XLE Energy SPDR June Outlook—Energy stocks had a rough month in May and could bounce in the near-term, but the longer-term outlook for Crude and the long-term fundamental drivers of the sector are challenged. We’d rather allocate elsewhere for June after getting stopped out of our long mid-May.

Price Action & Performance

XLE couldn’t attract any momentum buyers to continue it’s near-term bullish reversal in May, confirming the longer-term underperformance trend which has been in force since the beginning of 2023. With inflation becoming tepid, investors rotated to Growth leadership and high yield exposures forsaking cyclicality. The month ended with profit taking in the Tech and Comm Services sectors, but unless consumer trends reverse course to re-trigger inflation fears it gets harder to make a case for owning Energy sector shares.

Economic and Policy Drivers

May started off on a disastrous footing for Crude when inventory reports showed far more Oil on hand than had been reported or expected. This has led to renewed concerns of a global supply glut amidst societal trends away from fossil fuels (vehicle electrification, alt. energy infrastructure, ex-US ESG initiatives) and ever more readily available alternative energy streams coming on line. Given those longer-term constraints, near-term shenanigans are borderline intolerable for potential Crude investors and we saw that with a big share dump in May.

How Can XLE Help?

XLE offers exposure to 23 of the largest US domiciled Energy Co’s. As such it offers superior liquidity and stability vs. the broad market Energy Sector. If inflation prints hot enough to tip the US Economy into recession, Crude and the Oil Majors like XOM, CVX and COP typically outperform through the middle of the recession historically. If the economy continues to surge despite emerging inflation, the Energy sector benefits from being in the Value cohort of the equity market. Value companies typically do well when earnings are abundant, and the cost of capital is rising. The area where it would be vulnerable is if we had a soft CPI print and investors flooded back into Growth areas of the equity market without any consolidation or Fed policy pivot. That is the prevailing condition through May.

In Conclusion

The technical, economic and fundamental cases for owning Energy shares are challenged at present. XLE is one of our 3 0% sector positions for June in our Elev8 Sector Model netting an UNDERWEIGHT vs. the S&P 500 of -3.86%

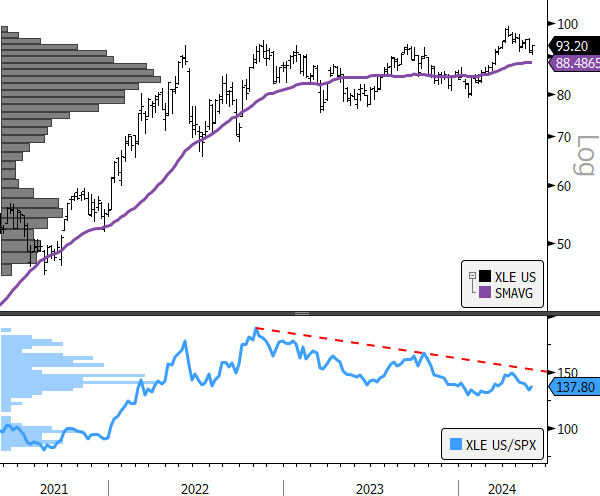

Chart | XLE Technicals

- XLE 12-month, daily price (200-day m.a. | Relative to S&P 500)

- Relative Strength Curve rolled over at downtrend resistance. The steady walk-back of 2022 outperformance continues.