March 18, 2026

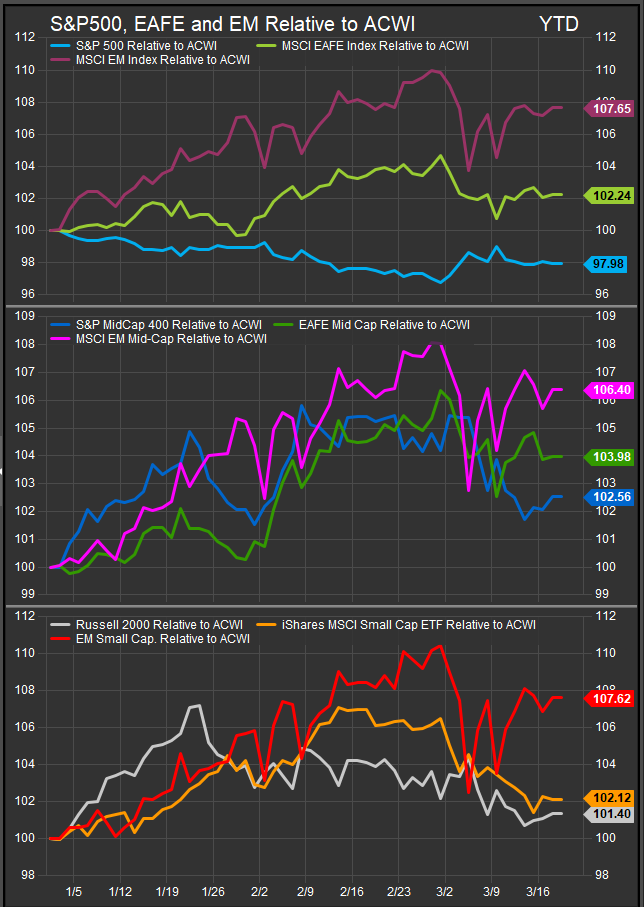

Typically, we discuss ex-US economies and equity markets that are showing strength and have potential for sustained outperformance in these features. This week is a change of pace as we are examining the recent flip in global equity leadership dynamics as investors have rotated back into US shares and away from ex-US. The following is an analysis of the drivers of that rotation.

The transition from contained tensions to open hostilities with Iran has introduced a classic macro shock—one defined by surging oil prices, rising volatility, and renewed uncertainty around global growth. Yet the most important market development has not been the drawdown itself, but the clear reassertion of U.S. equity leadership relative to international markets. This shift reflects more than a defensive rotation. It is rooted in structural differences across economies, earnings profiles, and capital flows that become more pronounced when energy markets are disrupted.

At the center of this divergence is the oil shock. Crude prices have surged sharply, with Brent briefly reclaiming $100 per barrel and weekly gains exceeding 25%, driven by disruptions in and around the Strait of Hormuz—a channel that facilitates roughly a fifth of global oil and LNG flows. That magnitude of disruption does not translate evenly across regions. For much of Europe and Asia, higher oil prices function as a direct tax on growth. These economies remain heavily dependent on imported energy, and rising input costs feed quickly into industrial margins, transportation costs, and consumer inflation. By contrast, the United States enters this period as a major energy producer. While higher gasoline prices still weigh on the consumer, the domestic energy complex benefits from rising prices, and the broader economy absorbs the shock with far less external strain. That asymmetry alone begins to explain why U.S. equities have held up better.

The composition of equity markets reinforces this advantage. U.S. indices are heavily concentrated in technology and communication services—sectors that are structurally less sensitive to energy input costs and more levered to secular growth drivers such as artificial intelligence and digital infrastructure. These businesses tend to have high margins, global revenue streams, and limited dependence on physical inputs. In contrast, international markets carry greater weight in industrials, materials, and export-oriented manufacturing. These sectors sit directly in the path of an energy shock, facing both higher costs and the risk of slowing end demand. As a result, even before considering valuation, investors are increasingly discounting a relative earnings resilience premium for U.S. equities.

Capital flows have amplified this divergence. Periods of geopolitical stress tend to concentrate liquidity into the deepest and most transparent markets, and the United States remains the primary destination for global risk capital. Even with elevated Treasury volatility and shifting rate expectations, U.S. assets continue to offer a combination of scale, liquidity, and perceived stability that international markets struggle to match. At the same time, higher oil prices are complicating the macro backdrop abroad. Emerging markets face deteriorating trade balances and tighter financial conditions, while developed markets confront renewed inflation pressures without the same policy flexibility. The result is a steady reallocation of capital back into U.S. equities, reinforcing relative outperformance.

Positioning has also played a meaningful role in the speed of the move. Leading into the conflict, investors had begun rotating toward international equities and cyclicals, while U.S. Growth exposure had been pared back amid valuation concerns and questions around AI monetization. The escalation in geopolitical risk forced a rapid reversal. Hedge fund leverage declined sharply, systematic strategies de-risked, and short positioning increased across global markets. In that environment, capital did not simply move to cash—it rotated toward assets perceived as more resilient. U.S. large-cap equities, particularly in Growth and Quality segments, became the natural destination. The unwind of prior positioning has therefore acted as an accelerant, not just a backdrop, to the performance gap.

Policy credibility and flexibility further support the U.S. advantage. While no economy is immune to an energy shock of this magnitude, the United States retains a more adaptive policy framework, deeper capital markets, and a central bank that is still viewed as capable of responding to evolving conditions. In contrast, European policymakers face tighter fiscal constraints, and emerging markets must navigate the competing pressures of inflation, currency stability, and growth. These differences are subtle in stable periods but become critical during times of stress, shaping investor confidence and capital allocation decisions.

Taken together, the outperformance of U.S. equities is not a temporary anomaly—it is the market expressing a clear preference for economic insulation, earnings durability, and liquidity in the face of an energy-driven geopolitical shock. The Iran conflict has not created these dynamics, but it has brought them into sharper focus. As long as oil remains elevated and global trade flows remain uncertain, the structural advantages embedded within U.S. markets are likely to persist.

For investors, the implication is straightforward. This is not simply a question of risk-on versus risk-off. It is a question of where the risk resides. In the current environment, that risk is disproportionately concentrated in energy-importing economies and cyclically exposed sectors. Until that changes, U.S. equities are likely to remain on the more favorable side of the global equity allocation decision.

FactSet / StreetAccount – Daily macro and sector performance summaries, including oil price moves, equity factor rotations, and regional market performance trends.

Bloomberg – Coverage of Strait of Hormuz disruptions, Brent crude surpassing $100, Treasury volatility, and global capital flow dynamics during the Iran conflict.

Reuters – Reporting on tanker attacks, oil supply disruptions, and the macroeconomic impact of rising energy prices on Europe and Asia.

Financial Times – Analysis of energy dependency across regions, fiscal constraints in Europe, and global trade risks tied to Middle East instability.

International Energy Agency (IEA) – Data on global oil flows, share of supply moving through Hormuz (~20%), and emergency reserve releases.

U.S. Energy Information Administration (EIA) – Statistics on U.S. energy production versus import dependency across global economies.

Goldman Sachs / JPMorgan Research – Positioning data (panic index, hedge fund leverage, ETF short flows) and insights into factor rotation and market technicals.