COMMENTARY:

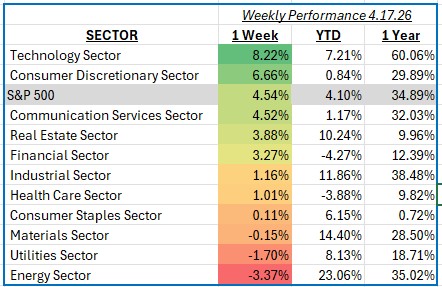

The S&P 500 advanced 4.54% for the week ending April 17, 2026, reflecting a strong rebound in equity markets driven by improving sentiment and supportive macro signals. Key highlights included moderating inflation data, which reinforced expectations for a more accommodative monetary policy path, and better-than-expected corporate earnings that helped stabilize growth concerns. Additionally, a decline in bond yields supported equity valuations, particularly in growth-oriented sectors.

Technology was the top-performing sector, gaining 8.2% for the week. The rally was fueled by renewed strength in mega-cap growth names, particularly Apple, Microsoft, and NVIDIA, as investors rotated back into high-quality secular growth leaders. Optimism around artificial intelligence spending and continued enterprise demand for cloud services were key drivers. Semiconductor companies also outperformed, supported by improving demand expectations and easing supply chain concerns, contributing meaningfully to the sector’s gains.

Consumer Discretionary also posted a strong return of 6.7%. Performance was led by dominant platform and retail names such as Amazon and Tesla, which benefited from resilient consumer spending trends and positive forward guidance. Strength in travel, leisure, and luxury goods further supported the sector, as demand remained robust despite prior concerns about economic slowing. E-commerce and digital services providers were particularly strong contributors as consumer activity continued to shift toward online channels.

Energy was the weakest-performing sector, declining 3.4% during the week. The pullback was driven primarily by lower crude oil prices, which weighed on large integrated producers such as ExxonMobil and Chevron. Softer commodity pricing, combined with concerns around global demand and rising inventories, pressured earnings expectations across the sector. Exploration and production companies also lagged, while oilfield services names saw more modest declines amid a slightly weaker activity outlook.

In summary, markets were led higher by growth-oriented sectors, particularly technology and consumer-driven industries, while energy lagged on commodity weakness. The week underscored a renewed preference for secular growth and earnings visibility, setting a constructive tone for equities in the near term.