COMMENTARY:

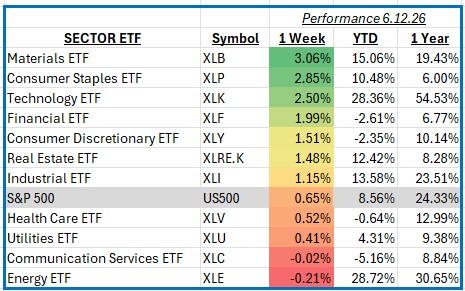

U.S. equities continued their advance during the week ending June 12, with the S&P 500 Index gaining 0.65%. Investor sentiment was supported by resilient economic data, easing concerns about a near-term slowdown, and continued optimism surrounding artificial intelligence and technology-related capital spending. Markets also focused on inflation trends that remained generally constructive, reinforcing expectations that monetary policy may become less restrictive later this year. Additionally, excitement surrounding the highly anticipated SpaceX initial public offering generated significant investor interest and contributed to broader enthusiasm for growth-oriented investments and capital markets activity.

The Materials sector was the strongest performer of the week, advancing 3.1%. Strength across industrial metals, construction materials, and specialty chemicals helped drive gains as investors responded positively to signs of improving global manufacturing activity and expectations for increased infrastructure spending. Several large constituents benefited from rising commodity prices and improving demand expectations. Leading contributors included Linde, Sherwin-Williams, and Freeport-McMoRan, with the latter receiving additional support from higher copper prices and growing optimism surrounding long-term electrification trends.

Consumer Staples also delivered a strong performance, rising 2.9% during the week. Investors rotated toward defensive sectors as geopolitical uncertainty and mixed economic signals encouraged a more balanced market posture. The sector benefited from stable earnings expectations, resilient consumer demand, and attractive dividend yields. Major contributors included Costco, Walmart, and Procter & Gamble, all of which outperformed as investors favored companies with strong pricing power, consistent cash flows, and dependable earnings growth.

Energy was among the weakest sectors, declining 0.2% for the week. Crude oil prices traded in a volatile range as investors weighed global demand concerns against ongoing geopolitical developments. While energy fundamentals remain relatively healthy, profit-taking following a strong prior run contributed to the sector’s underperformance. Larger integrated producers including Exxon Mobil and Chevron lagged, while weakness among certain exploration and production companies also weighed on overall returns.

Communication Services was another relative laggard, slipping 0.02%. The sector faced modest pressure as investors rotated toward cyclical and defensive areas of the market following several months of strong performance from large-cap growth companies. Some profit-taking in major holdings including Alphabet and Meta Platforms offset gains elsewhere within the sector. Despite the week’s underperformance, fundamentals remain supported by continued growth in digital advertising, cloud services, and artificial intelligence-related investments.

Overall, market performance remained constructive, with broad participation across sectors and continued support from economic resilience and corporate earnings expectations. While leadership rotated during the week, investor confidence remained intact as markets continued to balance growth opportunities with evolving economic and geopolitical developments.