Price Action & Performance

XLP outperformed the S&P 500 Index in April on a monthly basis for the first time since October of 2023. With some of the trends that have fueled the bull market taking a pause there is increasing reason to believe the market must pause to consolidate gains off the October ’22 low. If that is to occur, it is very likely XLP can continue to outperform from here as it would benefit from rotation away from leadership while offering low volatility characteristics at a point where volatility is likely to increase.

Economic and Policy Drivers

Inflation is a dominant theme across all sectors, but with very different implications. XLP outperformance would likely be driven by a hotter inflation print and a more Hawkish Fed. This may seem counter-intuitive, but the more Hawkish the Fed becomes, the more likely investors are to price in recession which would benefit low vol. sectors that historically act as defense. From an economic perspective, we are seeing signs of consumers trading down to more value-oriented spending. Strength in staples retailers like TGT, COST and WMT is reflective of this. Any significant correction in the equity and fixed income markets (rising rates = falling bond prices) has a negative wealth effect on the consumer generally, and if that is coupled with continued rising commodities prices Staples would be very likely to outperform relative to the broad market.

How Can XLP Help?

XLP has several characteristics that make it attractive to investors when there is expectation of equity price correction, volatility, or economic decline into late cycle or recession. It is comprised exclusively of Large Cap. US stocks which generally offer a lower volatility profile to the broad market. It has one of the highest dividend yields among the 11 GICS sectors which offers income and stability when markets are falling on price. It also contains many of the companies that have been and would continue to benefit from a tightening consumer. TGT COST and WMT mentioned above are prominent weights in the Sector and have outperformed in 2024 in aggregate as well as in April. They are major beneficiaries of economic substitution. Personal products like toothpaste, soap, laundry detergent and deodorant are seen as non-cyclical products that people need regardless of recession. Food is clearly a necessary and Tobacco has very strong customer loyalty. These are all reasons why 5 of 6 industries within the sector outperformed and market internals are improving for the sector at a time when they are deteriorating for the broad market.

In Conclusion

Headwinds for equities broadly typically benefit the relative performance of XLP. With the SPX off close to -6% over the past month and inflation getting hotter not cooler, there is a good chance for XLP to help investors this month. I would recommend an overweight position in XLP for May.

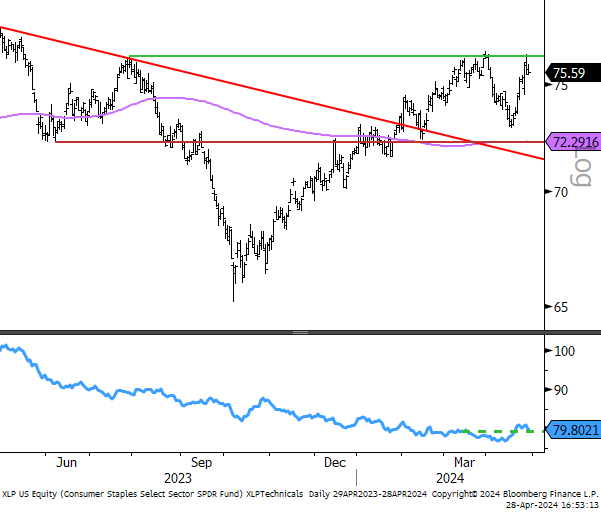

Chart | XLP Technicals

- Price approaching resistance (green line) at the $77 level with support at the $72 level, which aligns with the 200-day moving average (purple line)

- Relative Strength Curve (blue line) is signaling a near-term buy signal with a break-out above a previous high (dotted green line)