COMMENTARY:

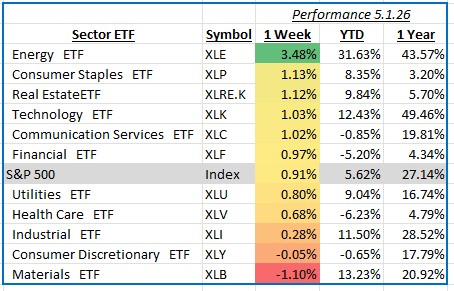

The S&P 500 advanced 0.91% for the week ending May 1, 2026, extending its recent winning streak as investors responded positively to another strong round of corporate earnings and resilient economic data. Markets were supported by continued strength in large-cap technology companies, easing concerns around oil prices late in the week, and evidence that the U.S. economy remains on stable footing despite elevated inflation pressures. Investors also monitored developments in the Middle East and commentary from global central banks as volatility in energy markets remained a key theme.

Energy was the top-performing sector this week, gaining 3.5%, as higher crude oil and natural gas prices continued to support investor sentiment. The sector benefited from ongoing geopolitical tensions tied to global supply disruptions and expectations for sustained energy demand. Integrated oil majors and exploration and production companies led the advance, with Exxon Mobil, Chevron, and ConocoPhillips among the strongest contributors. Investors were also attracted to the group’s strong free cash flow generation, dividend support, and defensive characteristics during periods of inflation uncertainty.

Consumer Staples also delivered solid performance, rising 1.1% for the week as investors rotated toward more defensive areas of the market. The sector benefited from continued demand for household products and packaged foods, while stable earnings expectations helped support valuations. Large multinational companies including Procter & Gamble, Costco, Coca-Cola, and Walmart contributed positively as investors favored businesses with resilient pricing power and dependable cash flows amid ongoing inflation concerns and uncertainty surrounding interest rate policy.

Materials lagged the broader market, declining 1.1% during the week as weaker metals prices and concerns about slowing global industrial demand weighed on the group. Investors remained cautious around the outlook for construction activity and manufacturing growth, particularly in China and Europe. Commodity-sensitive names, including mining and chemical companies, pressured returns, with weaker performance from firms tied to copper, steel, and industrial chemicals offsetting relative strength in select packaging and specialty materials businesses.

Overall, markets closed the week on a constructive note as strong earnings and steady economic activity continued to outweigh concerns surrounding inflation, interest rates, and geopolitical uncertainty.