April 15, 2026

The question of US versus international equities has rarely been more consequential, or more genuinely difficult to answer, than it is right now. The backdrop is not a clean macro cycle where one playbook dominates. It is a geopolitically fractured world where energy security, AI-driven earnings divergence, shifting trade alliances, and a weakening dollar are all pulling in different directions simultaneously. Getting the geographic allocation right through the end of April and into the summer may matter as much as getting sector selection right.

The short answer is this: the case for international equities is stronger than it has been in years, but it is not yet strong enough to justify abandoning US earnings leadership. The better frame is a deliberate reduction in US overweight combined with targeted exposure to specific international markets, rather than a wholesale rotation.

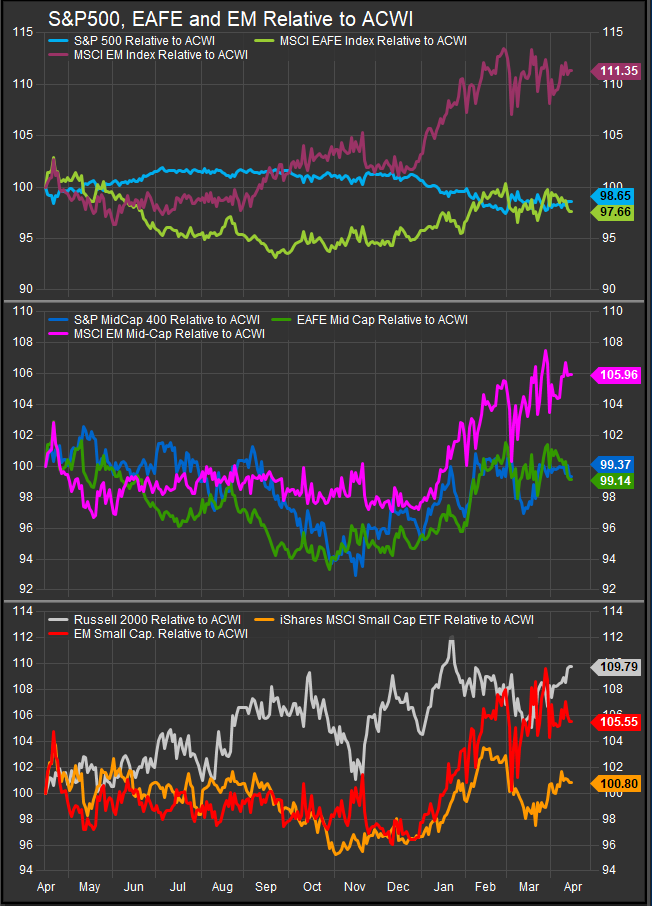

EAFE stocks (top panel) have lagged in the near-term while US and EM equities have been primary beneficiaries of the recent bullish impulse into the equity market.

The US case: earnings leadership is real, but crowded

Start with what the US has going for it. S&P 500 earnings growth of +12.6% year-over-year in Q1 would mark the sixth consecutive quarter of double-digit growth, and the Technology sector is expected to deliver +45%, with semiconductors projected at +95%, led by Nvidia at +117% and Micron at +167%. TSMC just reported $35.6 billion in Q1 revenue, up 33% year-over-year, confirming that AI-driven demand is not slowing. Amazon’s AWS AI revenue run rate hit $15 billion in Q1, and Anthropic is now being valued at approximately $800 billion in a new funding round, up from $350 billion just two months ago.

That earnings engine is real and it is largely a US story. No other market in the world has the same concentration of AI infrastructure, semiconductor design leadership, and hyperscaler capital spending. Goldman Sachs estimates that AI-related stocks will drive more than 60% of S&P 500 EPS growth in Q1, with Nvidia and Micron alone accounting for roughly half of index-level earnings growth.

But that concentration is also the risk. The BofA Global Fund Manager Survey shows investors are already net 10% underweight US equities, the least overweight since July 2025, even as they remain constructive on the medium-term outlook. Growth expectations fell by the largest margin since March 2022. Geopolitical conflict is now cited as the biggest tail risk by 44% of fund managers, up 30 percentage points over two months. The market that has done the most in recent years is now the market most exposed to sentiment reversals, energy-driven earnings headwinds, and the growing risk that AI optimism becomes harder to monetize in the near term.

The Iran conflict adds another layer. Energy costs are rising sharply, with gasoline averaging $4.153 per gallon nationally, up 17.3% month-over-month. Airlines are absorbing a $2 billion fuel hit in June quarter. Consumer sentiment hit a record low of 47.6 in the April UMich reading. These are not abstract macro risks. They are earnings headwinds for US consumer and transportation businesses that will show up in guidance over the next several weeks.

The international case: improving, and underappreciated

Against that backdrop, international equities are beginning to look more attractive for reasons that are both structural and tactical.

Europe is arguably the clearest near-term opportunity. European leaders are actively developing plans to ensure the continent can defend itself independently of the US, which implies a sustained increase in defense spending with direct implications for European industrial and aerospace companies. The European Central Bank still has room to cut rates more aggressively than the Fed in a slowing environment, which gives European equities a different monetary policy tailwind. And after years of valuation discount, European markets carry significantly more room for multiple expansion relative to their US counterparts.

