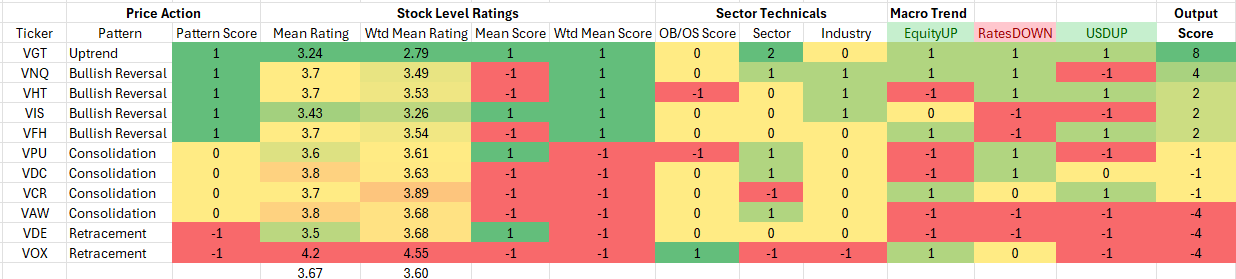

TOP3 Model Input Scores: July 2026

The table below shows the TOP3 model’s scores for July. Technology remains the top-rated sector idea. The model prefers near-term bullish reversal sectors Real Estate and Healthcare to compliment its Technology exposure in July. Financials had a similar score to Healthcare this month, but lost the tie-breaker. Communication Services was the lowest rated sector.

Key: Pattern = L/T (1yr+) Price Pattern of the Sector ETF, Mean Rating = simple average of 1-6 ratings (buyàsell) of all stocks within the sector, WTD Mean Rating = Cap Weighted Sector Constituent rating, OB = Overbought, OS = Oversold, N=Neutral

Model Input Commentary

The model inputs continue to favor Information Technology sector exposure. With interest rates remaining contained and commodities prices continuing to retrace gains despite the Fed’s emerging hawkish tone, investors are moving off their near-term defensive crouch and our models are supportive of pro-cyclical and Technology exposure. Healthcare and Real Estate sectors are favored among low vol. sectors. Energy and Materials sectors are near the bottom of our rankings as the market continues to discount geopolitical détente. The Communication Services sector ranked the weakest in our work as Alphabet corp. is showing signs of bearish transition. META and NFLX had already made a bearish transition and the sector is now without support from its 3 mega-cap. tentpoles.

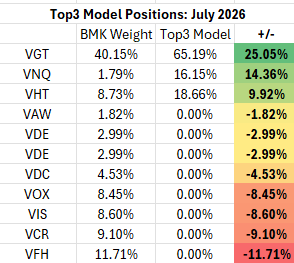

TOP3 Sector Rotation Model Portfolio: July Positioning vs. Benchmark Simulated S&P 500 (data as of 7/1/2026)

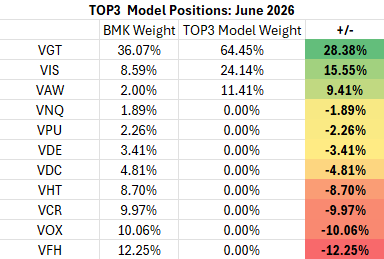

Previous Positioning as of last Rebalance: May 29, 2026

Conclusion

The AI trade remains central to the bull market and the current business cycle. After June’s consolidation, price action is firming in the near-term. Continuing downward pressure on commodities prices and a more hawkish Fed. have shaken out some speculative positions, but with interest rates moving lower and market breadth expanding, we think the bullish setup remains intact for July with firming employment figures in the near-term assuaging fears of a decelerating business cycle. Bullish re-rating for Healthcare and Real Estate is a good complimentary position for Technology exposure. We think a more hawkish Fed. is likely to cool inflationary dynamics as investors are likely to be more sober in their positioning with a potential rate hike or two added to the forward outlook. In the near-term we’ve seen interest rates move LOWER and that has typically been a tailwind for legacy defensive sectors like Healthcare and Real Estate.

About TOP3

We introduced the TOP3 Sector Rotation Model in July of 2024. Here’s a look under the hood at the inputs we use to score the 11 GICS Sectors and our resulting positions. The model includes up to 14 indicators that range from:

- Stock Level Technical Characteristics

- Macro-overlays:

- equity trend (S&P 500)

- interest rate trend (10yr US Treasury Yield)

- commodities trend (Bloomberg Commodities Index)

- USD trend (vs. EUR & Broad Currency Indices)

- Relative performance vs. the benchmark S&P 500

- Overbought/Oversold oscillator studies

We use the largest passive sector-based ETF by AUM ($) for each sector as our proxy for TOP3 sector positions. We select 3 out of 11 Sectors each month and have no exposure to the 8 sectors with the lowest scores in our model.

Data from Factset Research Systems Inc.