COMMENTARY:

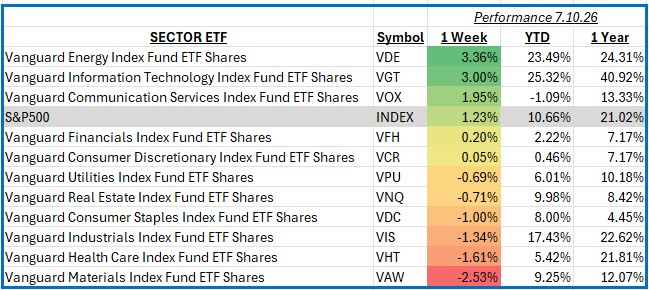

U.S. equities continued their upward momentum during the week ending July 10, with the S&P 500 advancing 1.23%. Investors were encouraged by another round of resilient economic data, including continued strength in the labor market and signs that inflation remains on a gradual path toward the Federal Reserve’s long-term target. Market sentiment also benefited from growing expectations that interest rates may remain stable in the coming months, while second-quarter earnings season approached with optimism that corporate profits will continue to demonstrate resilience despite a slower pace of economic growth.

Energy was the strongest-performing sector of the week, gaining 3.4% as crude oil prices moved higher on expectations for solid summer fuel demand and disciplined global production. Investors also responded favorably to improving global growth expectations, which supported the outlook for energy consumption. Integrated oil producers and exploration companies accounted for much of the sector’s advance, with Exxon Mobil and Chevron leading performance. Oilfield service companies also contributed positively as expectations for continued capital spending and drilling activity strengthened across the industry.

Information Technology was another standout performer, returning 3.0% as investors maintained their enthusiasm for artificial intelligence, cloud computing, and semiconductor-related businesses. Strong demand for high-performance computing and continued investment in AI infrastructure helped drive gains across the sector. Nvidia once again led performance, while Microsoft, Apple, and Broadcom also made significant positive contributions as investors continued to reward companies with durable earnings growth, strong balance sheets, and leadership positions in emerging technologies.

Materials was among the weakest sectors, declining 2.5% as lower industrial commodity prices and ongoing concerns about slowing manufacturing activity weighed on the group. Metals and mining companies, chemical manufacturers, and construction materials producers generally underperformed as investors questioned the pace of global industrial demand, particularly in China. Several diversified materials companies experienced broad-based selling pressure as investors favored sectors with stronger earnings momentum.

Health Care also lagged the broader market, falling 1.6%. Large pharmaceutical companies, health insurers, and medical device manufacturers contributed to the sector’s weakness as investors rotated toward more economically sensitive industries. Eli Lilly, UnitedHealth Group, and Abbott Laboratories were among the largest detractors during the week, although biotechnology stocks provided modest support in select areas of the sector.

Overall, the market demonstrated continued resilience as investors balanced encouraging economic data with anticipation for the upcoming earnings season. While leadership rotated among sectors, the broader backdrop remained constructive, reinforcing confidence in the long-term outlook for diversified investors.