XLK Information Technology Sector SPDR September Outlook—A material correction in the XLK this summer has the sector on neutral footing entering September. Our process favors the longer-term trend until there is convincing evidence it has failed. We begin September long the XLK and we expect investors will eventually see this intermediate term consolidation as an accumulation opportunity.

Price Action & Performance

We got shaken out of our long XLK position early in August, only for the whipsaw to trigger us back in on August 19th. These were tactical longs and shorts rather than structural, but we interpret the July/August correction as a warning, and we need to see price stay above the 200-day moving average to maintain our bullish conviction.

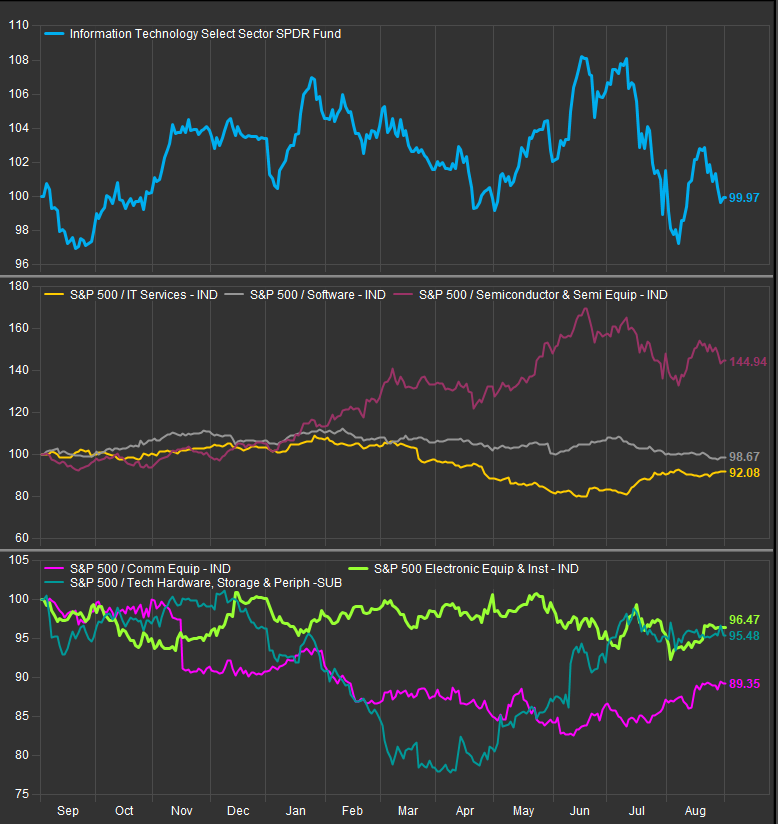

At the Industry level, the powerhouse Semiconductor Industry has been consolidating since its relative peak in June. Since June 1, Semiconductor and Software underperformance has dragged the sector relative curve down while IT Services, Comm. Equipment and Hardware have outperformed. This has been a bit of an intra-sector laggards rally.

At the stock level we still find many attractive charts. As previously mentioned, our process gives the benefit of the doubt to the strong long-term trends. We still evaluate the XLK long-term outperformance trend as viable and the macro conditions as supportive. If we undercut the recent relative-low, the picture changes for us.

At the stock level our favorite names are GDDY, FICO, ORCL, PANW, TYL, ANET, MSI, AAPL, APH, KLAC, MPWR and NVDA

Economic and Policy Drivers

A change in expectations on interest rate policy has sparked near-term rotation away from Technology shares. However, in the longer run, we expect lower rates to catalyze a continued bull market which should be a tailwind to the XLK. The upcoming presidential election season will likely increase uncertainty around foreign policy which has potential to cause elevated uncertainty for sourcing and production. This is an area of major contrast between the two candidates. However, both candidates are aligned with certain Tech surrogates, and are unlikely to court a powerful adversary in the Tech lobby.

Advancements in AI, continued demand for cloud computing, favorable policy like the CHIPS Act remain tailwinds to the sector. A concentration of users in the P/E space is a potential worry as those businesses may artificially inflate the user base of Tech. services. However, with interest rates moving lower, PE is likely getting some relief through decreased funding costs.

In Conclusion

We expect the inter-play between AI builders and AI users will be a continuing theme underpinning the bull market. The 18 months from January 2023 through June 2024 were dominated by XLK. Now that it’s tracing out an intermediate term consolidation we expect “FOMO” investors to pick up the trade into year-end. We do think there is potential for elevated volatility between now and the election, so we’ve kept our position modest this month to cover more areas of potential upside in the near term. Our Elev8 Sector Model starts September with an OVERWEIGHT allocation of 2.02% for September.

Chart | XLK Technicals

- XLK 12-month, daily price (200-day m.a. | Relative to S&P 500 | MACD | RSI)

- XLK is consolidating its attempted bullish reversal. The bet here is this intermediate term consolidation will be accumulated sooner than later

XLK Relative Performance | XLK Industry Relative Performance | 1yr

Data sourced from FactSet