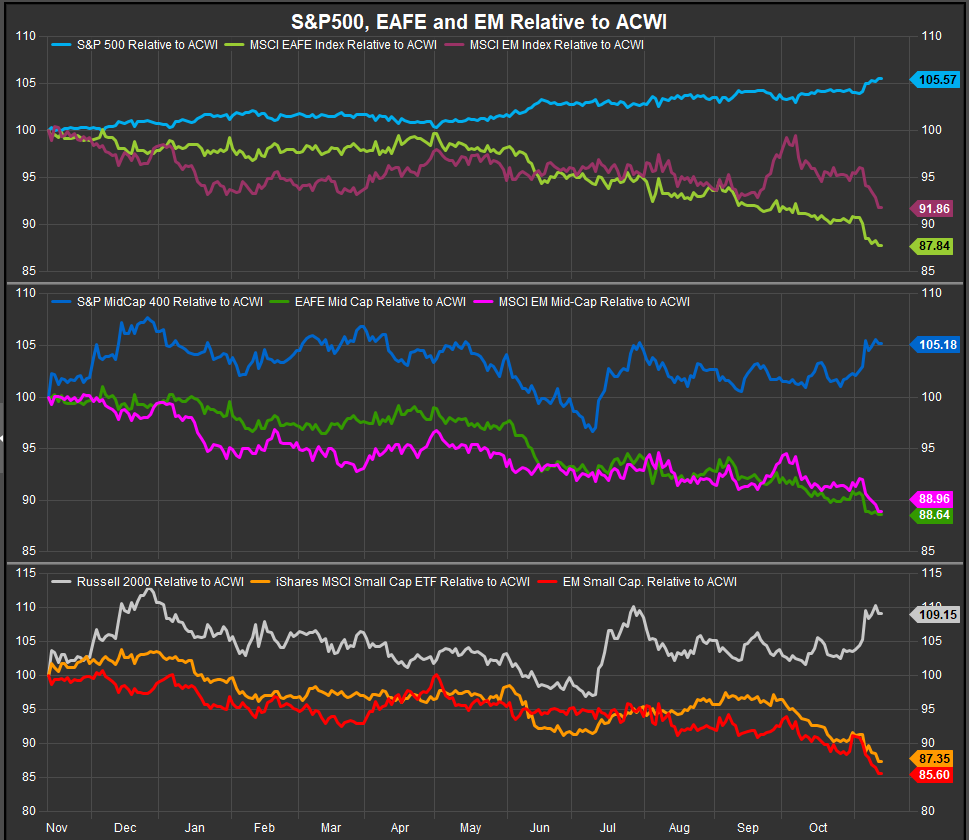

US Large Cap. Still in the Driver’s Seat (now joined by US Small & Midcap Stocks)

We last ran this serial at the end of October, and at the time Chinese equity performance was the headliner. Since then, very little (good or bad) has happened with Chinese equities at the top line. What we’ve seen instead is the resolution of the US Presidential Election putting a tailwind behind the domestic SMID-Cap trade as EM and DM equities have failed to keep pace with the latest round of exuberance in the US.

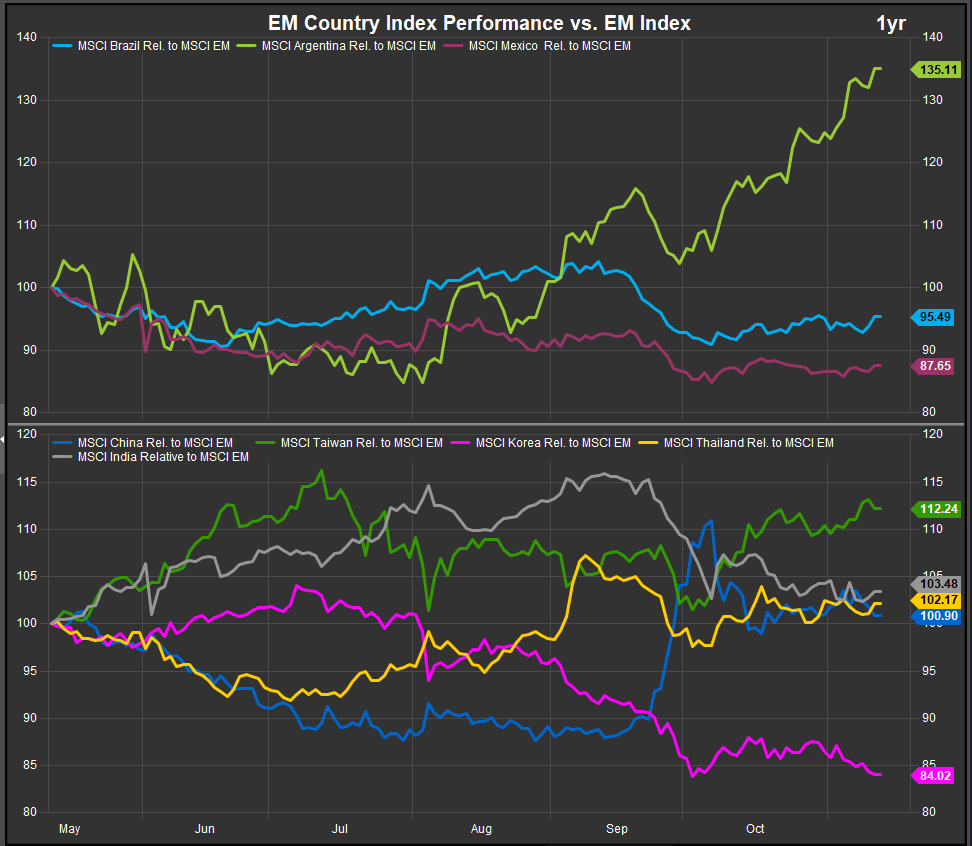

EM Country Performance

Taiwanese and Argentine shares continue to be the top performers in the near-term and over the past 12 months (chart below). The run up in Argentine shares has been nothing short of impressive. The MSCI Argentina Index has outperformed the MSCI EM index by 35% over the past 6-months outpacing regional counterparts.

Among Asia/Pacific countries in the EM space, China continues to consolidate its October gains, and while the bullish reversal pattern in Chinese shares remains intact, the lack of a buyer on the pullback is a bit concerning.

DM Equities Are Starting to Differentiate by Country Performance

In core Europe, German shares have separated themselves positively from those of France, Switzerland and the UK (chart below, top panel).

DM equities in aggregate have lagged during 2024. Our ETF proxy, the iShares MSCI EAFE ETF (EFA-US), has lagged the ACWI benchmark by 13% YTD. However, when looking at EAFE country constituents we see some clear winners and losers emerging. Asia/Pacific countries in the EAFE universe have firmed with strong performance from Singapore to go along with Australian and Japanese outperformance (chart below, middle panel).

Israeli shares have accelerated higher relative to the EAFE benchmark and represent the best performing EAFE country index.

Conclusion

Ex-US equities continue to lag at the aggregate level, but there are clear pockets of strength in some international geographies. Argentina, Israel and Singapore are showing outperformance trends worth getting excited about. China is still intriguing despite the (so far) lack of follow-through on its October surge.

From a macro perspective we would expect US equity leadership to continue over ex-US as long as interest rates/inflation stay contained. This should help the US power through inflationary headwinds to the business cycle while Europe continues its interminable flirtation with recession. Rising rates in the US could change the calculus and put the Fed in an awkward position regarding its continued plans to ease the policy rate and that scenario might open up a preference for ex-US shares.

Data sourced from FactSet Research Systems Inc.