COMMENTARY:

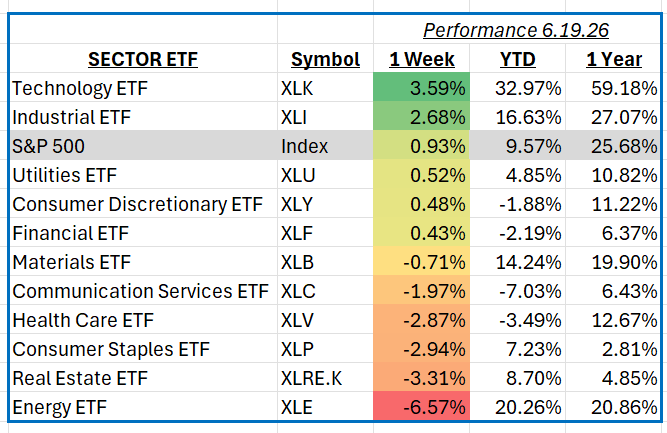

The S&P 500 advanced 0.93% for the week ending June 19, 2026, as investors navigated a mix of economic data, central bank commentary, and geopolitical developments. Market sentiment was supported by continued optimism surrounding artificial intelligence-related investment spending, resilient corporate earnings expectations, and signs that the U.S. economy remains on stable footing despite ongoing inflation concerns. Investors also closely monitored interest rate expectations and energy market volatility, which contributed to significant performance differences across sectors.

Technology was the strongest-performing sector during the week, gaining 3.6%. The sector benefited from continued enthusiasm surrounding artificial intelligence infrastructure spending, cloud computing demand, and semiconductor growth trends. Large-cap technology companies led the advance, with semiconductor and software names providing the largest contributions to returns. Strong performance from industry leaders such as NVIDIA, Microsoft, Broadcom, and Apple helped drive gains as investors continued to reward companies viewed as key beneficiaries of long-term AI adoption. Improved risk appetite and declining concerns about near-term economic weakness further supported the sector’s outperformance.

Industrials also delivered strong results, rising 2.7% for the week. Investor optimism was driven by expectations for continued infrastructure spending, manufacturing activity stabilization, and healthy demand for aerospace and defense products. Aerospace and industrial equipment companies were among the largest contributors, with companies such as GE Aerospace, Caterpillar, RTX, and Uber Technologies helping lift the sector. The group also benefited from expectations that capital expenditure trends remain constructive despite an uncertain global economic backdrop.

Energy was the weakest-performing sector, declining 6.6%. The sector came under pressure as crude oil prices retreated amid concerns about global demand growth and increased market volatility surrounding geopolitical developments. Integrated oil producers and exploration companies were the primary detractors, with Exxon Mobil, Chevron, ConocoPhillips, and EOG Resources contributing significantly to the sector’s decline. Lower commodity prices weighed on earnings expectations and reduced investor interest in the traditionally defensive energy trade.

Real Estate also lagged the broader market, falling 3.3% during the week. The sector faced headwinds from persistent concerns surrounding interest rates and commercial property fundamentals. Higher financing costs continued to pressure property valuations and future growth expectations. Large real estate investment trusts focused on commercial, industrial, and specialized property segments were among the largest detractors, as investors favored higher-growth sectors over income-oriented investments.

Overall, the week highlighted investors’ preference for growth-oriented sectors tied to innovation and economic expansion, while energy and interest-rate-sensitive areas faced renewed pressure. Market leadership remains concentrated in sectors benefiting from strong earnings momentum and long-term structural growth trends.