The currency dynamic also matters. A weaker dollar — which tends to accompany periods of US geopolitical stress and Fed easing expectations — is a direct tailwind for unhedged international equity returns. When the dollar weakens, foreign earnings translate back into more dollars for US-based investors, amplifying the underlying return.

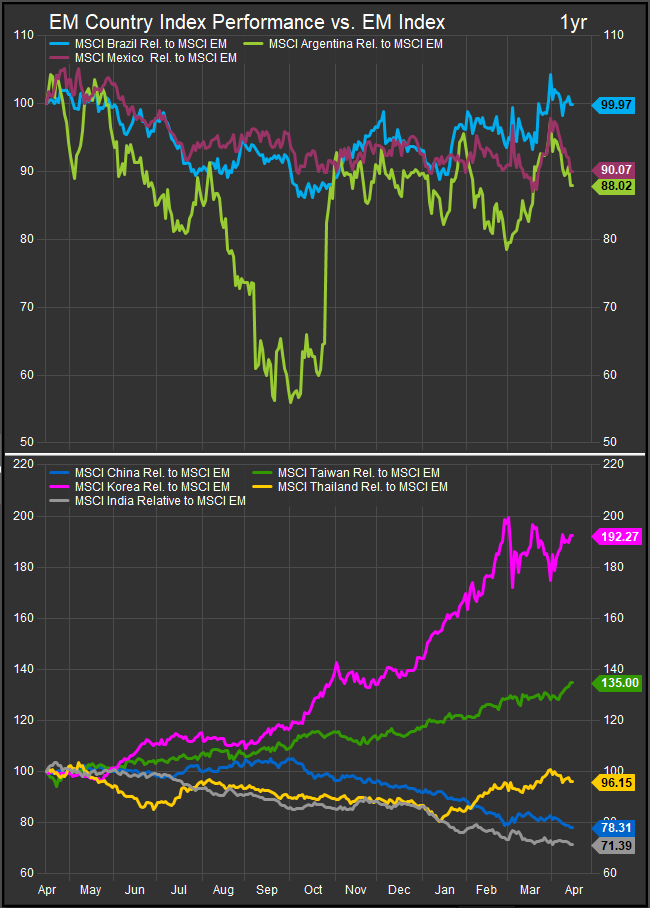

Emerging markets present a more nuanced picture, but one that is increasingly interesting. China’s Q1 GDP growth is expected to have picked up, and China is resuming some ties with Taiwan following a visit by an opposition leader, which modestly reduces near-term geopolitical tail risk on that front. India and South Korea are facing near-term pressure from oil price exposure, but their longer-term positioning within the AI supply chain remains intact. ASML just raised its full-year sales forecast on AI-driven chip equipment demand, and that story benefits Asian manufacturers directly.

The BofA survey is instructive here. While overall sentiment has deteriorated, the survey shows investors moving away from the US and toward international markets more broadly. That rotation is still early and still cautious, but the direction is increasingly clear.

The key risks to the international call

This is not a simple story. Three risks deserve attention before tilting hard toward international.

First, the Iran conflict creates asymmetric energy exposure for international markets. India and China are identified in today’s headlines as most at risk from the US naval blockade of the Strait of Hormuz. South Korean import inflation just hit a three-year high due to oil price surges. France’s inflation is already running above initial estimates because of energy costs. The same geopolitical shock that pressures US consumer spending can hit energy-importing international economies even harder.

Second, earnings growth outside the US is simply not as strong. The US earnings machine, led by Technology and Financials, is running at a pace that few international markets can match. European earnings growth has been more modest, and emerging market earnings remain highly variable by country and sector. Investors rotating out of the US need to accept a lower growth rate in exchange for better valuations and diversification.

Third, the AI story is still largely a US story. The hyperscalers, the leading semiconductor designers, and the frontier AI model developers are predominantly US-based. International exposure gives investors diversification and valuation relief, but it does not replicate the earnings leverage to AI capex that makes the US so compelling in a strong growth environment.Taiwan and Korea remain top Growth stories linked to the Semiconductor and AI Boom. These stocks are part of both US and Chinese AI value chains and screen as top ideas.

Continued resource demand will be key for nascent bullish reversals in LATAM while Korea and Taiwan are top AI-theme exposures within EM.

How to position

The practical conclusion is a structured reduction in US overweight rather than an outright rotation. Through the end of April, the most defensible positioning looks like this.

Within the US, maintain conviction in semiconductors, AI infrastructure, and Financials, where earnings visibility is highest and the Q1 reporting setup is strongest. Reduce or avoid broad consumer exposure, software, and anything that depends on discretionary spending holding up as fuel prices squeeze real incomes.

For international developed markets, Europe stands out as the most compelling incremental allocation, particularly through defense, industrial, and financial exposure that benefits from higher European defense spending, ECB easing optionality, and relative valuation. The iShares MSCI EAFE ETF (EFA) has already posted +3.0% over one month and +8.5% over six months, with positive year-to-date flows, and the EAFE Value fund (EFV) has added +17.1% over six months. Those numbers are not outliers. They reflect a genuine shift in where value and momentum are beginning to align.

For emerging markets, be selective. China’s domestic-facing economy and AI infrastructure buildout offer more interesting opportunities than export-dependent manufacturers facing oil-driven cost pressure. India remains a longer-term structural story, but faces near-term headwinds from energy exposure.

News and data sourced from Factset Research Systems Inc. and StreetAccounts.