Country ETF flows show investors are discounting a stronger global cycle, but not a simple broad risk-on trade. The best support is going to AI manufacturing, developed-market quality, select European cyclicals, and markets that benefit from lower oil. The weakest signals remain in China, commodity-sensitive markets, and countries facing currency, trade, or geopolitical pressure.

The case for improved global factory activity is increasingly data-backed. China manufacturing expanded for a seventh straight month in June and finished its strongest quarter since late 2020. Japan manufacturing also expanded in June and posted its best quarterly performance since early 2014. South Korean export growth remained strong as chip shipments tripled on surging memory demand. The eurozone posted its best manufacturing quarter since early 2022, helped by easing costs, while broader Asian factory activity continued to be supported by the AI boom.

The ETF tape confirms that improvement, but selectively. EAFE (EFA) gained 0.68% over 1 month, 10.43% over 3 months, and attracted $563M of 1-month inflows. Emerging Markets (EEM) were flatter over 1 month at +0.23%, but the medium-term momentum is stronger, with 24.95% 3-month returns and 24.65% 6-month returns, supported by $3.49B of YTD inflows. That split matters: EAFE is acting like a value-heavy developed-market catch-up trade, while EM/Asia is still more leveraged to AI, semiconductors, and Growth optimism.

The factor backdrop is also shifting. In broad U.S. style proxies, Value (VTV) outperformed Growth (VUG) over the past month, with VTV up 3.38% and taking in $2.21B of 1-month inflows, while VUG fell 3.76% despite modest positive inflows. That matters globally because EAFE benchmarks are more value-heavy than EM/Asia exposures. If inflation remains sticky and rates stay elevated, the value-heavy EAFE complex should continue to benefit from financials, industrials, energy-adjacent cash flows, and defensive quality. If rates fall or AI optimism accelerates again, Growth-heavy EM/Asia exposures should regain leadership.

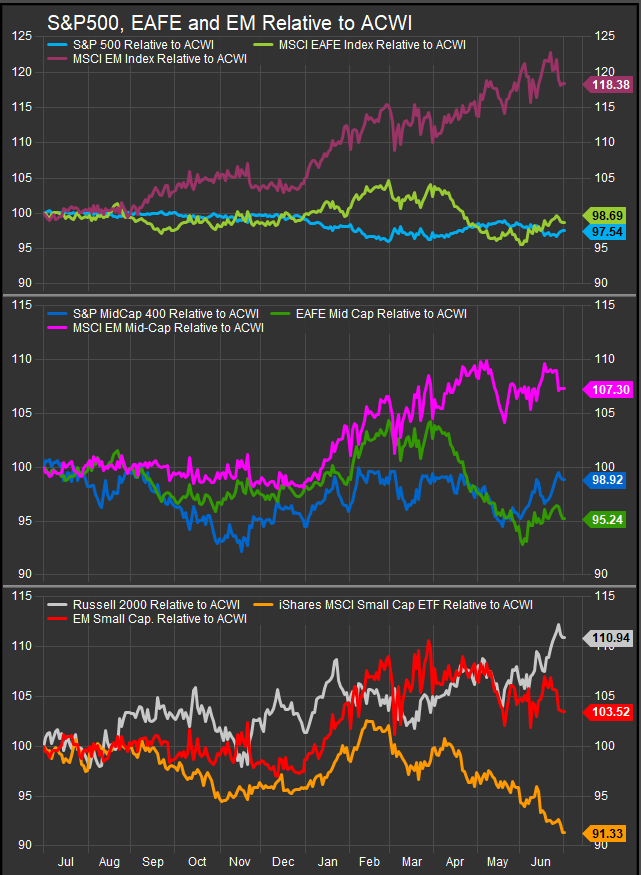

Chart: EM shares (top panel) have been clear leadership over the past 12-months. Recent selling hasn’t broken the trend, but it does set up a potential pivot that will either confirm or deny the longer-term outperformance trend.

