April 2, 2025

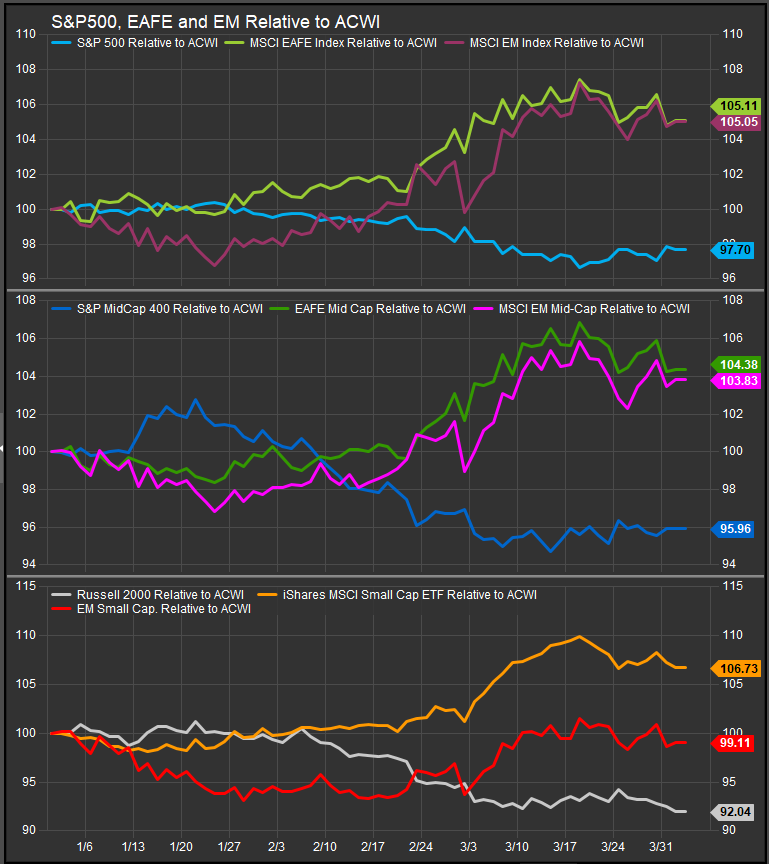

The rotation out of US Stocks has hit its first potential pivot point at the start of April. The S&P 500 is retesting March lows after the end-of-month rally got snuffed out at the 200-day moving average last Friday. The rally came at the expense of ex-US equity performance. The chart below shows the YTD dynamic between US, EAFE and EM equities. From January 27th – March 20th, we saw sharp rotation into EM and EAFE equities across all market cap. tiers at the expense of domestic stocks. Whether this is a pause, or a reversal of the trend matters a lot.

One of the key aspects underpinning the S&P 500’s 2023-2024 bull market trend was the exceptional growth potential and earnings profile of the Mag7 in combination with the US Information Technology Sector. Neither enclave of extremely large stocks was like anything found overseas at the time… Chinese Growth stocks were bottoming out and Europe was facing the same post-inflationary hangover that many areas of the Value trade confronted domestically. Continued ex-US outperformance would be a clear signal that investors have shifted their focus past discounting AI’s growth potential to other concerns. The most obvious one is the impact of new tariff policies that have dominated the news flow.

The tariff dynamic sets the table for volatility in both directions. However, its biggest impact on the discounting machine that is the stock market has been its effect on perceptions about Fed policy. If inflation concerns from a potential trade war materialize the Fed can’t aggressively ease and recession probability increases. At the risk of oversimplifying, that’s where we are. More movement away from US stocks would be a sign that recent discounting in former leadership isn’t enough of an incentive to attract accumulation given the new risks.

US Sector Performance Offers a Similar Message

US sector performance is at a similar pivot point. March was a clear unwind away from the Mega Cap. Growth trade. Technology and Discretionary Sectors were pummeled relative to the broad market while Commodity-linked sectors (chart below, top panel), and lower vol. sectors (middle panel) made gains along with Financials. We expect Discretionary and Technology sector performance to bounce when the market bounces. The signal develops if/when they outperform when the tape is down.

Conclusion

Tariff concerns have made the US economic expansion look more vulnerable in the eyes of equity investors. The performance spread that developed over the 2023-2024 US bull market has retraced, but market participants are still struggling to understand the scope of downside risk for stocks. If we see a continuation of February-March performance as April begins, we can gain conviction that the next move for US stocks is likely to be lower and key Mega Cap. Growth names have further to fall before their discount is compelling.

Data sourced from FactSet Research Systems Inc.