COMMENTARY:

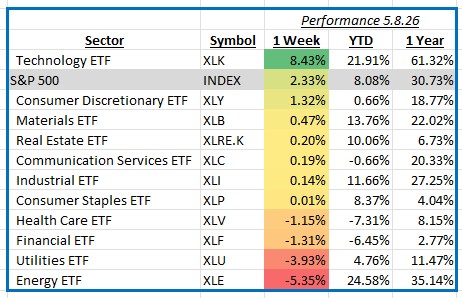

The S&P 500 delivered a strong rebound during the week ending May 9, 2026, gaining 2.33% as investors responded positively to improving sentiment around economic growth, corporate earnings, and expectations for monetary policy later this year. Markets were supported by continued resilience in labor market data and easing concerns that inflation pressures could reaccelerate. Investor optimism also improved following several large-cap earnings releases that highlighted ongoing strength in artificial intelligence spending, digital infrastructure demand, and consumer activity. Treasury yields remained relatively stable during the week, helping support higher-growth areas of the market.

Technology was the strongest-performing sector of the week, advancing 8.4% as investors aggressively rotated back into growth-oriented companies tied to artificial intelligence, semiconductors, cloud computing, and digital infrastructure. Strong earnings guidance and renewed capital spending expectations across the AI ecosystem fueled broad participation throughout the sector. Semiconductor manufacturers and mega-cap platform companies were among the largest contributors to performance, with gains led by companies such as NVIDIA, Microsoft, Apple, and Broadcom. Investor confidence was further supported by expectations that enterprise technology spending could remain durable even amid a slowing economic backdrop.

Consumer Discretionary also posted positive returns for the week, rising 1.3% as investors favored companies benefiting from resilient consumer demand and improving sentiment around household spending trends. Strong performance among internet retail, travel, and select automotive-related companies supported gains across the sector. Shares of Amazon and Tesla were among the largest positive contributors as investors responded favorably to improving revenue expectations and continued consumer engagement. Strength in online advertising and digital commerce trends also helped support broader sector performance.

Energy was the weakest-performing sector, declining 5.4% as crude oil prices moved lower amid concerns about slowing global demand growth and rising supply expectations. Commodity markets reacted negatively to softer economic data from several international markets and ongoing uncertainty surrounding future production levels from major exporting countries. Large integrated energy producers and exploration companies weighed heavily on returns, with notable weakness from Exxon Mobil, Chevron, and ConocoPhillips. Lower oil prices also pressured earnings expectations across the broader energy complex.

Overall, markets ended the week on a constructive note as investors balanced encouraging corporate earnings trends with ongoing macroeconomic uncertainty. Leadership from growth-oriented sectors continued to drive broader market gains while commodity-sensitive areas faced renewed pressure.