Country ETF Flow and Performance Signals

| Country / ETF | 1M Return | 3M Return | 6M Return | 1M Flow | YTD Flow | Message |

| Japan (EWJ) | 0.87% | 15.02% | 15.79% | $939M | $4.16B | Best developed-market AI/industrial inflow story |

| South Korea (EWY) | -1.91% | 73.41% | 104.73% | $729M | $4.25B | Investors buying AI memory weakness |

| Canada (EWC) | -1.53% | 8.40% | 6.65% | $603M | $1.80B | Developed-market quality and resource optionality |

| UK (EWU) | -0.27% | 5.32% | 5.85% | $297M | $711M | Defensive developed-market inflows |

| Switzerland (EWL) | 1.32% | 11.20% | 6.30% | $270M | $341M | Quality/defensive bid remains intact |

| Germany (EWG) | -2.85% | 9.96% | -1.30% | $176M | -$125M | Investors testing cyclical recovery |

| Spain (EWP) | 4.18% | 15.53% | 11.50% | $146M | -$93M | Strong Europe momentum, weaker YTD conviction |

| Netherlands (EWN) | 5.94% | 28.36% | 24.10% | -$16M | $128M | AI equipment exposure working, flows mixed |

| Taiwan (EWT) | 5.67% | 57.50% | 70.48% | -$244M | -$426M | AI leadership, but investors taking profits |

| China (MCHI) | -6.79% | -6.53% | -15.22% | $0 | -$776M | Factory improvement not enough for re-rating |

| Brazil (EWZ) | -3.01% | -5.28% | 8.88% | -$712M | $2.15B | Profit-taking after strong YTD buying |

| Norway (ENOR) | -11.39% | -8.58% | 13.58% | -$13M | $41M | Oil weakness pressuring energy-heavy market |

Japan (EWJ) remains the cleanest international flow story. The fund attracted roughly $939M over 1 month and $4.16B YTD, even though near-term performance was modest. Investors appear to be buying Japan as a diversified AI-adjacent market: semiconductor equipment, factory automation, capital goods, electrical equipment, and improving domestic manufacturing sentiment. Yen weakness remains a risk, but ETF demand is still persistent.

South Korea (EWY) is the highest-conviction AI manufacturing trade in flow terms. The fund has pulled in $729M over 1 month and $4.25B YTD, despite a 1.91% 1-month decline. That is a clear buy-the-dip signal tied to memory demand, chip exports, and AI hardware supply chains. The risk is currency stress, with the won under pressure, but investors are still prioritizing the earnings momentum from memory and AI chips.

Taiwan (EWT) is the key divergence. It gained 5.67% over 1 month, 57.50% over 3 months, and 70.48% over 6 months, but flows remain negative, with $244M of 1-month outflows and $426M of YTD outflows. Investors recognize Taiwan’s AI centrality, but they are managing concentration, geopolitical, and profit-taking risk after a major run.

Europe is improving, especially where factory momentum and value exposure overlap. Spain (EWP), Italy (EWI), Belgium (EWK), Austria (EWO), the Netherlands (EWN), and Switzerland (EWL) all show positive medium-term momentum. The eurozone’s best manufacturing quarter since early 2022 and softer inflation support a more constructive EAFE view. Germany (EWG) is still mixed: $176M of 1-month inflows suggest investors are testing the recovery, but YTD flows remain negative.

China (MCHI) remains the weakest major country signal. Better manufacturing data has not translated into equity confirmation. China (MCHI) fell 6.79% over 1 month, is down 15.22% over 6 months, and remains in $776M of YTD outflows. Investors are still focused on weak domestic demand, Western automaker share losses, trade friction, and policy uncertainty. Hong Kong (EWH) is also weak on price, though inflows suggest some investors are beginning to buy weakness selectively.

Latin America is losing momentum. Brazil (EWZ) remains a large YTD inflow winner, but the fund lost $712M over 1 month and fell 3.01%. That looks like profit-taking and a rotation away from commodity beta as oil-risk premiums fade. Mexico (EWW) is also seeing negative flows, likely reflecting trade uncertainty around USMCA and North American supply chains.

What Investors Are Discounting

Investors are discounting four main developments.

First, global manufacturing is improving, especially in AI-linked Asia and parts of Europe. That supports Japan (EWJ), South Korea (EWY), Taiwan (EWT), the Netherlands (EWN), Singapore (EWS), Spain (EWP), and Italy (EWI).

Second, investors are discounting lower oil as a consumer and inflation relief valve. That helps oil importers and developed-market cyclicals but hurts energy-heavy exposures such as Norway (ENOR), Brazil (EWZ), and parts of the Middle East.

