Price Action & Performance

XLF carried a positive end of June through the month of July with the sector finishing the month up >5% and in the strongest technical position in our Elev8 Sector Rotation Model.

At the industry level, Banking and Consumer Finance Industries have been joined as outperformers by the Insurance, Diversified Financials and Capital Markets industries, marking a positive sweep for the sector. Oscillator work registered an overbought reading this month, but the MACD is still flashing a buy signal, and the price pattern is a bullish “Cup & Handle” pattern. New 52-wk highs outnumbered new lows 9 to 0 in August rounding out a very bullish technical picture. Negatives include the weak seasonal period of the calendar and the recent S&P 500 correction, but the intermediate-term setup is quite bullish for equities and for the XLF in particular.

Economic and Policy Drivers

Lower inflation readings have helped reflate many bank balance sheets which had been over-indexed to the long end of the curve back in 2022 when the Fed. was telling us nice stories about transient inflation and no expected rate hikes. Investors have pivoted to expecting interest rate policy easing from the Fed. in the 2nd half of 2024. That has sparked rotation away from Mega Cap. Growth. Financials will likely benefit from any momentum the Trump campaign can gain as election season ramps given his legacy of cutting taxes for the wealthiest and easing regulatory hurdles for businesses. Interest rates remain a key pivot as broadening upside participation in the equity market may spark bets on a reemergence of inflation, but so far that concern is not visible in the data.

Foreign policy in a new administration will likely have some bearing on Financial Sector performance as well. Isolationist policy which is favored by many in the MAGA conservative camp is inherently inflationary as it would likely continue disaggregation of the global supply chain and create barriers to trade. This has potential to put upwards pressure on interest rates and the USD.

In Conclusion

The XLF has found its footing and now looks like one of the most attractive sectors within the US equity market from a technical perspective. Rotation into cyclicals due to expectations of policy easing in the 2nd half of 2024 has been a benefit and we expect it will continue to be in August. Our Elev8 Sector Model continues with an OVERWEIGHT Position in XLF of +3.22% vs. the benchmark S&P 500

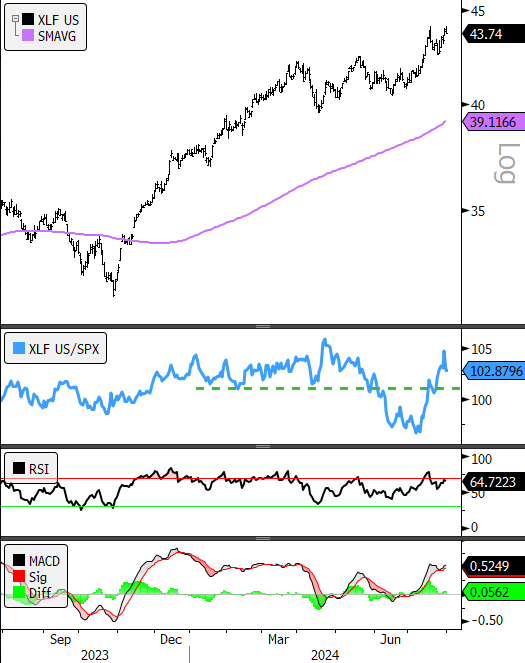

XLF Technicals

- XLF daily (200-day m.a. | Relative to S&P 500)

- Relative-curve is back near highs for the year. We expect some momentum to carry forward amidst bullish oscillator readings and a clear rotation into Value from Growth

Data sourced from Bloomberg