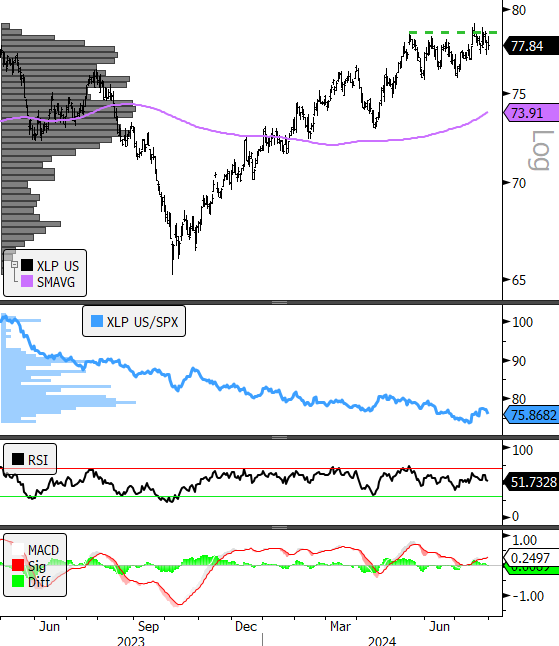

Price Action & Performance

XLP outperformed the S&P 500 in July by 74bps for the month of July. Similar to our view on XLV we are not impressed by the reversal so far and attribute it more to top level weakness from the S&P 500 index as a whole (which is correcting in a strong uptrend) rather than any catalytic enthusiasm for Staples shares. XLP oscillator work failed to hit any overbought readings on the RSI which is a negative attribute, while the MACD rolled over into a neutral position after briefly triggering a buy signal mid-month. It also failed to sustain a break-out above resistance on price which keeps it out of favor with the technical inputs in our model. 3 stocks in the Sector made 52-wk highs during the month. The technical were an improvement, but not impressive.

Economic and Policy Drivers

Cooler inflation prints in May, June and now July have cut the legs out from under the recession trade and have given the edge to high-beta stocks at the expense of min vol. stocks for the time being. XLP is a part of both cohorts on the losing end of these developments. We would likely need to see a sustained correction through August for XLP to outperform.

Staples co.’s typically operate lower margin businesses with a broad array of essential products. The product categories are typically associated with value-oriented marketing. This has caused consumers to balk at some of the higher prices showing up on store shelves for established brand names. The present behavioral trend is exacerbated by increased competition from private label entrants into the traditional staples categories.

ESG policies also add a layer of cost that is particularly difficult for the Staples sector. Increased R&D and costs associated with recyclable and reusable packaging is a strain on lower margin businesses that market low price points.

While expectations of dovish interest rate policy animate a near-term bid into laggards, we don’t see a clear catalyst for long-term outperformance in the XLP at present. Rather, the dynamics outline above remain in force.

How Can XLP Help?

XLP has several characteristics that make it attractive to investors when there is expectation of equity price correction, volatility, or economic decline into late cycle or recession. It is comprised exclusively of Large Cap. US stocks which generally offer a lower volatility profile to the broad market. It has one of the highest dividend yields among the 11 GICS sectors, which offers income and stability when markets are falling on price. That isn’t the environment we appear to be in at present, but if we get negative surprises on inflation or exogenous shocks that challenge the bull trend, XLP offers a quick way to add defensive characteristics to an equity portfolio.

In Conclusion

Weaker inflation and a fairly bullish earning season from the Tech. Sector have put the XLP in the back seat. Several o our model inputs have deteriorated for the sector since May and it now scores as a zero-weight sector for July in our work. Our Elev8 Sector Rotation Model Portfolio remains out of XLP for August and starts the month short the sector -5.8% vs. the benchmark S&P 500

Chart | XLP Technicals

- XLP 12-month, daily price (200-day m.a. | Relative to S&P 500)

- Relative downtrend remains intact despite July gains. We remain short.

Data sourced from Bloomberg