March 4, 2026

Near-Term Selling in Korea and Japan: Risk Shock, Positioning Unwind, and Currency Cross-Currents

The sharp downdraft in South Korean and Japanese equities looks less like a “fundamental repricing” and more like a classic macro risk shock colliding with crowded positioning. The immediate catalyst is the Middle East escalation and the associated jump in energy risk premia, which has tightened global financial conditions and triggered de-risking across cyclicals, exporters, and high-beta technology. That dynamic has been amplified by mechanical selling (VaR/risk-parity deleveraging, margin calls) and by the signal from U.S. semiconductors: when the SOX complex breaks hard, Korea’s index-level exposure and Japan’s global cyclicals tend to get hit disproportionately.

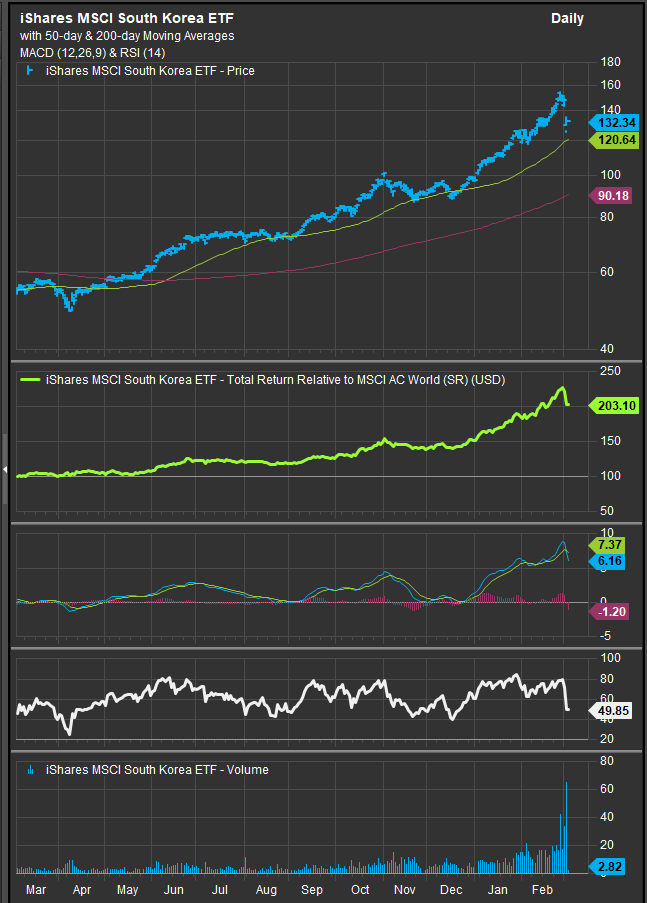

EWJ: Trading into near-term support between the 80 and 84 levels

EWY: Strongest global outperformance trend pulling back to the 50-day m.a., A violation to the downside would be the negative signal for Korean Equities

What’s driving the selloff

1) Energy shock + terms-of-trade vulnerability (especially Korea).

South Korea is unusually sensitive to Middle East-driven oil spikes because it is a large energy importer and its equity index is heavily tilted toward global trade and manufacturing. Reuters described the episode as Korea’s worst trading day, with the won hitting a multi-year low intraday and officials signaling readiness to deploy market-stabilizing measures. The equity transmission is straightforward: higher oil raises input costs, squeezes margins in energy-intensive sectors, and increases inflation uncertainty—pushing investors to demand a higher risk premium.

2) Forced deleveraging and “mechanical” selling.

Reports of panic selling and margin calls in Korea are consistent with a positioning unwind rather than a slow-moving earnings reappraisal. When volatility spikes and indices gap lower, leveraged and risk-targeting strategies sell first and ask questions later. Bloomberg similarly framed the move as an abrupt derisking episode with volatility gauges jumping to crisis-era levels.

3) Tech/export beta and global risk-off transmission.

Korea’s market is dominated by global tech and export champions, so any combination of (a) U.S. semis weakness, (b) higher oil, and (c) FX volatility creates a self-reinforcing loop: weaker equities → weaker currency → higher hedging costs / more outflow pressure → weaker equities. Reuters highlighted heavy losses in major Korean bellwethers alongside the won’s sharp move.

4) Japan: broad risk aversion plus cyclicals/financials pressure.

Japan’s selloff appears to be the “global beta” version of the same shock. Rising uncertainty around the duration of Middle East conflict pushes investors toward caution, while oil sensitivity (import costs) complicates the inflation/growth mix. Reuters also noted the yen’s moves and the policy constraint: higher oil can raise inflation while also threatening growth, limiting how cleanly the policy outlook can be read.

How likely is it to continue?

Continuation risk is real in the very near term, but it’s conditional—not inevitable.

