Price Action & Performance

The XLK outperformance trend hit a speed bump in July. Shifts in Fed. interest rate policy expectations revived optimism for other Sectors and led to XLK redemptions. We are taking a constructive view of the resulting near-term oversold condition for XLK and expect investors to snap up discounted shares adroitly.

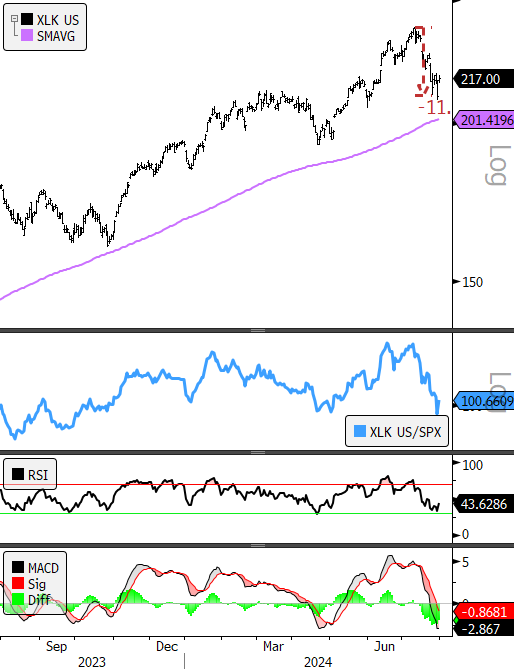

On price action, the XLK posted a peak-to-trough decline near 12% for July. This leaves the sector oversold on the RSI and MACD oscillators. Despite the top line correction for the sector, July produced four 52-wk new highs within the sector and zero 52-wk new lows which gives us indication that the correction is more about taking profits and working off overbought conditions than a clear indication of trend change. We note the sector is now a YTD laggard and the Semiconductor Industry is now flat for the year. We think this will be viewed as an accumulation opportunity by investors generally.

Economic and Policy Drivers

A change in expectations on interest rate policy has sparked near-term rotation away from Technology shares. However, in the longer run, we expect lower rates to catalyze a continued bull market which should be a tailwind to the XLK. The upcoming presidential election season will likely increase uncertainty around foreign policy which has potential to cause elevated uncertainty for sourcing and production. This is an area of major contrast between the two candidates. However, both Trump’s first term and Biden’s presidency saw the Tech. Sector flourish and we don’t see one political party or the other ultimately being better for the sector.

Advancements in AI, continued demand for cloud computing, favorable policy like the CHIPS Act remain tailwinds to the sector.

In Conclusion

We expect the inter-play between AI builders and AI users will be a continuing theme underpinning the bull market. The 18 months from January 2023 through June 2024 were dominated by XLK. Now at near-term oversold conditions we expect “FOMO” investors to pick up the trade into year-end. We do think there is potential for elevated volatility between now and the election, so we’ve taken in our position this month to cover more areas of potential upside in the near term. Our Elev8 Sector Model starts August with an OVERWEIGHT allocation of 2.27% for August.

Chart | XLK Technicals

- XLK 12-month, daily price | 200-day m.a. | Relative to S&P 500)

- XLK is now deeply oversold in an intact long-term uptrend. Negative seasonals could complicate the scenario, but on its face, this is a textbook bullish accumulation opportunity for XLK