5% annualized, with manufacturing PMIs consistently under 50, signaling contraction. Japan’s growth has plateaued as well. In the U.S., Industrial Production grew just 0.9% YoY in August, and the ISM Manufacturing PMI registered 49.1 in September, confirming contractionary trends. Global PMI aggregates likewise show factory activity subdued. These figures underscore that while inflation persists, it is not commodity-driven but instead rooted in wages, shelter, and services.

China

The supply backdrop has added to downward price pressure. U.S. shale output has been resilient, while OPEC+ discipline has weakened. The World Bank reported an energy price index decline of 3.9% in August, with U.S. natural gas down 8.8% and oil down 3.6%. Metals have also struggled, with the metals index off 0.3% in the same month. Agriculture has remained stable after strong harvests, and weather disruptions have been limited. Without acute supply shocks, commodities have lacked catalysts for sustained rallies.

Crude

Financial and currency markets have reinforced this picture. A strong U.S. dollar—underpinned by delayed Fed easing and safe-haven demand—has depressed commodities by making them more expensive for non-U.S. buyers. Investor flows into commodities have also been muted, with speculative funds favoring technology and growth equities over commodity exposures. The “inflation hedge” bid into raw materials, strong in 2021–2022, has not returned.

Commodity-linked equities have underperformed. Energy and materials have lagged the S&P 500 in 2025 as lower commodity realizations and weak global industrial activity eroded earnings leverage. The Russell 1000 Growth index has significantly outpaced Value in mid-2025, confirming that investor preference lies with technology and consumer growth stories rather than commodity-linked cyclicals. Agricultural equities have also normalized, as the input-price shock that drove extraordinary margins in 2022–2023 has faded.

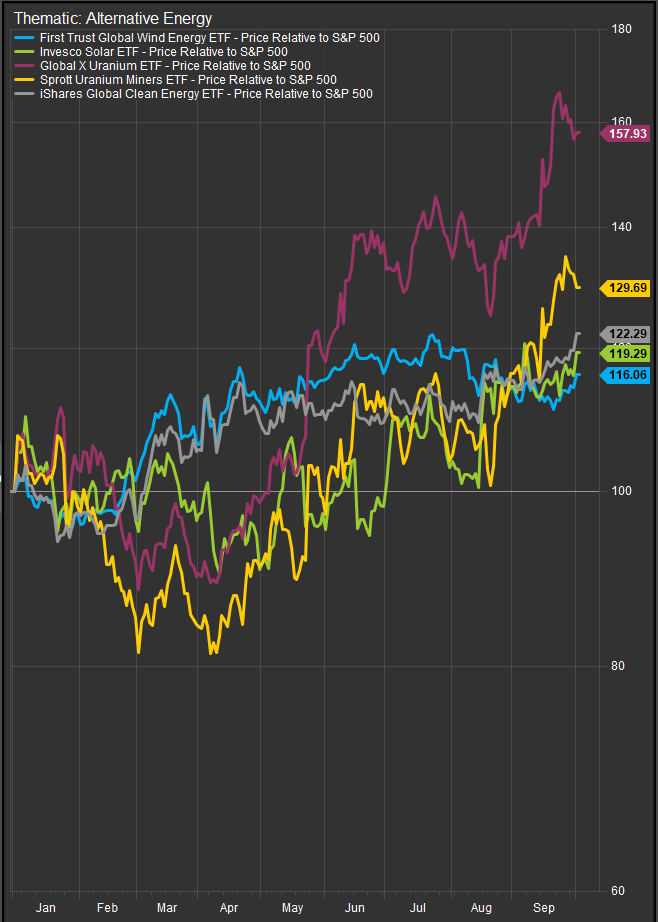

Opportunities remain for select investors. Precious metals such as gold (chart below) and silver are benefiting from safe-haven demand, expectations of Fed rate cuts, and geopolitical hedging. Energy majors with downstream refining and chemicals may defend margins more effectively than upstream-only peers. In materials, copper producers stand out given their link to electrification, grid upgrades (chart below), and clean energy infrastructure, even as cyclical demand softens. Agricultural firms with global diversification may provide relative protection if climate variability introduces episodic supply shocks.

Gold

Smart Grid

Alternative Energy ETFs

In order for commodity demand to rebound in a meaningful way, several shifts would need to occur across the global economy, policy environment, and financial markets. At the core is the need for stronger global growth. China, which remains the world’s largest marginal consumer of many raw materials, has been growing at just above 4% in 2025, far below levels that previously supported commodity super-cycles. A meaningful acceleration in property activity or large-scale fiscal stimulus focused on infrastructure could reignite demand for metals such as steel, copper, and aluminum, as well as for energy inputs. Similarly, a recovery in Europe and Japan—where GDP growth has been stuck near 0.5%—would lift industrial consumption. Emerging markets, particularly India, Southeast Asia, and parts of Africa, also hold the potential to provide incremental demand for food, energy, and construction-related metals if their domestic growth trajectories accelerate.

Overall, 2025 has demonstrated that headline inflation does not necessarily translate into commodity strength. With services driving price pressures, demand for raw materials soft, supply resilient, and financial flows disengaged, commodity prices have stayed low. Yet, investors attentive to structural trends—green transition demand, precious metals, and select integrated energy and agriculture plays—may find opportunities in a market where broad indexes remain under pressure.

Sources

- International Monetary Fund. World Economic Outlook April 2025: Chapter 1. IMF, 2025. imf.org

- World Bank. Commodity Markets Outlook April 2025. World Bank, 2025. thedocs.worldbank.org

- World Bank. Commodity Price Data (The Pink Sheet), August 2025. worldbank.org

- U.S. Federal Reserve / Trading Economics. United States Industrial Production, August 2025. tradingeconomics.com

- Institute for Supply Management. ISM Manufacturing PMI Report, September 2025. prnewswire.com

- S&P Global. Global Manufacturing PMI, September 2025. spglobal.com

- China Briefing. China’s Economy in H1 2025: GDP, Trade and FDI Highlights. china-briefing.com

- Behorizon. China’s Economy in H1 2025: Resilience Amidst Uncertainty. behorizon.org

- Mesirow. 2Q 2025 Market Summary. mesirow.com

- LPL Financial. Midyear Outlook 2025: Fixed Income and Commodities. lpl.com

- Morgan Stanley. Commodity Outlook 2025: Three Areas to Watch. morganstanley.com

Other Data sourced from Factset Research Systems Inc.