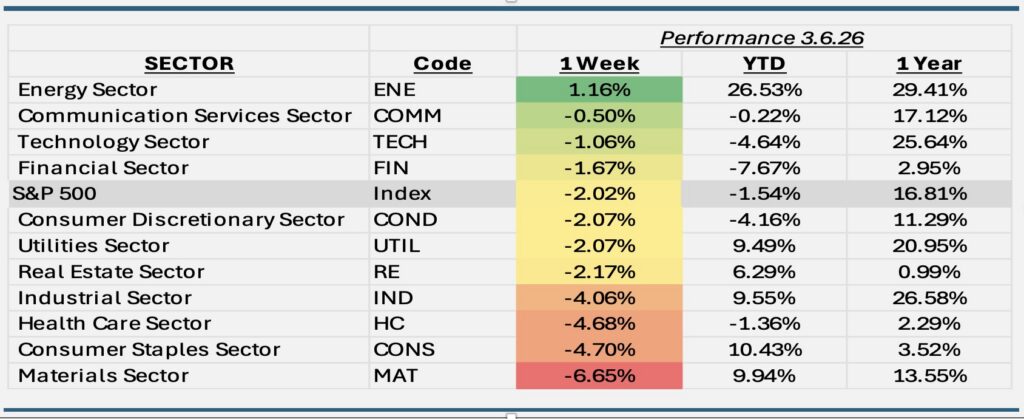

The S&P 500 fell 2.0% for the week, marking its worst weekly decline since October as markets digested a rare combination of geopolitical tension, energy driven inflation pressure, and softening U.S. economic data. Risk appetite deteriorated steadily, culminating in a broad selloff on Friday.

- Crude oil surged to its highest level in over two years as the conflict in Iran escalated, raising fears of prolonged supply disruptions. The February payrolls report came in below expectations, reinforcing concerns that the labor market is losing momentum. Equity weakness was broad based across global markets. The U.S. dollar strengthened, gold was surprisingly muted, and volatility rose sharply as investors sought liquidity over traditional havens.

- Energy was the only sector to finish the week in positive territory (+1.2%), supported by the sharp rise in crude prices. Exxon Mobil (XOM) and Chevron (CVX) were the most impactful contributors, benefiting from widening upstream margins and renewed investor demand for inflation resilient assets

- Materials was the worst performing sector (+6.7%), pressured by global growth concerns and rising input costs. Chemical producers and industrial metals names sold off sharply as investors reassessed demand expectations. Linde (LIN) and Freeport McMoRan (FCX) were among the largest detractors, reflecting weakness in both specialty chemicals and copper markets.

- Consumer Staples underperformed (-4.7%) as investors rotated away from defensives amid concerns that higher energy prices could squeeze margins and dampen consumer spending. Procter & Gamble (PG) and Coca Cola (KO) were notable laggards, with both facing pressure from rising commodity costs and a stronger U.S. dollar. The sector’s traditionally stable profile offered little insulation in a week dominated by inflation fears.

- Equities ended the week on a decisively negative note as investors grappled with geopolitical uncertainty, inflationary energy shocks, and softening economic data. While the S&P 500 remains within a few percentage points of its highs, the week underscored the market’s sensitivity to macro volatility. Leadership narrowed, defensives failed to provide shelter, and Energy stood alone as the beneficiary of the shifting landscape.

ETF Tidbits:

In the ETF world, income‑focused and options‑based ETFs continued to attract steady interest as investors looked for ways to generate yield while managing volatility. Crypto‑linked ETFs also remained active, with strong trading volumes and ongoing product filings keeping the category in the spotlight. Regulators continued to focus on clear disclosures and marketing practices, especially for complex or derivatives‑based ETFs.

New SMRF ETF – no not those guys (little blue characters who live in a carbon free environment). It’s a New Actively Managed SMR Focused Nuclear Technology ETF launched on February 19th 2026, the ALPS Nautilus SMR Nuclear & Technology ETF. It also uses an option overlay for income and performance enhancements. The fund is currently based off the SMRFX Index, by Nautilus Indexes the sister company to ETF Insight, and index partner Vetta Fi. Patrick and Mike form the research team for the index and will manage an actively managed model on the portfolio companies in ETF Themes.