COMMENTARY:

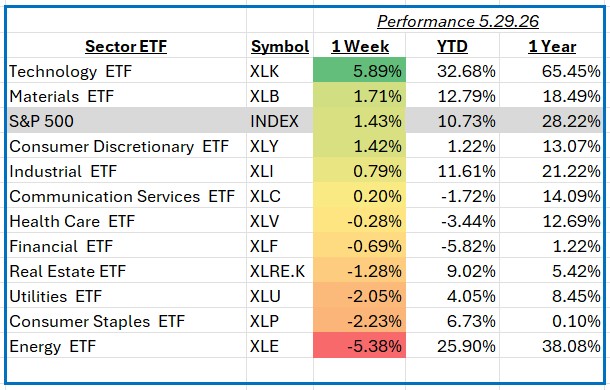

The S&P 500 delivered a strong gain of 1.43% for the week ending May 29, 2026, supported by encouraging economic data, resilient corporate earnings, and renewed optimism surrounding artificial intelligence-related investments. Investors responded positively to signs that inflation continues to moderate while economic growth remains steady. In addition, expectations that the Federal Reserve may have greater flexibility to ease monetary policy later this year helped support risk assets. Strong earnings results from several large-cap companies further reinforced confidence in the outlook for corporate profits and economic activity.

Technology was the strongest-performing sector of the week, advancing 5.9%. Performance was driven by continued enthusiasm surrounding artificial intelligence infrastructure spending, as well as strong earnings and guidance from several semiconductor and software companies. Large-cap technology leaders were the primary contributors to sector gains, with notable strength from NVIDIA, Microsoft, Broadcom, and Apple. Investor demand remained concentrated in companies positioned to benefit from growing data center investment, cloud computing expansion, and AI adoption. Lower interest rate expectations also provided an additional tailwind for growth-oriented technology stocks, which tend to benefit from declining discount rates.

Materials also posted a positive week, gaining 1.7%. The sector benefited from improving sentiment toward global manufacturing activity and expectations for increased infrastructure and industrial spending. Strength in industrial metals prices supported many of the sector’s largest holdings, while improving demand expectations helped lift chemical and specialty materials companies. Leading contributors included Linde, Sherwin-Williams, and Freeport-McMoRan, as investors favored companies with exposure to industrial production, construction activity, and long-term electrification trends. The sector also benefited from a generally favorable backdrop for commodity-related businesses.

Energy was the weakest-performing sector, declining 5.4% during the week. The primary headwind was a notable pullback in crude oil prices as investors weighed concerns about global demand growth and increasing supply expectations. Integrated energy producers and exploration companies led the decline, with Exxon Mobil, Chevron, and ConocoPhillips among the largest detractors. Lower commodity prices pressured earnings expectations across the sector, while investors rotated capital toward higher-growth areas of the market. Despite the week’s weakness, energy companies continue to generate significant cash flow and maintain generally healthy balance sheets.

Overall, markets finished the week on a constructive note, supported by improving economic conditions, moderating inflation pressures, and strong corporate earnings, with growth-oriented sectors leading the advance.