COMMENTARY:

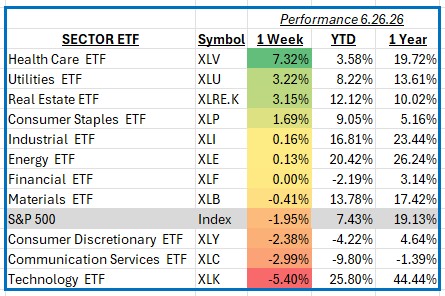

The S&P 500 declined 1.95% for the week ending June 26, 2026, as investors balanced encouraging economic data against renewed concerns over valuations in several of the market’s largest technology companies. Markets were influenced by continued expectations that inflation is gradually moderating, while investors also evaluated Federal Reserve commentary for clues on the timing of future interest rate reductions. Defensive sectors benefited from the shift in sentiment as investors favored companies with stable earnings and attractive dividend characteristics over higher-growth areas of the market.

Health Care was the week’s strongest-performing sector, advancing 7.3% as investors rotated toward defensive industries amid broader market weakness. Strong earnings outlooks, continued demand for innovative treatments, and renewed optimism surrounding pharmaceutical and medical technology companies helped lift the sector. Large-cap pharmaceutical firms, including Eli Lilly, Johnson & Johnson, Merck, and AbbVie, were among the primary contributors to performance, while medical device manufacturers also posted solid gains. The sector’s combination of earnings stability and relatively attractive valuations made it a preferred destination for investors seeking reduced volatility.

Utilities also delivered impressive gains, returning 3.2% during the week. Falling Treasury yields improved the relative appeal of dividend-paying stocks, while expectations for a more accommodative monetary policy supported interest-rate-sensitive sectors. Investors continued to favor regulated electric and gas utilities for their dependable cash flows and defensive characteristics. Leading contributors included NextEra Energy, Southern Company, Duke Energy, Constellation Energy, and American Electric Power, all of which benefited from increased investor demand for stable income-producing investments.

Technology was the weakest-performing sector, falling 5.4%, as investors locked in profits following the group’s strong gains earlier this year. Several large-cap semiconductor and software companies experienced notable selling pressure amid concerns that valuations had become increasingly stretched. Weakness among NVIDIA, Microsoft, Apple, Broadcom, and Advanced Micro Devices accounted for much of the sector’s decline, outweighing strength in select software companies. Investors also reassessed expectations for artificial intelligence-related spending following the sector’s substantial year-to-date rally.

Communication Services declined 3.0%, pressured primarily by weakness among several of its largest internet and digital advertising companies. Shares of Alphabet and Meta Platforms retreated as investors reduced exposure to higher-growth technology-related businesses, while Netflix also traded lower following recent gains. Although advertising fundamentals remain healthy, the sector underperformed as investors rotated toward more defensive areas of the market.

Overall, the week highlighted a clear shift toward defensive positioning as investors favored sectors offering stable earnings and dependable cash flows. While short-term volatility may persist, economic fundamentals remain relatively resilient, and market participants will continue watching upcoming inflation reports, corporate earnings, and Federal Reserve policy for direction during the second half of the year.