COMMENTARY:

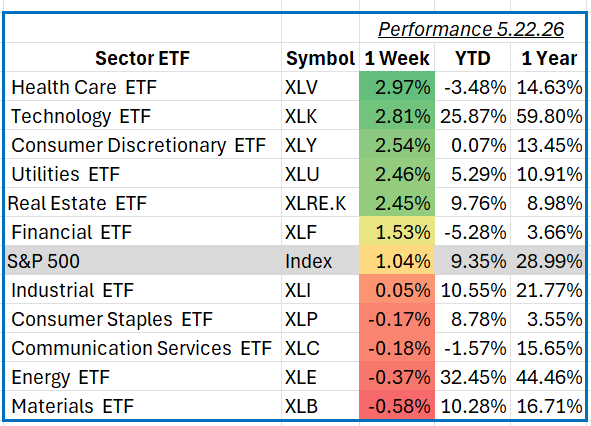

The S&P 500 advanced 1.04% for the week ending May 22, 2026, as investors continued to balance resilient corporate earnings with evolving expectations for monetary policy and economic growth. Market sentiment improved during the week following encouraging inflation data and signs that consumer spending remains stable despite elevated interest rates. Investors also responded positively to continued strength in artificial intelligence-related capital spending and improving outlooks from several large-cap technology companies. Meanwhile, Treasury yields stabilized after recent volatility, helping support equity valuations across growth-oriented sectors.

Technology led the market higher this week, gaining 2.8% as investors continued to favor companies tied to artificial intelligence infrastructure, cloud computing, and semiconductor demand. The sector benefited from strong earnings momentum and optimistic commentary surrounding enterprise technology spending trends. Large-cap semiconductor and software companies were among the primary contributors to performance, with gains led by Nvidia, Microsoft, Broadcom, and Apple. Investor enthusiasm surrounding AI adoption remained a dominant theme, while easing bond yields also supported higher valuations for growth-oriented technology shares.

Consumer discretionary stocks also posted solid gains, rising 2.5% for the week as consumer spending trends remained resilient and several retailers reported stronger-than-expected results. Improving confidence around household balance sheets and continued strength in travel and entertainment activity supported the sector. Amazon and Tesla were among the largest contributors to returns, while gains in home improvement and online retail companies also added to sector performance. Investors appeared encouraged by signs that higher-income consumers continue to spend despite persistent inflation pressures.

Communication services also contributed positively to overall market performance during the week, supported by strength in internet, streaming, and digital advertising companies. Continued momentum in online advertising demand and improving engagement trends lifted several large-cap media and platform businesses. Alphabet and Meta Platforms were key drivers of returns as investors responded favorably to ongoing AI integration initiatives and disciplined expense management across the sector.

Materials lagged the broader market, declining 0.6% amid weaker commodity prices and concerns surrounding slowing global industrial demand. Mining, chemicals, and packaging companies faced pressure as investors evaluated softer manufacturing data from overseas markets and mixed signals on construction activity. Weakness in copper and steel producers weighed on returns, while declining precious metals prices also limited performance within the sector.

Overall, markets finished the week on a constructive note as investors remained focused on earnings strength, moderating inflation trends, and the outlook for economic growth heading into the summer months.