- If oil stays elevated and headlines imply a longer campaign, equity volatility can remain high and selling can persist, particularly in Korea where the currency channel tends to amplify stress. Broad global coverage has emphasized the energy-price shock as a central driver of the latest risk-off wave.

- If volatility remains high, systematic strategies tend to keep exposure constrained. That means rallies can be “sold into” until realized volatility compresses.

- If policymakers lean in, stabilization often follows. Korea has a playbook (verbal guidance, liquidity support, monitoring short-selling dynamics, FX smoothing) and Japan has historically used rhetoric and the threat of intervention to dampen disorderly FX moves.

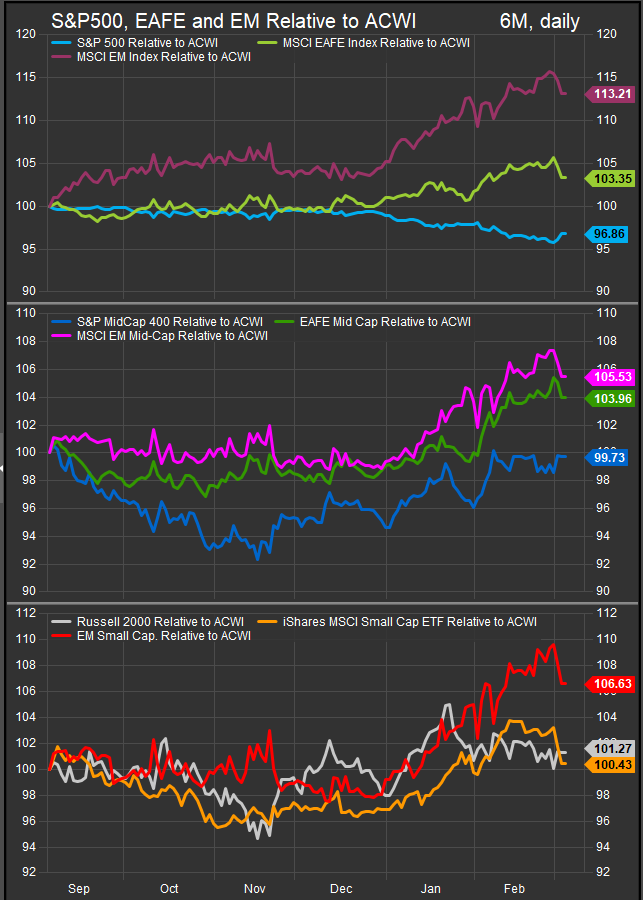

Bottom line: the next 1–2 weeks are likely to be driven more by energy and geopolitics than by micro fundamentals. Once oil volatility cools, the probability of stabilization rises quickly—especially given the amount of mechanical selling already implied by the size of the move. If USD remains strong, EM outperformance broadly could be threatened. The chart below shows a nascent US rebound on performance vs. ex-US as investors become concerned about the bull trend’s prospects.

Are currency trends versus USD a factor?

Yes—currency is a second transmission channel and in Korea it can become the dominant one during stress. A key component moving forward will be Fed policy. If US recession odds rise sharply (continued softening employment and GDP) and the Fed leans more dovish, USD weakness could return. If military conflict proves inflationary, we could see a global sell off and risk off moves into USD, EUR and JPY at the expense of EM currency.

South Korea (KRW):

The won’s sharp depreciation matters because it signals capital outflows and raises the cost of hedging for foreign investors. It can also tighten domestic financial conditions via imported inflation and funding markets. Reuters reported the won hit a 17-year low intraday before paring losses, underscoring how currency stress and equity stress were feeding each other. If the won remains volatile, it increases the odds that global investors reduce Korea exposure regardless of near-term valuation.

Japan (JPY):

The yen can behave in two competing ways: a safe-haven bid in global risk-off episodes, or a weaker-yen move if oil prices worsen Japan’s trade/inflation mix and markets reassess policy. Reuters commentary around the yen and oil-linked inflation/growth risks reflects that push-pull. In practice, for Japanese equities the key is not “yen up or down” in isolation—it’s whether FX volatility forces hedgers and systematic strategies to cut exposure.

What to watch next

- Oil and shipping-risk indicators (and any policy actions affecting energy transport/security). If the risk premium compresses, Asian equities can stabilize quickly.

- FX stabilization: KRW steadiness is a leading indicator for Korea equities; JPY volatility is a leading indicator for Japan equity hedging flows.

- U.S. semis / global tech leadership: Korea is effectively a leveraged expression of global semis risk appetite.

- Local policy signaling: any credible steps to curb disorderly trading conditions can reduce tail-risk premia.

Sources

- Reuters — South Korean stocks’ record slide and won weakness amid Middle East conflict

- Reuters — Japan finance minister comments on FX vigilance; yen dynamics amid oil-risk backdrop

- The Guardian — Global market reaction and energy-price surge tied to Middle East war

Bloomberg — Korea selloff/volatility spike framing