Third, investors are separating AI winners from AI risk. South Korea (EWY) and Japan (EWJ) are attracting capital because their AI exposure is tied to manufacturing, memory, equipment, and infrastructure. Taiwan (EWT) is still performing, but outflows show investors are managing risk after a powerful rally.

Fourth, investors are treating China (MCHI) as a tactical trade rather than a durable allocation. Better factory data is not enough while domestic demand, trade policy, and confidence remain weak.

Most Bullish Developments

The most bullish global development is the manufacturing turn. China, Japan, South Korea, Asia broadly, and the eurozone are all showing better activity. The ETF evidence supports this through strong medium-term momentum in South Korea (EWY), Taiwan (EWT), Japan (EWJ), the Netherlands (EWN), Spain (EWP), Italy (EWI), Austria (EWO), and Greece (GREK).

The second bullish development is the continued AI capex cycle. Chip demand, memory shortages, AI power financing, and data-center infrastructure investment remain powerful drivers. That favors South Korea (EWY), Taiwan (EWT), Japan (EWJ), Singapore (EWS), and the Netherlands (EWN).

The third bullish development is EAFE stabilization. EAFE (EFA) is now positive over 1, 3, and 6 months and attracting 1-month inflows. If inflation stays elevated enough to keep value sectors relevant but not so high that central banks are forced into aggressive tightening, EAFE could remain a steady beneficiary.

Most Bearish Developments

The biggest bearish development is that China’s equity market is not confirming better macro data. China (MCHI) remains weak across 1-month, 3-month, and 6-month windows, with YTD outflows still significant.

The second bearish development is currency stress in Asia. Yen weakness and won depreciation can complicate the otherwise bullish manufacturing and AI story. Currency volatility can reduce foreign investor confidence even when earnings momentum is improving.

The third bearish development is trade fragmentation. A potential end to USMCA, restrictions on foreign inverters, and EU efforts to limit steel imports all point to a less efficient global trade system. That is a headwind for Mexico (EWW), China (MCHI), Germany (EWG), and export-heavy emerging markets.

The fourth bearish development is the commodity reversal. Lower oil is good for inflation and consumers, but it hurts energy-heavy country ETFs. Norway (ENOR), Brazil (EWZ), Saudi Arabia (KSA), and Qatar (QAT) are no longer getting clean support from the commodity side of the cycle.

Chart: US 10yr real yield remains near the high end of the long-term range. The absolute level of interest rates (bottom panel) is moving lower, but investors are still expressing concern about inflation potential through the elevated 10yr yield.

Investment Conclusion

In sum, the country ETF message is constructive, but still selective. The market is rewarding improved factory activity, AI manufacturing, EAFE value exposure, and developed-market quality. The strongest flow confirmation is in Japan (EWJ), South Korea (EWY), Canada (EWC), the UK (EWU), Switzerland (EWL), Germany (EWG), Spain (EWP), Italy (EWI), and Singapore (EWS). The weakest signals remain China (MCHI), Brazil (EWZ), Mexico (EWW), South Africa (EZA), Norway (ENOR), and several energy-sensitive Middle East markets.

The level of interest rates is the key variable to monitor from here. If inflation pressures persist and rates stay firm, the value-heavy EAFE benchmark should continue to benefit from financials, industrials, defensives, and cyclical value exposure. If inflation cools enough to revive optimism around Growth and AI duration, EM and Asia should regain the advantage, led by South Korea (EWY), Taiwan (EWT), Japan (EWJ), and broader semiconductor-linked exposure. The global equity setup is not a blanket international risk-on call. It is a split market: EAFE benefits from value and rate resilience, while EM/Asia benefits from renewed Growth and AI momentum.

ETF performance and flow data sourced from FactSet Research Systems Inc.

News sources: Bloomberg, Reuters, FT, CNBC, Nikkei, Axios, TechCrunch, SCMP, Semafor,

Disclaimer: This material is for informational and educational purposes only and should not be considered investment advice, a recommendation, or a solicitation to buy or sell any ETF, security, country exposure, or investment strategy. Country ETF flows and performance can change quickly and may reflect short-term positioning rather than durable investor conviction. International investing involves currency, geopolitical, liquidity, regulatory, and macroeconomic risks. Past performance is not indicative of future results. Investors should consider objectives, risk tolerance, liquidity needs, and consult a qualified financial professional before making investment decisions.